Daily Variation Margin flows between Clearing Houses and Clearing Members and between Clearing Members and their Clients are sizeable e.g. we know from LCH SwapClear’s CPMI-IOSCO Disclosures that the highest VM paid on a single day by all members to the CCP was $16 billion!

As Clearing Houses make intra-day margin calls, Clearing members generally maintain a margin buffer for operational efficiency and will require their clients to do likewise. Meaning that each day the profit from a position is not drawn down to zero or the loss made up to zero, but instead a cash buffer is maintained in the margin account. The size of this buffer depends on clearing risk policy and on a firms operational ability to find same day cash to cover any intra-day margin call and the cost of doing so.

In this article I will look at how to determine an appropriate size for the margin buffer.

A Simple Approach

As we need the buffer to cover a potential 1-day loss, a simple approach is to use the Initial Margin determined by the Clearing House and scale it down to a 1-day period. Lets use an example to see how appropriate this is.

Initial Margin

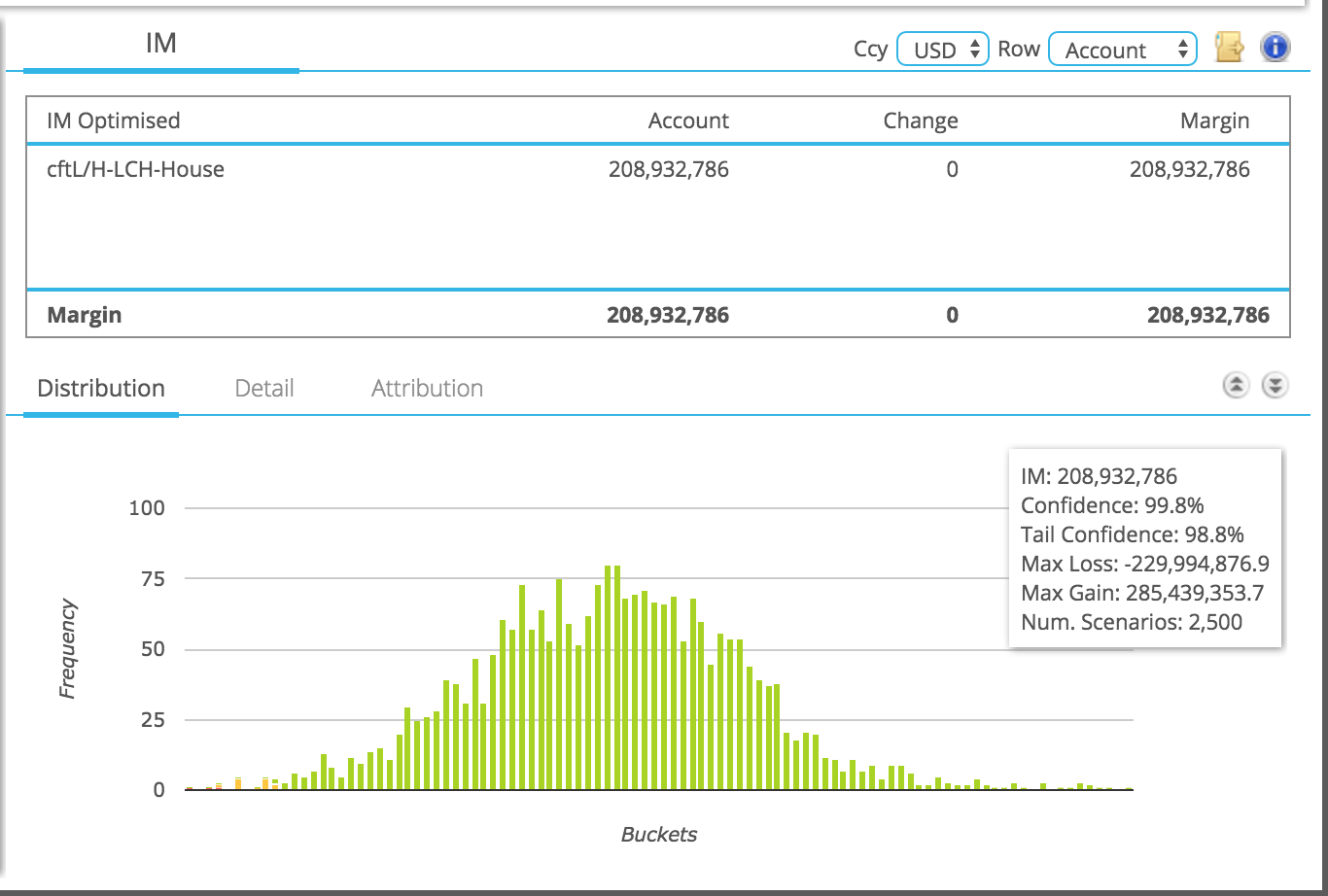

Using CHARM, we create an Cleared Swaps account with the following Delta sensitivity profile.

Seven currencies with an overall Delta of -$7.8m; meaning for each 1bps risk in rates, this account will lose $7.8m. Note the substantial position in EUR, GBP and CAD, as well as 10Y and 25Y.

Running LCH IM in CHARM for this account and assuming it is a House account.

We get an IM of $209 million.

As this is for a 5-day period, we can approximate a 1-day period by dividing by the square root of 5, giving $93.5 million. Now in reality we would round this up as we do not want to be adjusting the buffer too frequently, but lets go with $93.5 million as our estimate.

Whats Wrong with this?

Well at almost half the IM, the buffer looks to be too conservative for the risk in the account.

By using the LCH IM figure we are using a model that covers 10 years history of 5-day moves and takes a 99.7% confidence level Expected Shortfall measure.

How else can we size the buffer?

Well we could look at the history of margin calls on this account, say for the past year and using that data pick the largest amount we have had to provide.

But that is a worse approach as the risk in our account could well have changed significantly over the period and so we would not be comparing like for like.

A better approach would be to use the history of 1-day moves in our risk factors and apply those to our current portfolio and determine a loss for a given confidence level.

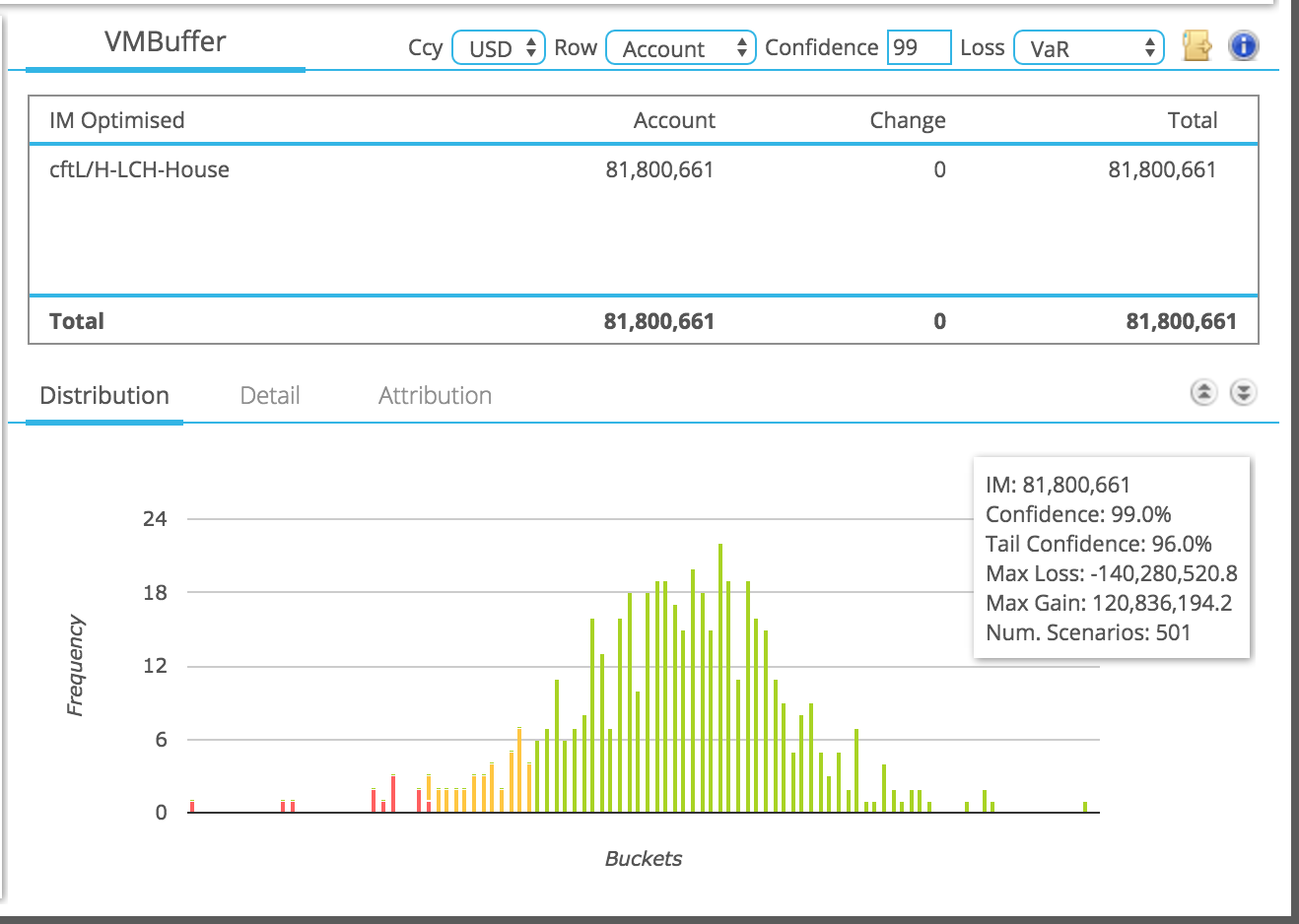

Historical Simulation using 1-day shifts

In CHARM we can do precisely this using either a 1-year or 2-year historical period.

Giving us $82 million using a VaR measure at 99% confidence level.

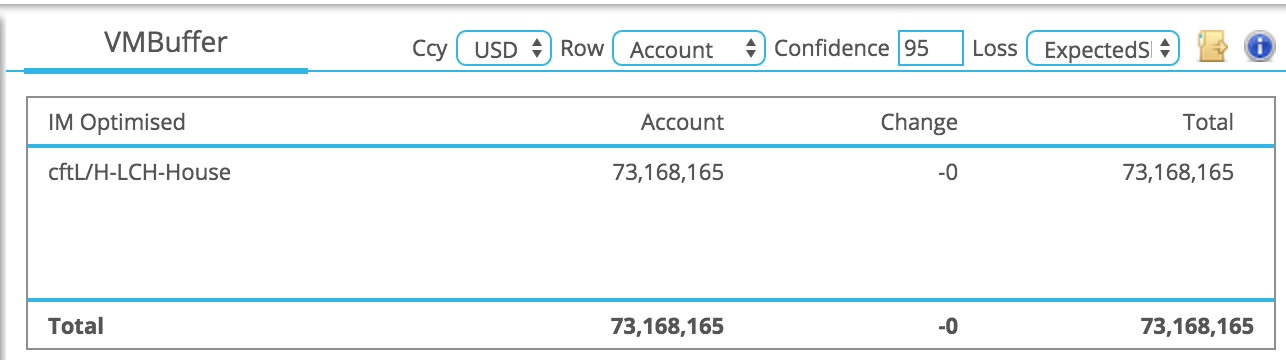

Lets use a different confidence level and statistic.

Giving us $73 million using Expected Shortfall and 95% confidence level.

Both lower than the $93.5 million derived from the IM; but which should we use $73 million or $82 million?

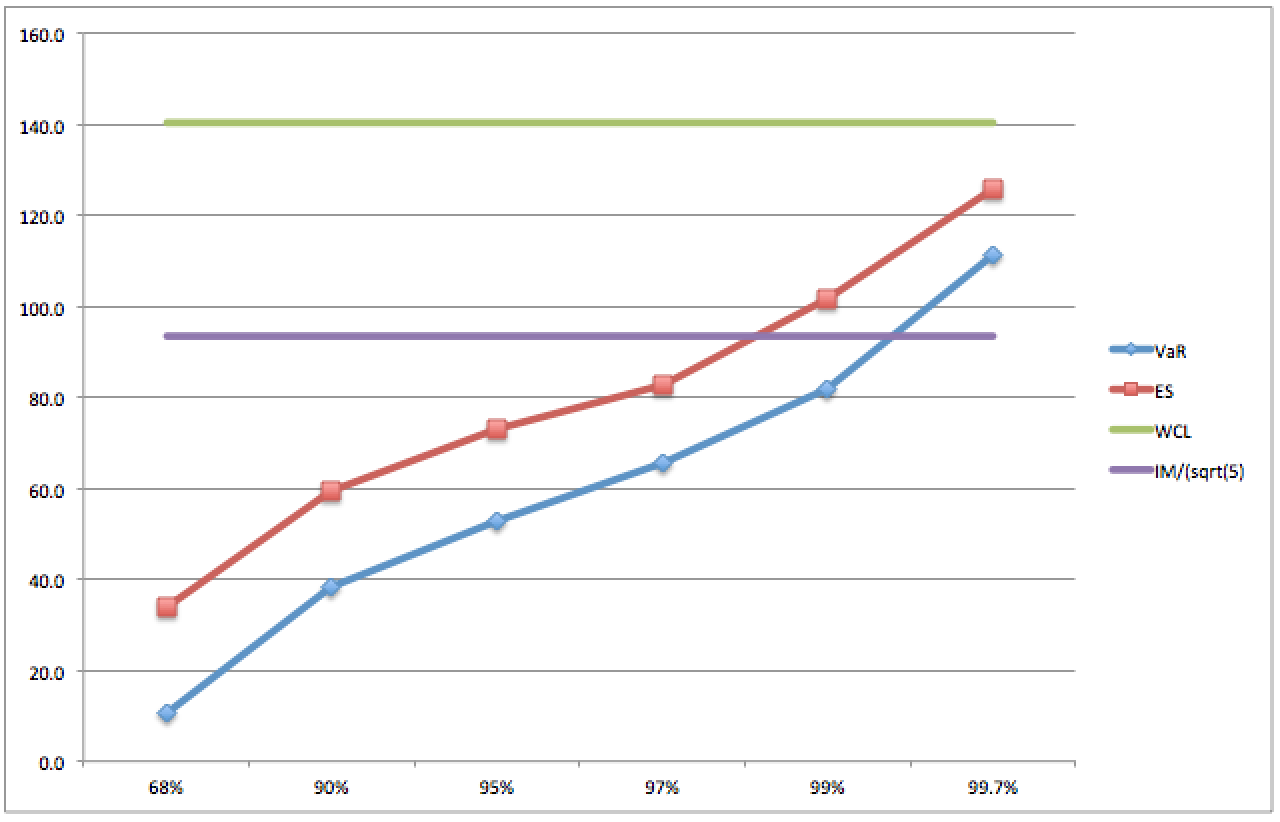

First lets run a few different confidence levels and measures, starting with 68% for one standard deviation all the way to 3 standard deviations as well as the worst loss. Doing so, we get the following chart.

Showing the:

- Green line as the Worst Case 1-day loss of $140 million

- Purple line as the IM derived estimate of $93.5 million

- Blue line as VaR at specified confidence levels

- This crosses at 99.2% with the IM derived estimate

- Red line as ES at specified confidence levels

- This crosses at 98% confidence with the IM derived estimate

Giving us a wide range of values, all the way from $10 million to $140 million.

Which is the right answer? Well it depends.

My gut feel tells me $73 million (ES at 95%), which is $20 million lower than the IM derived estimate.

Why? Because I am comfortable that on average once a month this buffer might be exceeded, while if this occurred once in a hundred days (i.e. twice a year) my operational procedures to cope with the event might not be smooth.

Discussion

While there is no right answer as to the size of this buffer, it is important that it is:

- Responsive to changes in risk on the portfolio. If there is an increase or decrease in risk, the buffer must change accordingly. Daily change is probably too frequent, but monthly or quarterly would be appropriate.

- Balances the availability of same-day funds versus the potential cost of maintaining a liquidity buffer. This seems like a “business” decision (i.e. how much risk are we comfortable with?), because it is very likely that on a day of large VM calls, same-day cash will be exceptionally hard to raise.

Firms may also wish to consider what currency they are likely to be called-in versus the currency they keep their buffer in e.g. USD.

Clearing Members should run such analysis for each of their client accounts, where the additional risk is that for an intra-day CCP margin call, the client may not able to provide same day funds, which the Clearing Member will be obliged to provide to the CCP.

CHARM provides the analytical tools necessary to make more informed decisions on sizing the margin buffer.

We use the current risk of the portfolio and run rigorous statistical tests.

These are better than simple approximations using Initial Margin.