This is not quite our normal “LIVE BLOG” type of announcement for SOFR First in Swaptions (and other non-linear derivatives).

I tend to think that Options markets like to make things (unnecessarily?) complicated, and so there are a number of moving parts to look at for SOFR First in USD Swaptions.

In Summary

- November 8th 2021 was the “SOFR First” initiative for interdealer markets in USD Swaptions.

- IBA also started publishing a benchmark-compliant ICE SOFR Swap Rate on the same day.

- At the time of writing this blog, ISDA have not yet added this new ICE SOFR Swap Rate to their definitions. We believe the update is imminent.

- This means that USD Swaption traders have only been able to trade SOFR Swaptions as physically-settled products so far this week, which is different to previous market standards that were cash-settled.

- We still saw 13-17% of the USD swaptions market transacted versus SOFR so far this week.

- This is likely to move much higher once cash-settled USD SOFR Swaptions start trading.

RFR Swaptions

First off, it is worth taking a look at GBP markets as an example of what is possible for RFR swaptions trading. SONIA first for GBP non-linear derivatives arrived on May 11th 2021:

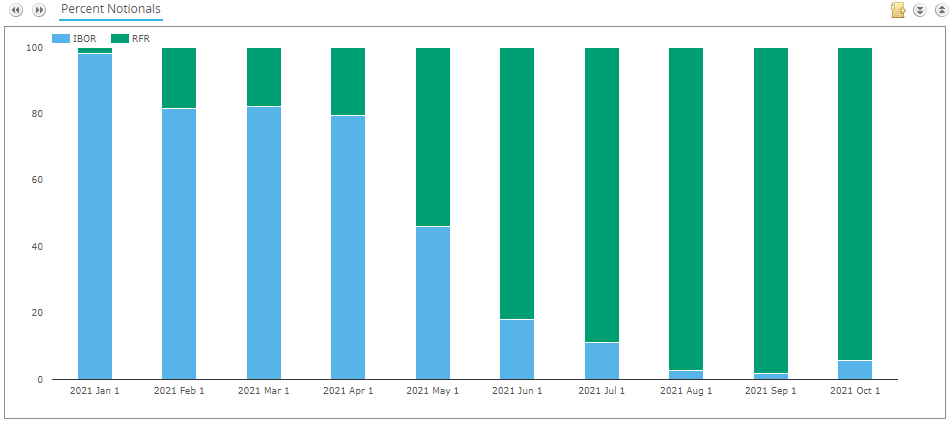

When we look at GBP options reported to SDRs we see that 95%+ of Swaptions are now trading versus SONIA (the RFR):

Okay, this is not the best source of data for the GBP market but it’s what we have. This data is fairly considered reflective of the overall market and highlights that trading of Swaptions, Caps, Floors etc on an RFR has been successfully adopted as the market standard.

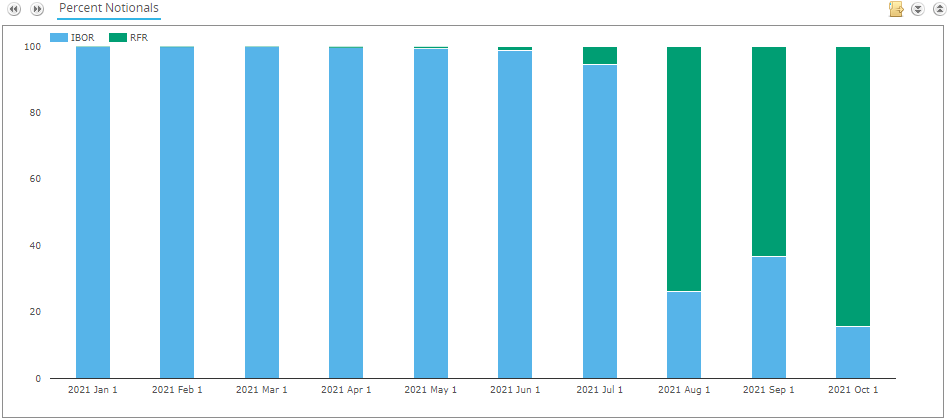

Interestingly, JPY has seen a similar transition since TONA took-off, with TONA swaptions now making up 84% of traded volumes reported to SDRs:

Of the LIBOR set of currencies with active swaptions markets, this now leaves USD as the odd one out. Let’s see how yesterday went.

SOFR First for USD Swaptions

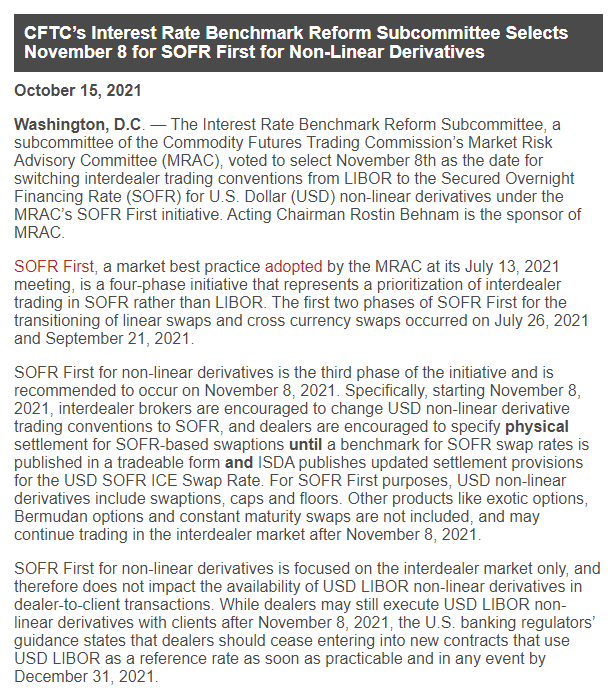

First off, recall that the announcement from the CFTC was somewhat nuanced when they announced the November 8th 2021 date:

Namely, SOFR first for Swaptions is;

- For the interdealer market only.

- The language here implies that the Swaptions should be physically settled (into a SOFR swap cleared at either LCH or CME).

- Cash settlement is not being ruled out, but the market needs to wait for some announcements from benchmark providers and ISDA.

IBA and ISDA to the Rescue?

My (somewhat limited!) understanding of the USD Swaptions market is that it mainly trades cash-settled. I think there are many questions to be raised as to exactly why this is, but as we have been made painfully aware during the RFR transition, changing market conventions is hard. Like, really really difficult!

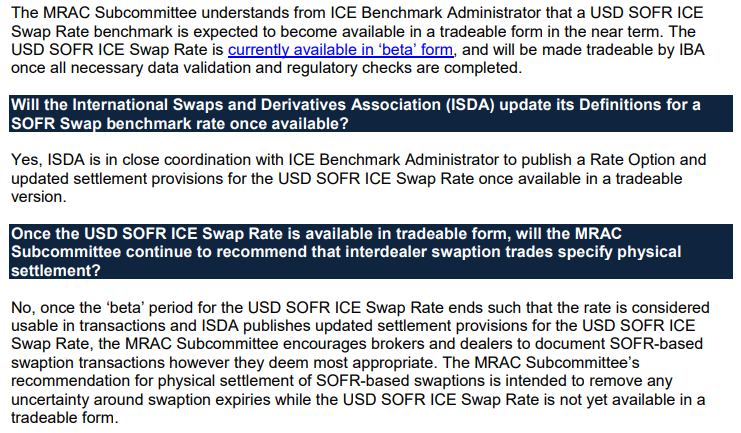

There was an FAQ document issued by the CFTC in conjunction with their SOFR First announcement for Swaptions, and it makes pretty interesting reading. The main point is:

In Summary;

- IBA (ICE) were already working on publishing a benchmark-compliant SOFR Swap Rate, and it was being published in “Beta” (test) at the time of the SOFR First announcement.

- Whilst IBA still had some work to do to secure regulatory approval for these new rates, there was also work involved by ISDA.

- In short, before cash-settled swaptions should be traded against SOFR, both IBA and ISDA had some work to do.

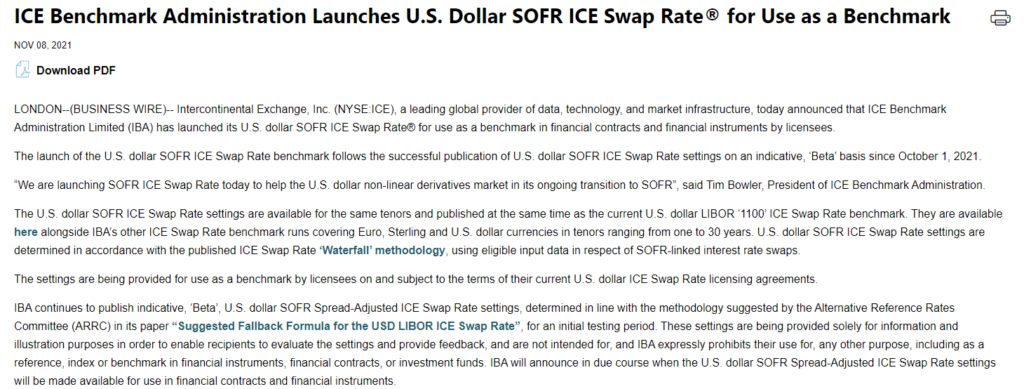

And what do you know? Yesterday, IBA issued a press release that their SOFR ICE Swap Rate® is now available for trading!

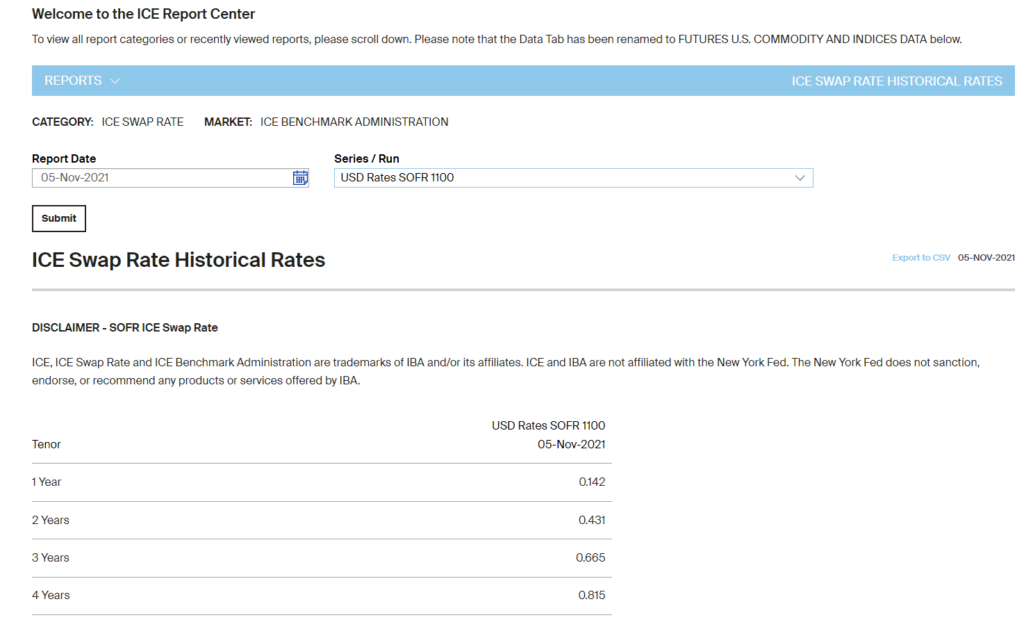

We can now all access these SOFR Rates on the ICE Market Data portal which is certainly a step closer to trading cash-settled SOFR swaptions:

Final Parts of the Puzzle

I believe ISDA will imminently update their documentation (sometime today), so that we can all bask in the glory of a flood of SOFR Swaption trading in the USD market. I admit I am not 100% sure what ISDA need to do, but I guess it is something along the lines of:

- Insert a definition of the (now published) USD ICE SOFR Rate.

- Make the USD ICE SOFR Rate the fallback for the existing USD ICE LIBOR Rate.

- Define some type of fallback for the USD ICE SOFR Rate.

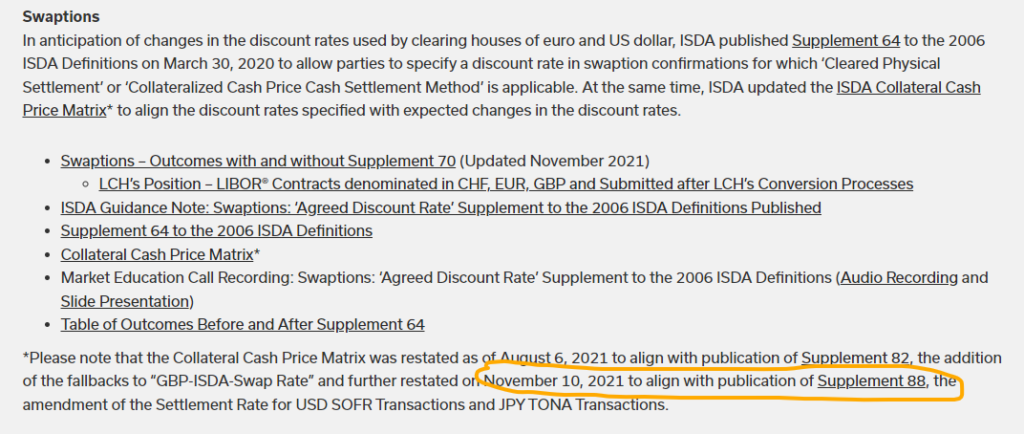

Looking under “Swaptions” on the ISDA Benchmark Reform page suggests that this process has been completed for GBP swaptions, and that we are now waiting for something equivalent to “Supplement 70” (GBP) to cover USD SOFR swaptions (and JPY). I will try to update this blog once the ISDA publications are out.

The existing Supplement 70 talks about fallbacks for both LIBOR-based ICE swap rates and even what may happen if the RFR-based ICE swap rates are not published (there’s an interesting Fallback scenario to think about for our readers!).

**UPDATE**: The Supplement 88 is now published on the ISDA website:

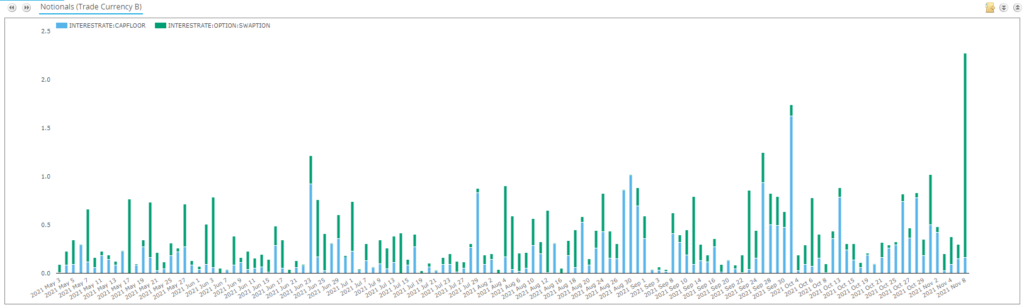

So What Traded in SOFR Swaptions?

All of this is happening “in real-time” so to speak. Fortunately, SDR data is published with only a 15 minute delay, so we can see the impact of SOFR First on the USD Swaptions market:

Showing;

- The notional volume of USD SOFR Swaptions reported to US SDRs each day since May 2021.

- Monday 8th November was the first day we saw more than $2bn notional of SOFR swaptions trade.

- The SDR does not indicate whether swaptions are cash-settled or physically settled (it does not include the reference cash-settlement index nor the CCP where the swap would physically settle, which is a shame).

- Let’s therefore assume that 100% of the volumes are cash-settled at the moment.

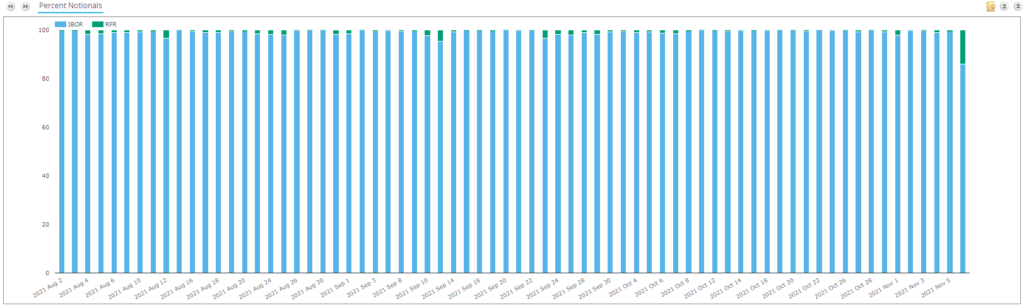

So a record day in SOFR Swaptions. It is important to put this in context against all other Swaptions reported:

Showing;

- The percentage of notional traded in the USD Swaptions market as either IBOR (blue) or SOFR (green, “RFR”).

- Yesterday was a record day for SOFR.

- 13% of swaptions activity was versus SOFR.

Is 13% of the SDR equivalent notional (or 17% by trade count) a good start for SOFR First in Swaptions? Put one way, I would guess that it accounted for the vast majority of physically-settled swaptions yesterday!

I think if you consider that a) we are targeting only interdealer markets and b) the infrastructure does not appear to have been in place yet for the “market standard” instrument, 13-17% is a great start!

In Summary

- SOFR First in Swaptions resulted in more than $2bn notional of SOFR swaptions transacted.

- This accounted for 13-17% of the USD Swaptions market.

- The market was initially waiting for important infrastructure to be put in place to trade cash-settled USD SOFR swaptions.

- This is important because the market-standard for USD swaptions prior to RFR reform was cash-settlement.

- Expect SOFR Swaptions to account for an even greater portion of the market once cash-settled swaptions start trading.

- It is a shame we cannot see in the SDR which swaptions are cash- or physically- settled.