The latest ISDA-Clarus RFR Adoption Indicator presents some truly incredible numbers in August 2021. On to the details.

August 2021

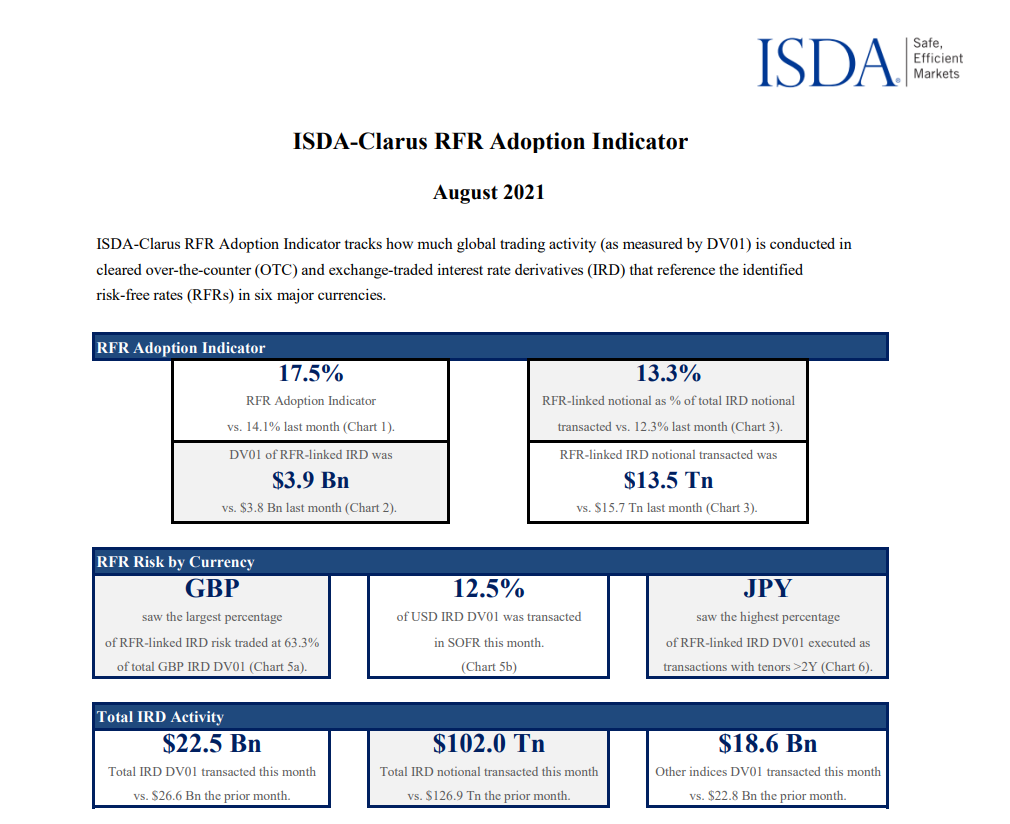

The headline RFR Adoption Indicator increased to a new all time high of 17.5% in August 2021. The chart looks particularly healthy:

August 2021 was the first month where SOFR First really demonstrated its impact in the USD market. However, there are highlights across all of the LIBOR currencies:

- A new all-time high of 17.5% for the overall RFR Adoption Indicator.

- USD SOFR adoption increased to 12.5%, following the “SOFR First” initiative.

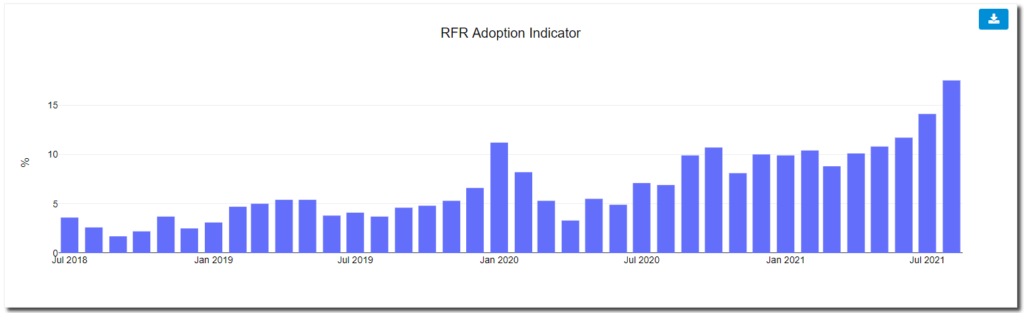

- 49.5% of JPY risk was versus TONA.

- 50% of CHF risk was versus SARON.

We will show some new USD data at the end of this blog, but let’s also check in on the significant moves in JPY and CHF. The rate of adoption in these two currencies is even more impressive than the move in USD.

JPY TONA

The RFR Adoption Indicator in JPY hit 49.5% last month!

- The rise in TONA trading has been truly meteoric.

- It was at just 6.9% of the market in June this year, less than three months ago!

- The JPY market shows how quickly things can change.

With 50% of the market now trading versus TONA, this suggests that it is not only the interbank market that is adopting RFRs in Japan. There must have also been a significant shift in client markets. This is great to see and evidence that once RFRs gain traction, liquidity moves very quickly.

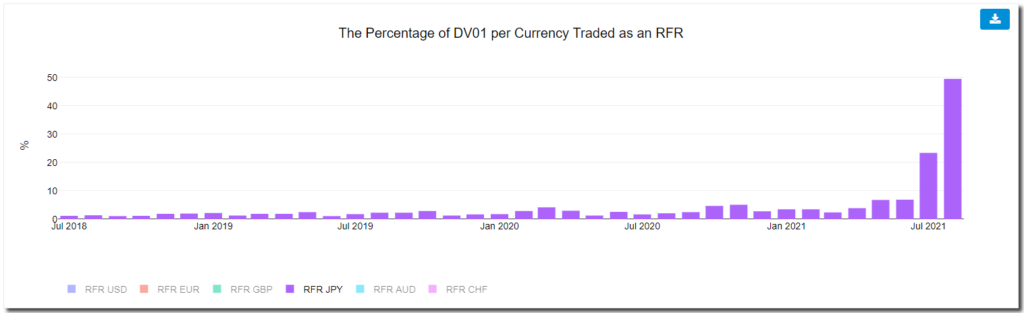

CHF SARON

Our second “poster child” of August 2021 is the CHF RFR market. 50.4% of risk was traded versus SARON last month:

- CHF markets seem to be able to shift VERY quickly when market standards finally change. Recall the original demise of TOIS and the adoption of SARON back in November 2017 (Yes, benchmark reform really has been going on that long!).

- SARON trading was just 6.3% of the market six months ago in March 2021.

- Even three months ago, it was only at 13.7%.

- The past two months have been transformational for the CHF market. Whilst July and August may be traditionally quiet months, they have seen real transition happen.

We assume that with over 50% of the CHF market now trading versus SARON that clients are also adopting RFRs. This widespread adoption is very promising for a smooth transition as we head toward Q4.

CHF and JPY seem to be progressing very well. This is a far cry from where we were when LIBOR’s demise was announced in March of this year. Back then, Clarus responded to the IBA consultation with concerns over CHF and JPY markets specifically:

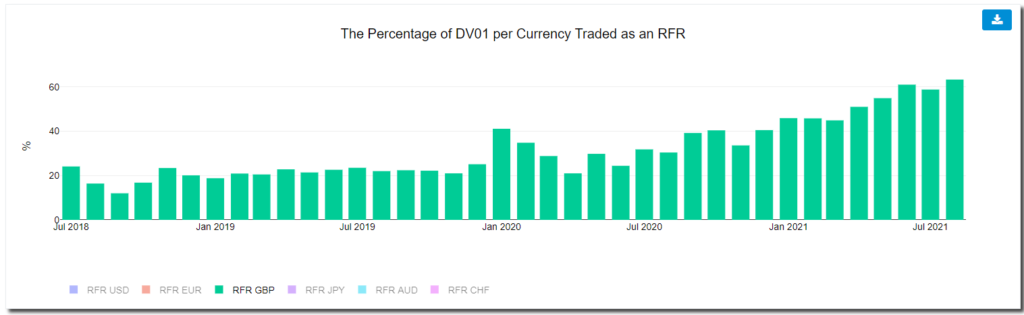

GBP SONIA

Let’s not allow UK markets to become victims of their own success here! GBP SONIA saw a new record in RFR Adoption last month, reaching 63.3% of all risk traded:

USD SOFR

Finally, let’s look at a couple of novel aspects of the USD data.

- SOFR accounted for 12.5% of all USD risk traded.

- For USD OTC trading (i.e. excluding futures), 17% was transacted versus SOFR.

- SOFR risk traded in OTC markets was twice as large as SOFR risk traded in ETD markets. Previous to July this year, ETD SOFR markets (i.e. SOFR futures) had always been much larger.

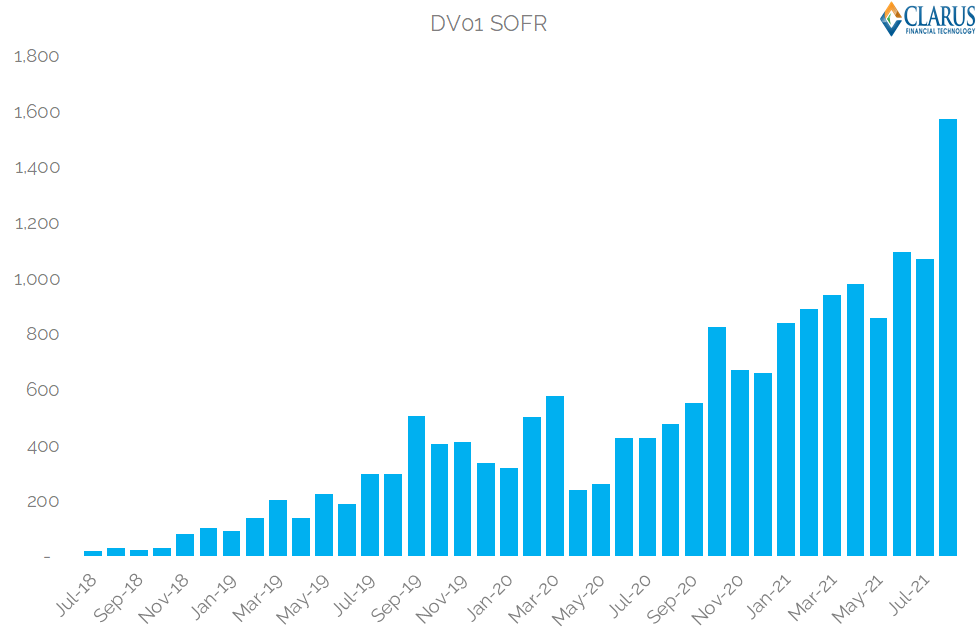

- Total SOFR DV01 was a record amount, with over $1.5bn DV01 traded (+47% versus last month).

Given how quiet August 2021 markets were, the sheer amount of SOFR risk traded is pretty impressive:

Our particular notes on this data include:

- Futures are now lagging OTC markets by a significant amount. Twice as much risk trading in OTC markets than ETD markets isn’t “normal” for USD markets. Will futures transition accelerate over the Sep and Dec IMM rolls?

- 17% of USD OTC markets trading versus SOFR is consistent with our recent analysis (even a little higher). Is it fair to assume all of this is interbank activity or are clients getting in on a significant portion of the action too? We would like to see what the Tradeweb and Bloomberg SEF RFR Adoption Indicators are to get an idea of this. Head over to SEFView to look at the client activity in SOFR yourselves.

Closing Remarks

Looking at the precedents out there, such as JPY and CHF in the past two months, USD SOFR looks well set to accelerate into Q4.

It might seem strange to readers that with GBP, JPY and CHF all at 50% (or more) that our overall indicator is at 17.5%. Looking at the data, there are two reasons for this:

- USD markets are the largest Rates markets by some distance, therefore are a primary driver of the overall adoption indicator.

- EUR markets still see almost no uptake of €STR trading.

Monitoring the data promises to be an interesting task into Q4. We will continue to work to ensure the necessary transparency is brought to the market to allow market participants to monitor these important trends.

In Summary

- The ISDA-Clarus RFR Adoption Indicator hit a new all-time high of 17.5%.

- USD SOFR adoption increased to 12.5%, following the “SOFR First” initiative.

- 50% of both JPY and CHF markets now trade versus RFRs.

- 63% of GBP risk was versus SONIA, a new high.

- The data continues to reveal that transition is happening in RFRs.