The use of Risk Free Rates (RFRs) such as SONIA and SOFR continues to grow. Volumes are increasing as described in recent Clarus blogs, see SOFR Volumes April 2019, SARON Activity and Growth in RFR Markets.

But the development of a term market in RFRs is still in it’s early stages. Clearing House data shows significant trading in the shorter maturities (< 2 years) but much less in longer maturities. In this blog I look again at the CCP volumes for SOFR and SONIA and whether the transition from IBOR-based trading to RFR-based trading has been extended to maturities beyond 2 years.

Recently, the Alternative Reference Rates Committee (ARRC) has published a Users Guide to SOFR,which at 21 pages is a good read and well worth it when you have 15-30 mins to spare. In the guide, the concept of a forward-looking rate was discussed as one way to encourage the uptake of RFRs in cash markets to develop trading in longer maturities.

A Term RFR (TRFR) is still in development but could greatly assist certain products and markets establish a longer term RFR curve.

Cleared RFR volumes

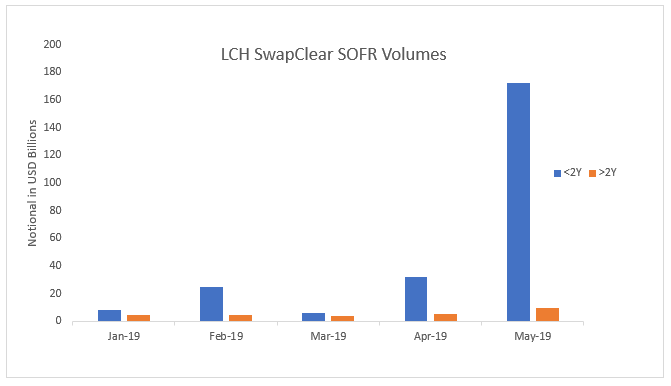

Lets starts with LCH SwapClear monthly volumes of cleared USD SOFR Swaps.

- A big jump in May with < 2Y cleared volume of $172 billion of double-sided gross notional.

- While > 2Y volume is just $9.7 billion.

- (No need to convert to dv01 equivalent as even then > 2Y volume is significantly less than < 2Y).

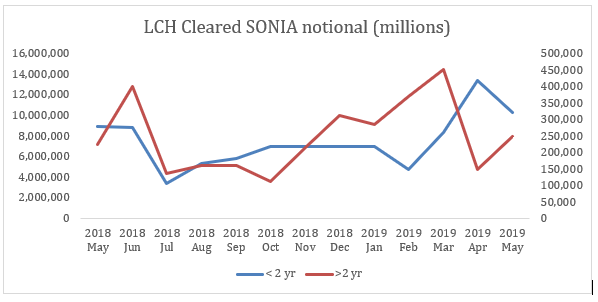

Next the SONIA chart below shows that there is still a long way to go before longer-term SONIA trading (RHS scale) is comparable to the shorter dated < 2Y trading (LHS scale).

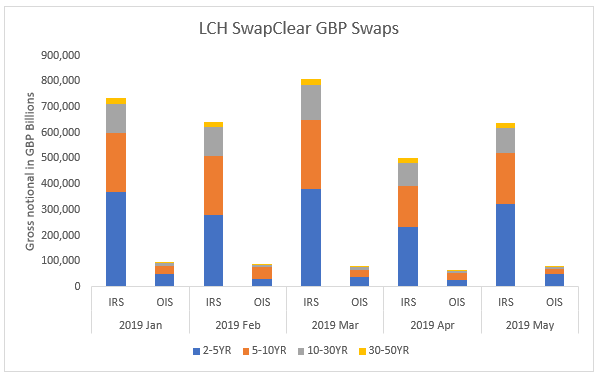

The following chart shows GBP volumes in IRS and OIS for tenor buckets greater than 2 years and shows there is much to be done before 2021 for the OIS SONIA bars to take over from the IRS Libor ones.

Underlying risk

Many market participants recognise the need to switch from Libor to RFRs well ahead of 2021. But the challenge remains how this may be achieved. Derivative markets, as shown by the cleared volumes, are not showing clear signs of making that transition.

But derivatives are just that; derivatives. The underlying demand from cash markets for RFR-based products and trades is not evident yet, which would drive a response from the derivatives markets to provide hedges.

Many end users of financial products across loans, bonds, securitisations etc. have expressed a clear preference for a benchmark that is set in advance and operates in a similar way to Libor. This effectively removes many of the operational and system issues associated with moving to RFRs.

Term Risk Free Rates are one answer to the problem.

Term RFRs

The concept of a TRFR has been around for some time. The SONIA TRFR consultation from 2018 and the ARRC consultations on benchmarks for cash instruments consultations summary have highlighted the utility of the TRFR for the cash instruments.

The argument is that the cash instruments represent ‘real’ requirements for funding and investment which translates into a term issuance and loan market which needs hedging instruments like derivatives.

The other direction, i.e. derivatives will somehow ignite the use of RFR-based cash products, is somewhat more difficult to argue. The introduction of viable and robust TRFRs is regarded as a useful step towards creating real demand for product with maturity greater than 2 years

Summary

Moving the majority of trading in maturities greater than 2 years from Libor to RFRs has not occurred yet. Is this a ‘chicken and egg’ issue? What is needed to make this happen is a real challenge for 2019.

If it is left too late the task of transition from Libor is made more difficult.

TRFRs may be the answer but they are still under development.