I have previously written about the changes to derivative markets and the ways they are accommodating and adjusting to replacing Libor. Trades which reference Libor and other like benchmarks are gradually being replaced with RFR trades across many currencies and products as 2021 draws ever nearer.

In this blog I will look at some recent regulatory developments and the ways markets are adapting. I will also touch briefly on the Term RFRs (TRFRs) again and how these are also developing.

Regulatory developments

On 28th January 2019 Edwin Schooling Latter, Director of Markets and Wholesale Policy at the FCA, delivered an important speech at the ISDA Annual Legal Forum.

For those who missed the live speech, you can read it at this link.

This important speech continues the FCA message on Libor cessation and is well worth the read. In particular, Schooling Latter points out that SONIA volumes are now greater than GBP Libor volumes. However, the duration-adjusted numbers still have Libor leading SONIA: I discuss this a little later in the blog.

The key message in the speech is to transition from Libor to SONIA ahead of 2021 before fallbacks are triggered in derivative, loan or any other contract or product. Waiting for the fallbacks to trigger can have undesirable consequences and should be avoided. Risks (market, operational and accounting) can be substantial unless participants make an orderly move away from Libor before cessation.

As this transition occurs, we should be able to observe more trading volumes and longer-dated SONIA trades in the data sets. This is a likely trend worth watching in 2019.

Changes in the Libor/RFR ratio of trading volume

The FCA analysis considered cleared volumes only. Using CCPView I looked at the last 2 years of data for GBP and USD at LCH SwapClear. I filtered on LCH because, as the 2018 CCP Market Share Statistics blog shows, the vast majority of derivative volume is within this CCP.

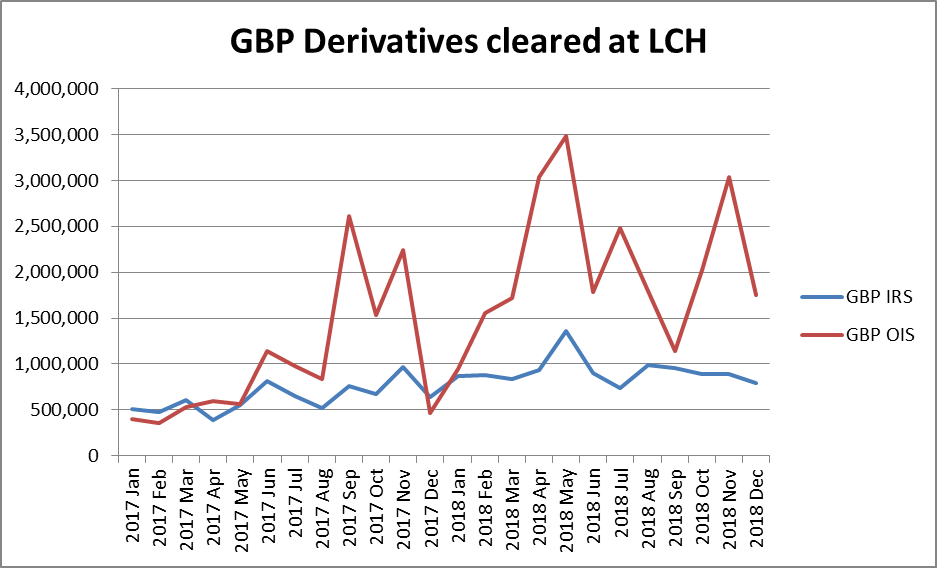

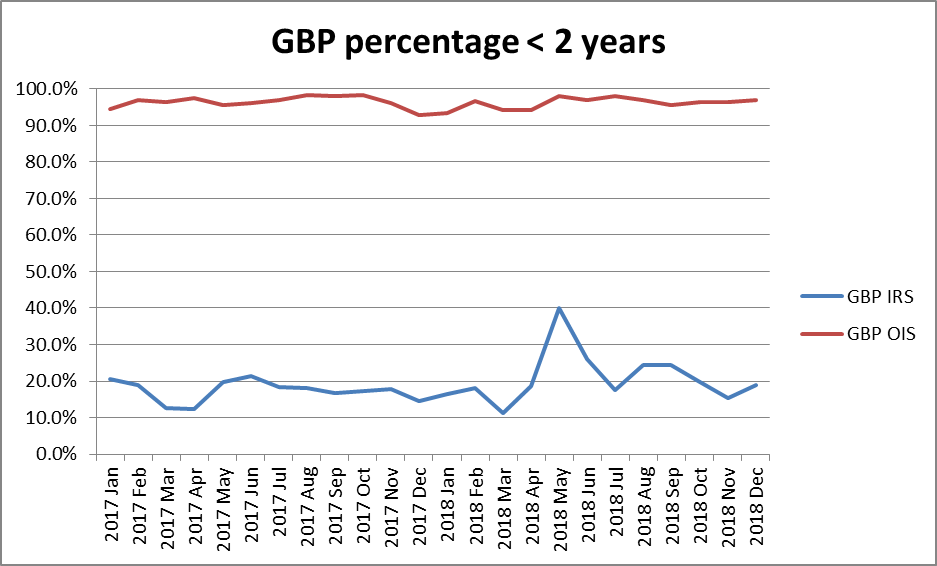

The following charts show the GBP OIS and IRS volumes as well as the percentage of trade volume under 2 year maturity.

The OIS trade volumes are consistently higher than IRS for the past year and have grown significantly. But over 95% of the OIS volume is less than 2 year maturity.

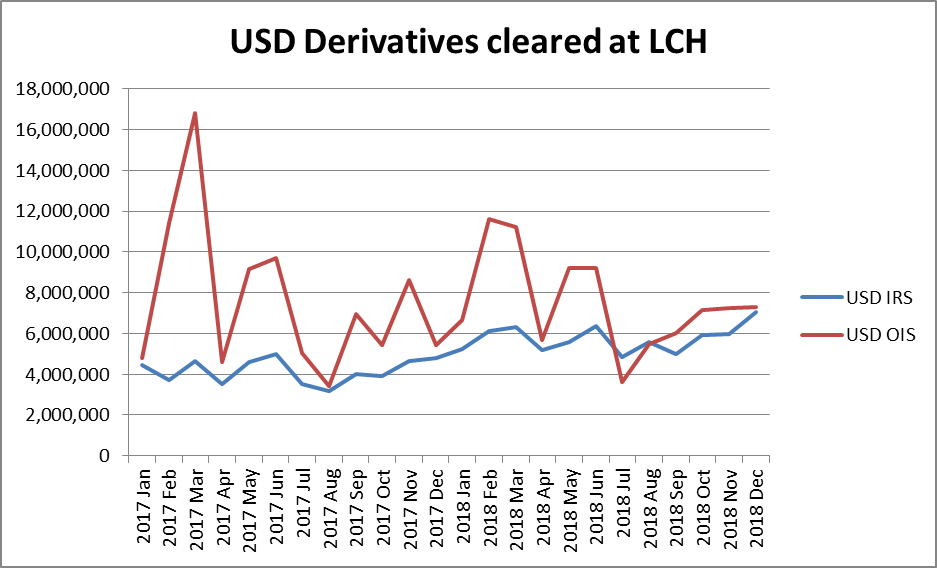

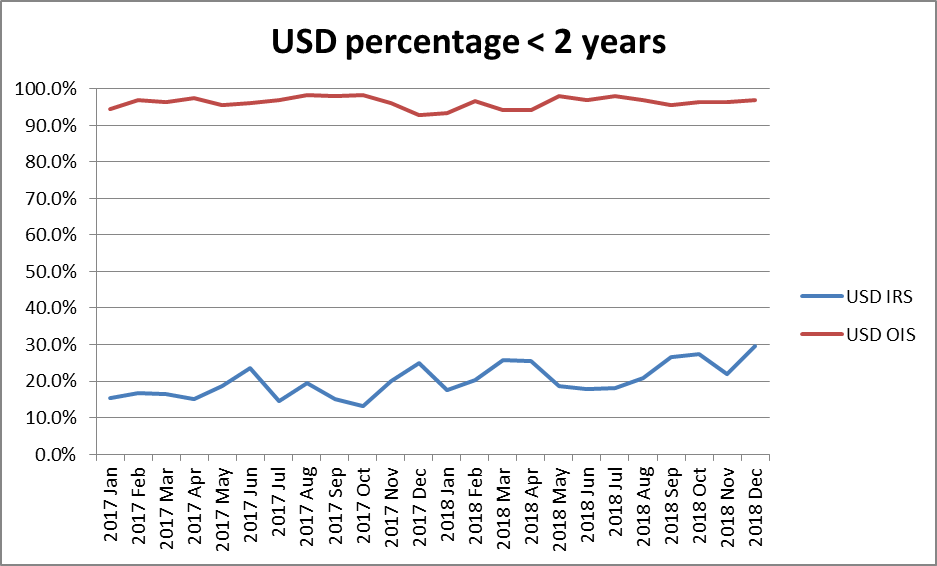

Similar results are shown for USD derivatives in the following charts, in this case the USD OIS are FedFunds and not SOFR, which are only just starting to trade.

Again, the percentage of USD OIS (Fedfunds) traded volume less than 2 years maturity is over 95%. The total volumes of OIS and IRS are comparable with OIS just edging ahead.

Clearly the OIS markets are very liquid but very concentrated in shorter tenors.

For wider participation (buy and sell side) in RFR benchmarks to occur, we will need to see OIS volumes in longer tenors catch and overtake the IRS. The more liquid the longer maturities in OIS trading become, the more likely the wider market will adopt RFR benchmarks.

The FCA does point this out in the recent speech. Liquidity in longer tenors will have to improve to entice buy side participants to switch from Libor to RFRs.

TRFR developments

I commented in my December 2018 blog that recent consultations have highlighted that many participants and customers find TRFRs much more appropriate than the compounded RFR (settled in arrears) approach used in SONIA, FedFunds and SOFR OIS markets.

ICE have started to provide indicative TRFRs for GBP, USD and JPY. These are currently derived from futures, with a place holder for swaps derived. The portal is worth a visit and I expect it will play an important part in making RFR markets much more accessible to participants across many products and markets.

TRFRs are under development and are an important step towards a transition from Libor as recommended by FCA.

I will be watching this development closely over the next few months.

Necessary developments for 2019

2019 will be an important year for the development of new markets and benchmarks based on RFRs. I believe the following will need to happen before a meaningful transition of trading from Libor to RFRs:

- Finalisation of the ISDA documentation for fallbacks for the first four currencies (GBP, JPY, CHF and AUD).

This will create contractual and model certainty for the derivative markets and provide a template for loan and security documentation.

- Establishment of TRFRs to widen the appeal of RFR benchmarks.

Many market participants have expressed a clear preference for a rate set at the start of the relevant period rather than compounded in arrears. TRFRs will have to be based on actual trades or committed bids and offers to avoid the Libor issues of ‘expert judgement’. But this can be achieved as Futures and OIS trading continues to grow.

- Increasing the OIS traded volumes at longer maturities.

Liquidity attracts liquidity: the more trading takes place in longer maturities, the more market participants will find confidence in the RFR benchmarks and accelerate the transition from Libor to SONIA, for example.

The transition from Libor to RFRs has to happen but the market needs some critical developments.

This will be something to watch closely in 2019 and beyond.