- We noticed that the SNB quoted Clarus data at the most recent CHF SARON working group.

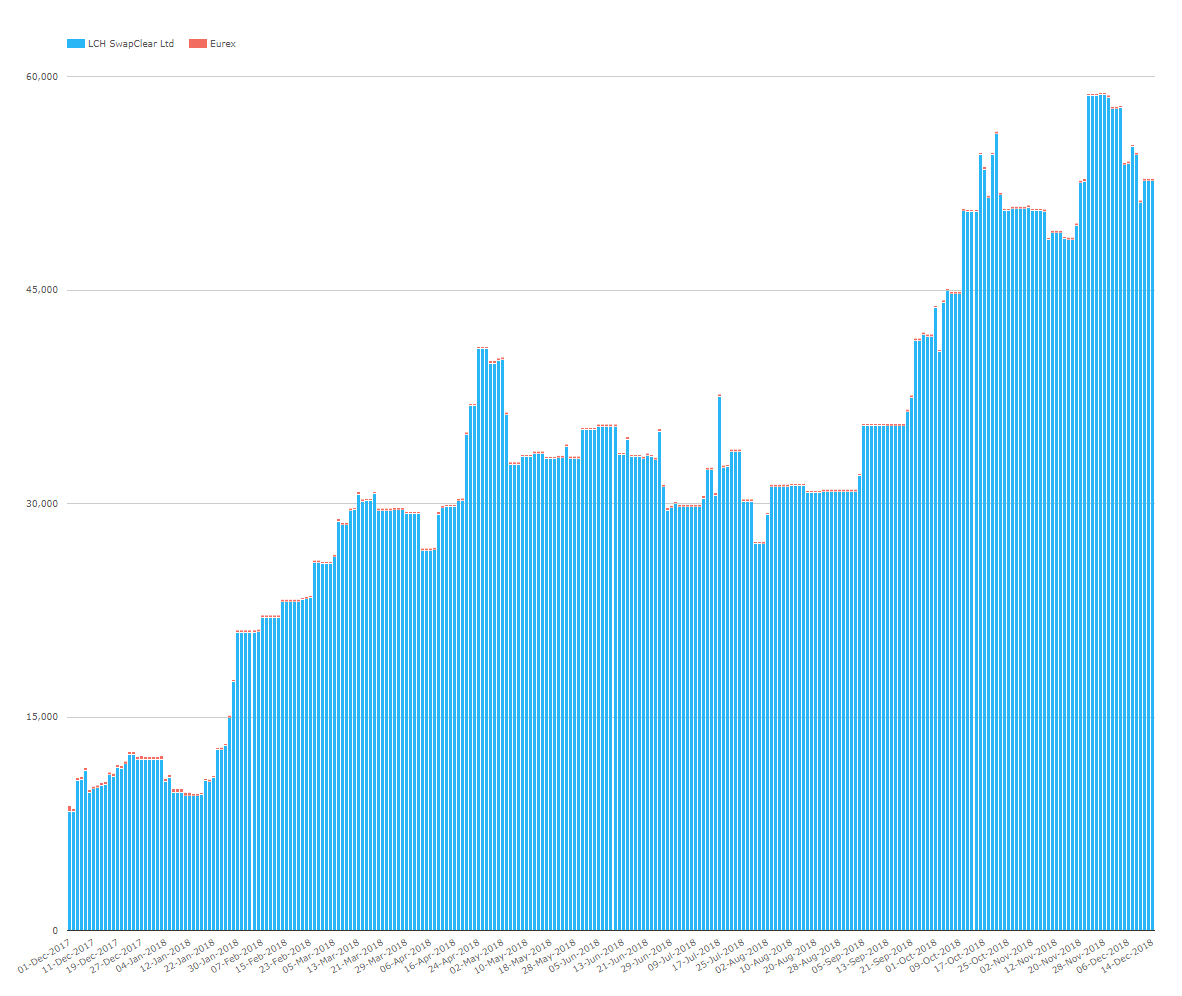

- We show that Open Interest in SARON now stands at nearly CHF60bn.

- Most of this is in short-dated products, less than 2 years.

- We find that 77% of risk is traded in tenors shorter than 2 years.

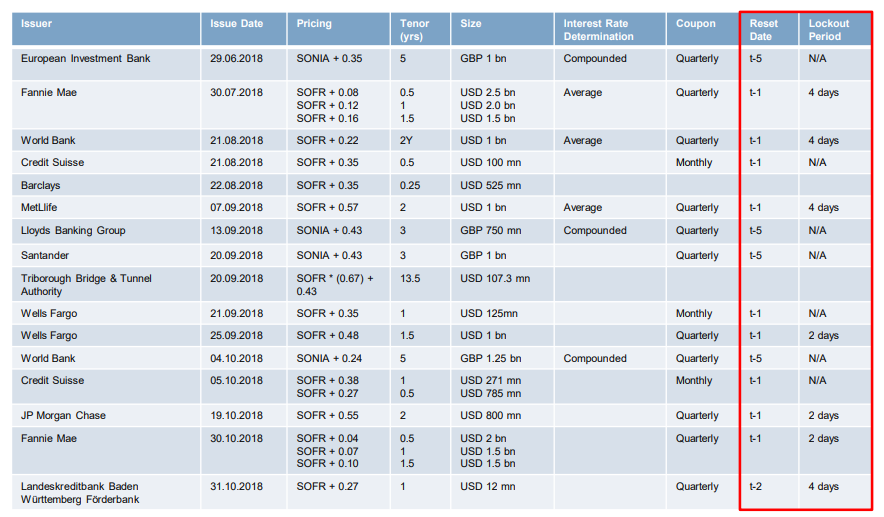

- Markets need to choose a single convention for reset offsets on RFR-linked bond issuance.

I thought I should continue our occasional series on CHF SARON. We last looked back in November 2017, when the demise of TOIS was finally upon us, and the market was busy replacing CHF TOIS swaps with CHF SARON swaps. Fortunately, all of the open interest in TOIS swaps at LCH SwapClear expired just as the old TOIS index ceased to be published.

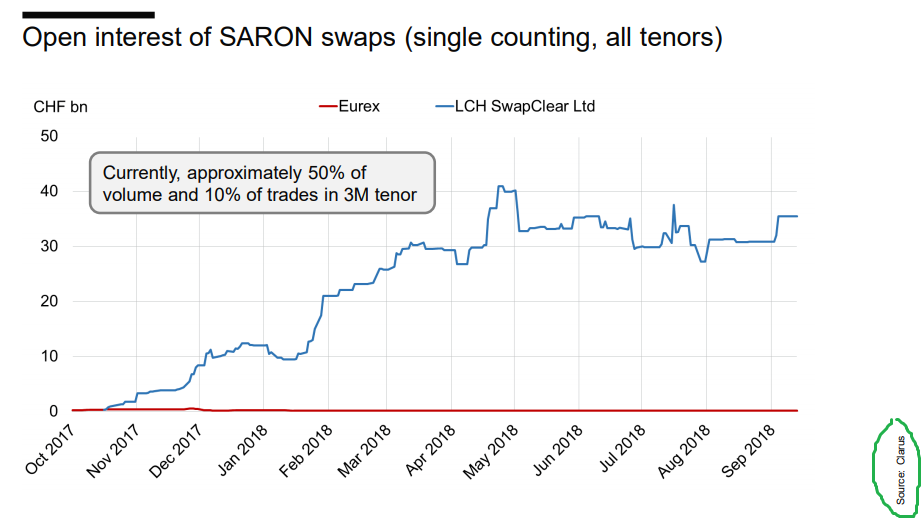

Open Interest in SARON

Since that point, the open interest in SARON swaps at LCH has steadily increased. I saw this chart from the recent SNB Working Group on RFRs, and noticed that they chose a particularly noteworthy source for their data:

The working group was held on 31st October 2018, so I thought I should update the chart using CCPView (which is the source of the above data as well):

Showing;

- Good news! The chart above shows the daily evolution of Open Interest of outright CHF SARON swaps across both LCH SwapClear and Eurex.

- It is continuing to grow, even in the six weeks since the Working Group was held.

- We are now nearly at CHF60bn outstanding.

Background

Before I go on to look at the tenors being traded in CHF SARON swaps, I just wanted to highlight two parts of the SNB Working Group deck that it is worth noting – they’ve done some great work here.

First – As an industry, we have to quickly decide on issuance conventions for debt linked to the new RFRs. It is crazy that we’ve had at least 16 issues versus RFRs, and yet I count SIX different interest conventions for reset offsets (the number of days between the fixing being published and the payment date) and lockout periods. That is just crazy. Settle on a single convention – please! There is a great summary table here:

And for a more up-to-date table, head over to the CME SOFR portal, where there are now 23 issues listed versus SOFR. Let’s settle on a single convention. Standardised markets are better for everyone.

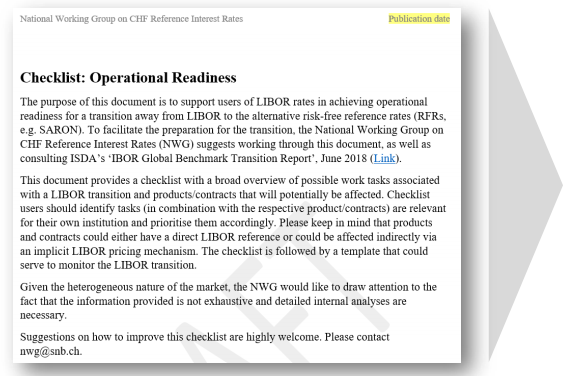

Second – the SNB have published an “Operational Readiness Checklist” for institutions to self-assess where they are with their RFR plans.

Some of this may be obvious, but it’s got to be a useful exercise going into 2019 to make sure that institutions haven’t got any so-called “blind spots” in their project plans.

Some of this may be obvious, but it’s got to be a useful exercise going into 2019 to make sure that institutions haven’t got any so-called “blind spots” in their project plans.

The Working Group also covered much of the content that we have looked at for other currencies. The SNB National Working Group clearly states:

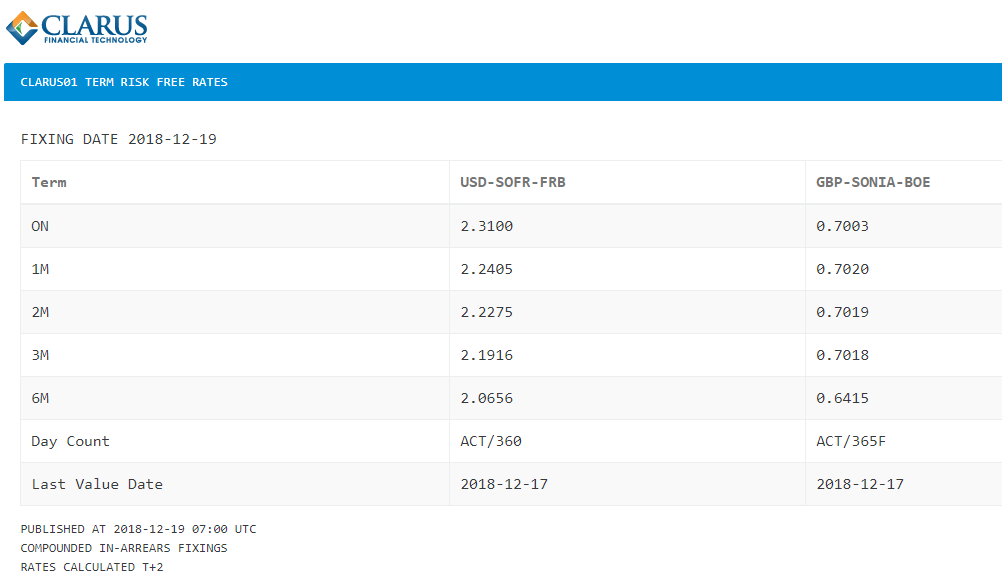

This is exactly in line with our own response to the SONIA consultation on Term Rates and is why CLARUS01 now exists. We are looking to include support for SARON when it is feasible to do so on rfr.clarusft.com.

This is exactly in line with our own response to the SONIA consultation on Term Rates and is why CLARUS01 now exists. We are looking to include support for SARON when it is feasible to do so on rfr.clarusft.com.

(For those readers not already familiar with CLARUS01, it is designed to make the transition away from LIBOR as simple as possible. We provide term fixings in-arrears, which will fit into your existing trade ecosystem without the need to deal with compounding.)

They also cover topics close to our hearts, such as how cashflow uncertainty can be mitigated and fallbacks for old LIBOR contracts. They also mention the work being done on Cross Currency swap standards, which we haven’t yet covered. Let us know if we should take a look at this important market.

SARON Tenor Data

With the overview done, I’d like to present our unique data. We have volume data by Tenor for all swaps cleared at LCH SwapClear. This gives us a great overview of the state of trading in CHF SARON (for example), and allows us to track the transition away from LIBOR.

Showing;

Showing;

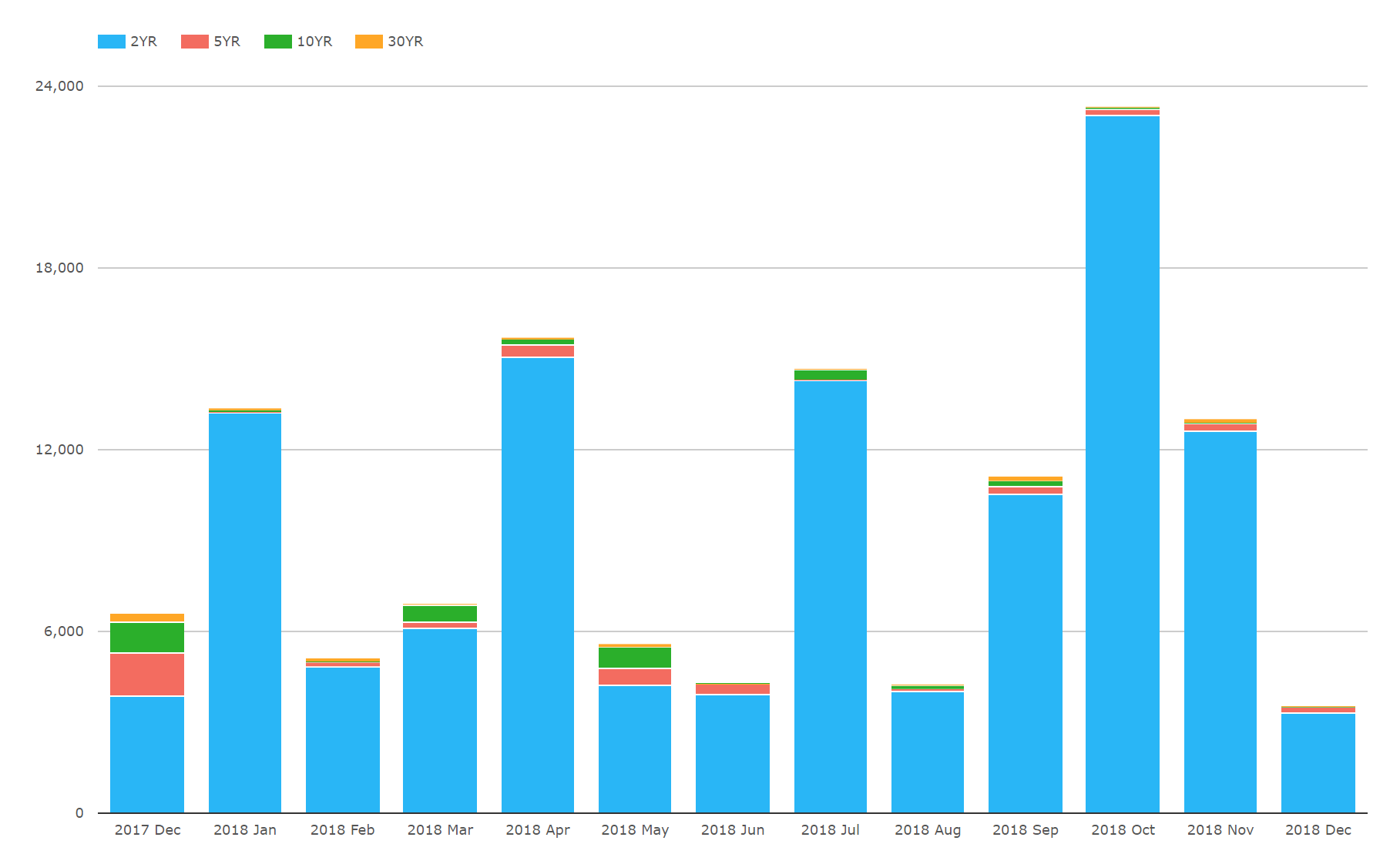

- SARON volumes are shown in notional terms above.

- They are split by 2y, 5y, 10y and 30y tenors.

- As always with notional measures, the charts are dominated by short-dated products.

- Notional volumes can reach almost CHF24bn in a single month.

- Volumes have been pretty volatile. October 2018 was a clear record.

For reference, the same chart for CHF LIBOR activity is markedly different:

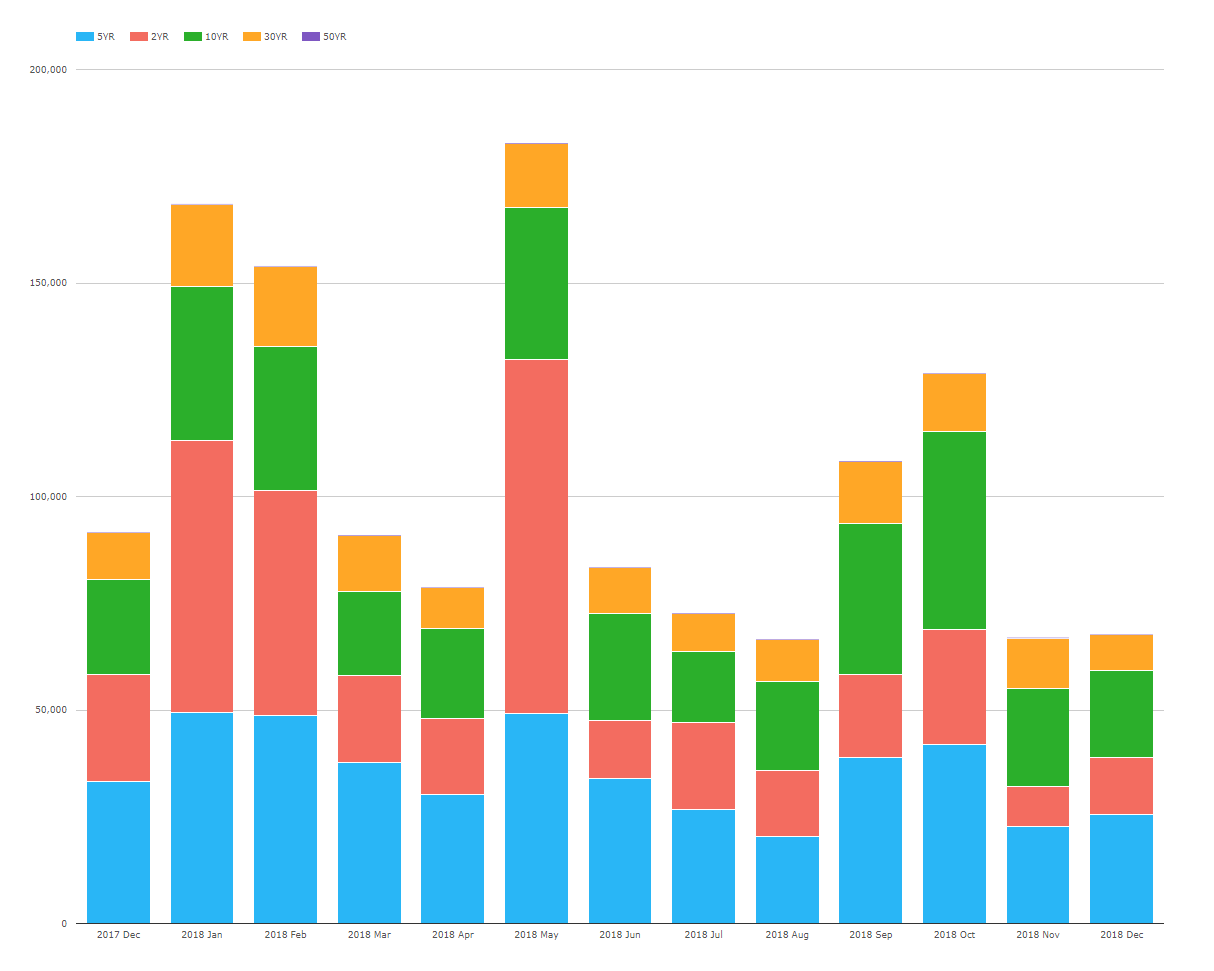

- 5y is the most traded tenor, even when measured in notional terms.

- Activity is far more evenly split across all of the tenors.

- 30y is particularly active – more so than I expected.

- Total notional amounts can reach CHF180bn in a single month.

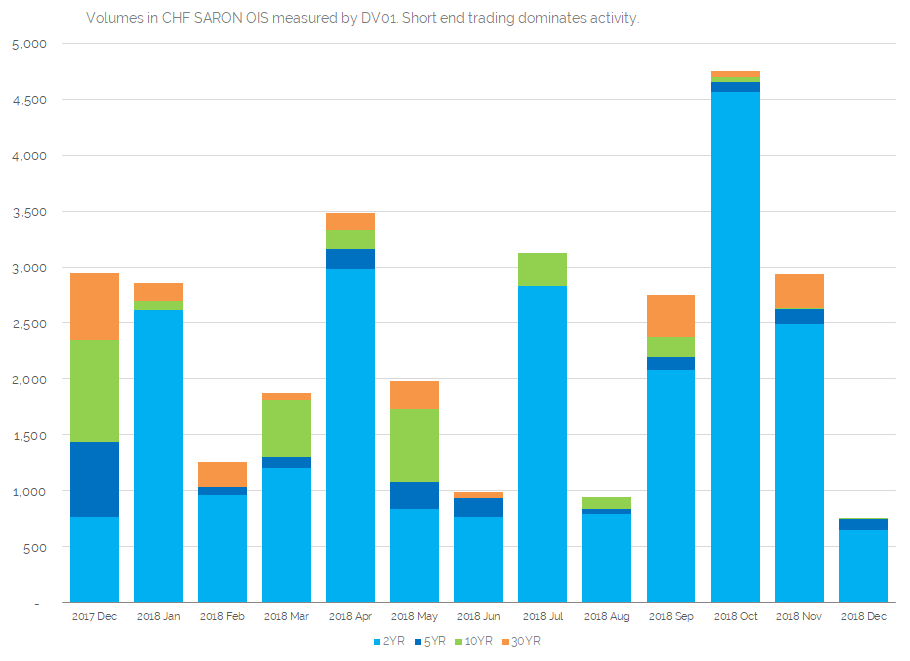

SARON DV01 Data

Now let’s look at the SARON data in terms of DV01. This provides a maturity agnostic measure of the amount of risk traded.

- Even in DV01 terms, volumes are heavily dominated by trading in tenors of 2 years (and less).

- 77% of SARON risk has been traded in tenors shorter than 2 years.

- Overall volumes can be pretty impressive though. October 2018 was the record ever month for SARON trading, when nearly CHF5m of DV01 traded.

- Volumes are volatile, with a more typical month seeing around CHF2.5m DV01 trade.

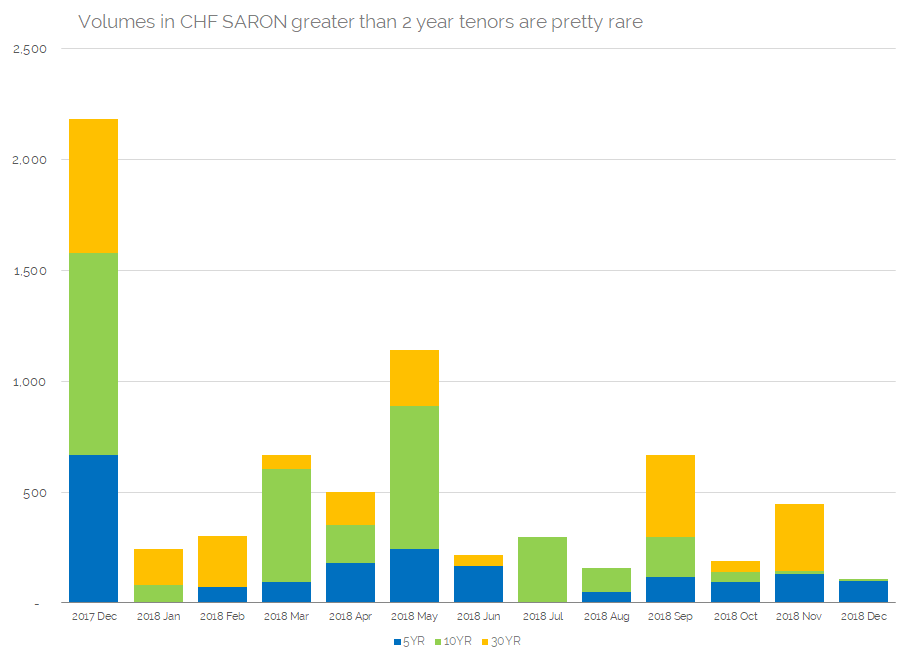

Now let’s look at just the longer tenors – 5y, 10y and 30y. Same data as above:

- Long-dated SARON trading is yet to really take-off.

- We saw decent volumes one year ago, when markets were transitioning from TOIS to SARON. Nearly CHF2.5m in DV01 traded in a single month.

- Since that point, there has only been one month when long-dated SARON has traded more than CHF1m in DV01.

- This long-dated trading needs to evolve and grow for SARON to successfully replace LIBOR in CHF Swaps.

A key aspect that could drive this long-dated SARON trading is the creation of a bond market linked to SARON. That will be a tough ask whilst interest rates are so negative in Switzerland, so we will have to rely on the issuers themselves to swap back out of fixed rate debt into SARON itself.

In Summary

- Open Interest in SARON linked products has reached nearly CHF60bn.

- Most risk is traded in tenors shorter than 2 years.

- We need a market convention for reset offsets on debt-issuance linked to RFRs.

Great summary, John.

Essentially all the Libor trades with maturities beyond 2021 have a Fallback component, so all that “Libor” flow is already implicitly SARON even now.

One thing you might have some insight on is the impact of changing the margin calculation to account for Fallback swaps containing a SARON (or more generally, RFR) component and a Fallback-spread component. How would revaluation in light of historic OIS-Libor spread movements affect the margin amount in the event the clearing houses adapt their models?