Last week at SEFCON IV in NY, CFTC Chairman Gary Gensler in his keynote stated that Swaptions were the largest Interest Rate product not currently being Cleared.

This triggered me to think about updating my last blog of July 2013, see Swaptions Clearing, Why is it Important?

Trade Volumes

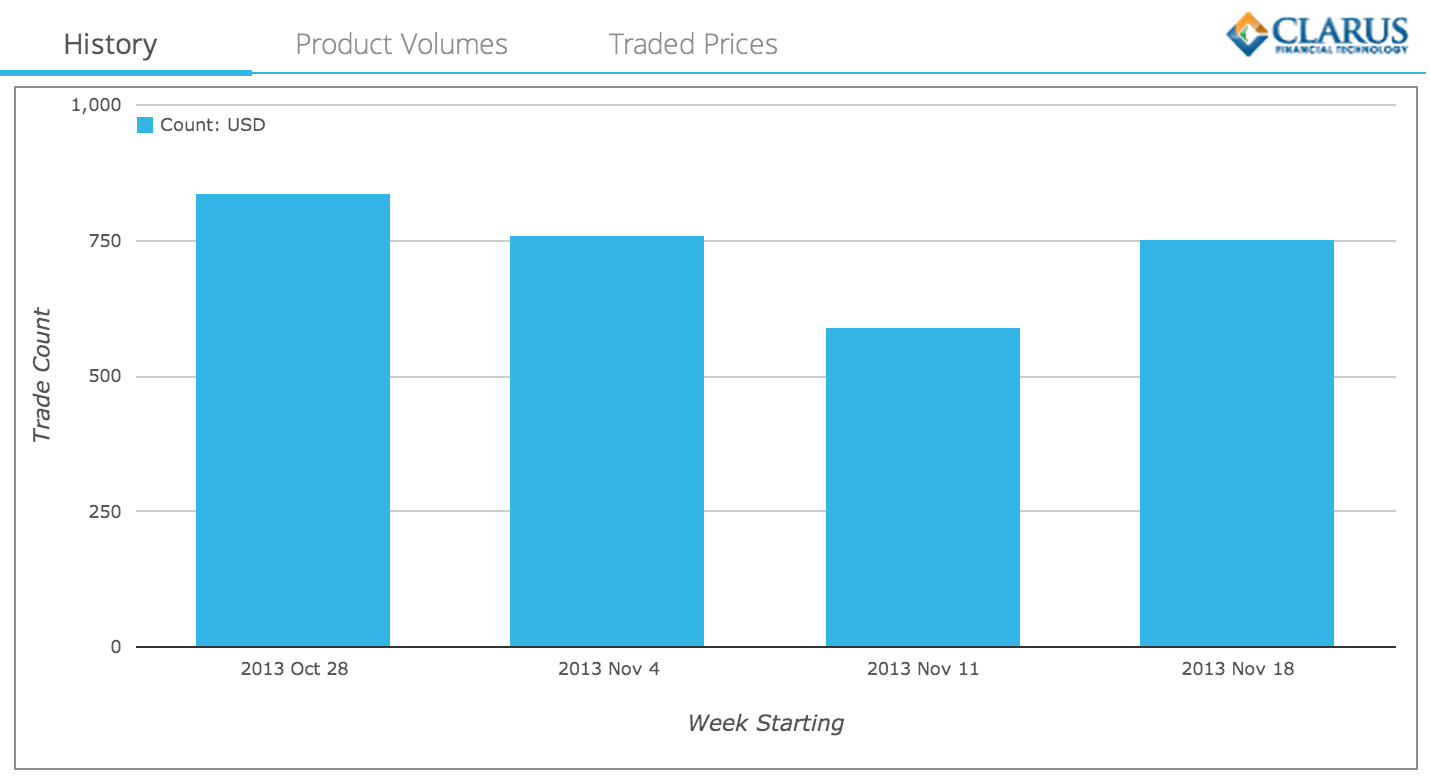

Using SDRView to look at USD Swaptions for the 4-week period starting 28 Oct 2013, we see there are 750 trades a week.

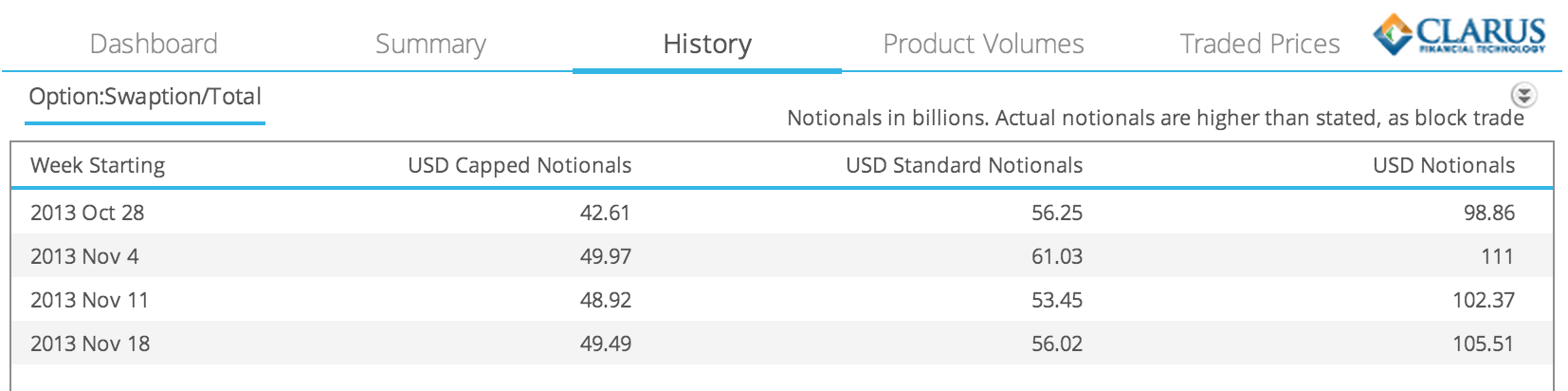

Now looking at the Gross Notional Volume, split by Capped and Standard trades, we see:

From this we can observe:

- That at least $100 billion a week or $20 billion a day is traded.

- The standard notional is much higher than my earlier blog due to the increase in block size rules since then.

- In that blog, we were seeing weekly volumes of $50b and I postulated that they were at least $100b

- We can now say that actual weekly volumes are likely to be even higher, perhaps as high as $150b-$200b a week.

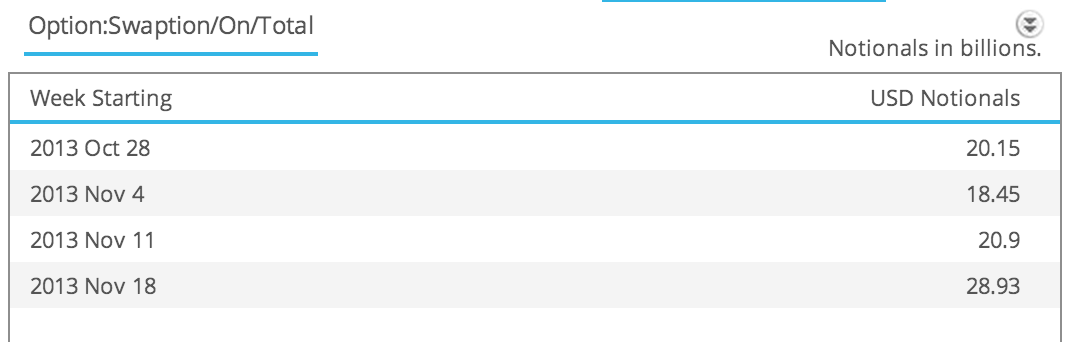

Swap Execution Facilities

It is interesting is to see that even though Swaptions are not Cleared, around 20% of Swaptions trading volume is On SEF.

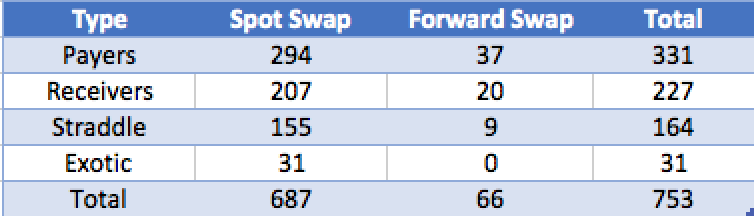

Types of Swaptions

Now lets look at the types of Swaptions that are commonly traded, in an average week (4-8 Nov 2013).

From which we can see that:

- European Payers and Receiver Swaptions on Swaps that start on the expiry plus Spot days are the most common trades

- Straddles (buy/sell of a payers & receivers at the same strike) is the next most common trade

- European Payers and Receives on Forward Start Swaps (aka Mid Curve Options) are the next most common

- Exotics are less than 5% of trades

Straddles

Lets start with Straddles and view these by Expiry on the y-axis and Swap tenor on the x-axis.

From this we can observe:

- 10Y Swap tenor is by far the most common tenor, 90 out of 155 trades.

- 1M, 3M, 6M, 1Y, 3Y are the most common option expirys, representing 118 trades.

- 1Mx10Y and 3Mx10Y are the most common trades.

- Such short expirys are called Gamma trades as they are more sensitive to the swap rate than the volatility.

- 3Y expiry on 10Y and 30Y, as well as 5Y & 10Y expirys on 10Y also trade.

- Such long expirys are called Vega trades as more they are more sensitive to the volatility of the swap rate.

Now what about the Strikes?

Well we know that the dealer market primarily trades ATM Straddles.

If we drill-down on the 10 trades that are 3Mx10Y, we see that this is indeed true, as the Strikes on a given business day are all clustered together at the 3M Forward 10Y Swap Rate.

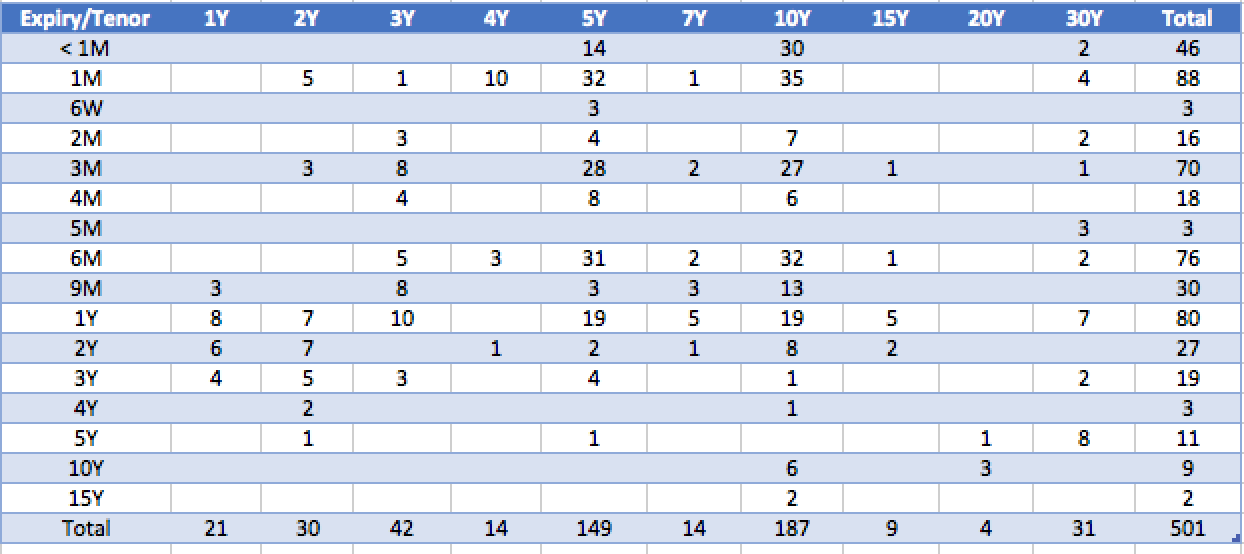

Payers and Receivers

Now lets look at Payers & Receivers traded in the week of 4-8 Nov by Expiry and Swap Tenor.

From this we can observe:

- 10Y and 5Y Swap tenors are by far the most common, with 187 and 149 trades.

- 1M, 3M, 6M, 1Y are the most common option expirys, representing 314 trades out of 501.

- 1M, 3M, 6M expirys into 5Y and 10Y are the most common trades.

- The range of expirys and tenors is wider than that for Straddles.

- There are longer expirys and tenors than for Straddles.

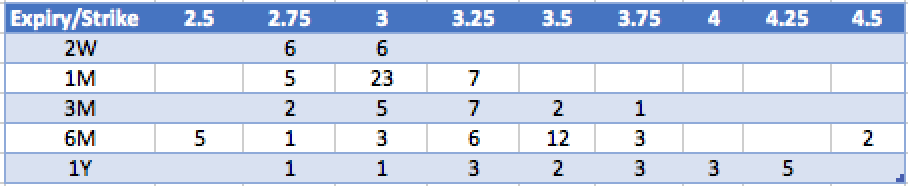

Now what about Strikes.

Selecting just the common expirys for 10Y swap tenor, we see the following:

So very different from Straddles, in that:

- We see a good range of strikes traded for each expiry.

- for 1Y expiry, we have strikes from 2.5% to 4.25%

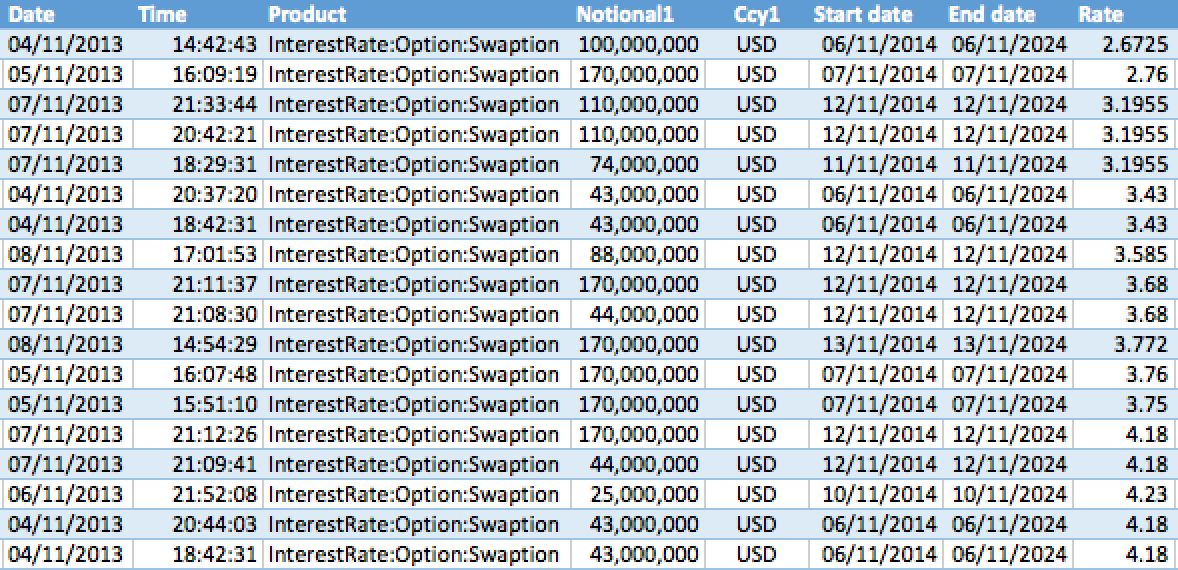

- the drill-down below shows these 18 trades

Summary

Well we can see that we have a wealth of data on Swaptions in SDRView.

The market is large and liquid.

With good volume in European Straddles, Payers and Receivers.

With 1M, 3M, 6M, 1Y being the major expirys and 5Y and 10Y the major swap tenors.

And at least in these we can see that a good range of strikes trade.

So Vol smile and Vol skew should be observable from the prices of these trades.

Final Thought

Swaptions are an important product and one that would benefit from clearing and cross-margining with Swaps.

We know that a number of CCPs are working on launching Swaptions Clearing in 2014 and 2015.

We wish them all the success in this.