What Are GSIBs?

If you need a refresher of the GSIB framework, please check-out our blogs on:

We have recently introduced GSIBView, an app for analysing the scores in more detail. It provides a drill-down into the GSIB components and allows our data customers to analyse particular bank behaviour over time. Check out a run-down of the data and please do contact us for a free trial.

What is Window Dressing?

The best definition I found was from an ECB Working Paper:

Window-dressing is the practice by which regulated entities adjust their activity around an anticipated reporting or disclosure date, with the objective of appearing safer or, in the case of the G-SIB framework, less systemically important to the regulator, supervisor, or market participants. The G-SIB assessment is conducted once a year, and the calculation of G-SIB scores relies on year-end data. Thus, banks involved in the exercise could have an incentive to reduce activities affecting the G-SIB score in the last quarter of the year, with the intention to reduce additional capital buffer requirements arising from the G-SIB framework.

ECB Working Paper Series No 2298

The whole paper is worth a read: “Behind the scenes of the beauty contest: window dressing and the G-SIB framework“. It begins by stating;

This paper illustrates that systemically important banks reduce a range of activities at year end, leading to lower additional capital requirements in the form of G-SIB buffers. The effects are stronger for banks with higher incentives to reduce the indicators, and for banks with balance sheet structures that can more easily be adjusted…. a reduction in the provision of certain services at year-end may adversely affect overall market functioning.

ECB Working Paper Series No 2298

In particular, repos (repurchase agreements) are a particularly short-dated activity that can readily be scaled back at reporting dates. They are typically overnight, and certain studies show that “roughly 10 percent of the overall tri-party repo market vanishes at the end of each quarter (when banks have to report their capital ratios).”

The Repo Market

I’m sure that our readers have seen various articles about how GSIB capital requirements, along with the Leverage Ratio, have negatively impacted repo markets. Remember that as we transition to SOFR, we will all be repo traders eventually!

A quick google search shows plenty has been written about it:

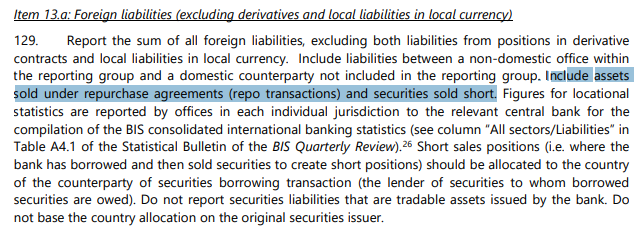

However, when I referred back to my previous blogs on GSIB, I couldn’t see where repo activity was included in the GSIB framework. I therefore went back to the original BIS definitions and found the following:

This “Item 13a” falls within the GSIB category “Cross Jurisdictional Activities”.

The ECB paper also suggests that repo activity will impact the Interconnectedness and the Size categories of the GSIB scores as well.

Since repos often occur between financial institutions and represent a considerable share of crossborder transactions, they have an impact on the size as well as the interconnectedness and the cross-jurisdictional indicator of the G-SIB framework.

ECB Working Paper Series No 2298

GSIB Data

The ECB paper goes on to present compelling statistical evidence that banks do indeed engage in window dressing, whereby GSIB scores are seen to decrease into Q4 before rebounding in Q1.

Rather than replicate that analysis, which is based on European regulatory filings from 2014-2017, I thought I could present more recent data from our newly launched GSIBView data.

We are able to grab quarterly US data. This enables us to investigate whether we also see these dips in GSIB scores around year-end for US banks.

Last week, the December 2019 figures were published here. GSIBView is now updated with these end of year scores for the US banks. I’ll have a look at the overall scores next week in more detail:

Cross-Jurisdictional Indicators

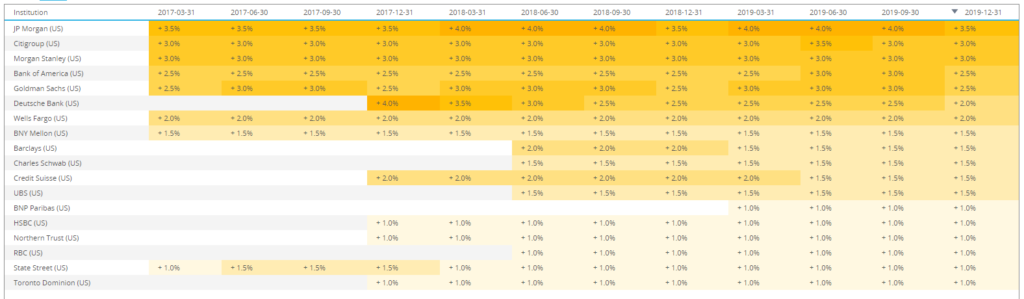

Our GSIBView app allows you to drill-down into the detail of each score. We can then track the ups and downs of these indicators over time. Looking back from 2018 we see the following for GSIB banks in terms of Cross-Jurisdictional activity:

Showing;

- The quarterly GSIB value of Cross-Jurisdictional Indicators per US bank since September 2018.

- Any value that decreases by more than 2% is shaded blue.

- Any value that increases by more than 2% is shaded orange. The darker the shading, the larger the change.

- We can see that among the largest 10 GSIBs in the US (down to Barclays US arm in the list), 6 of them decreased their indicator scores into year end 2018/2019 by 2% or more.

- This behaviour was even more widespread for year end 2019/20 where 11 of the US GSIBs decreased their scores by more than 2%.

This doesn’t mean that the 2019/20 scores were lower than the previous year-end. In some cases (Citi, MS, UBS) the end 2019 scores were higher than the previous year, despite decreasing from their previous quarter.

Rather, we see clear evidence that these indicator scores bounce back in Q1 of each year:

- JP Morgan show an indicator score of 141 in September 2018, which decreases to 128 in December but immediately bounces back to 145 in March 2019.

- This type of “V” is replicated by Goldmans, BoA, MS, Credit Suisse.

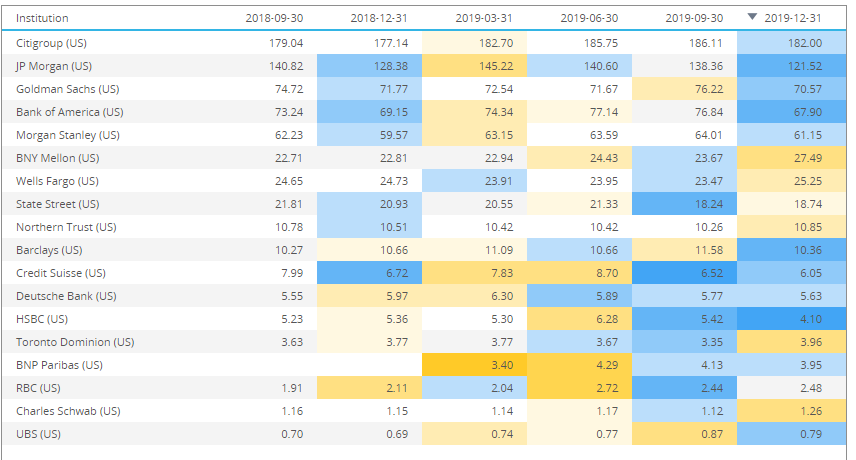

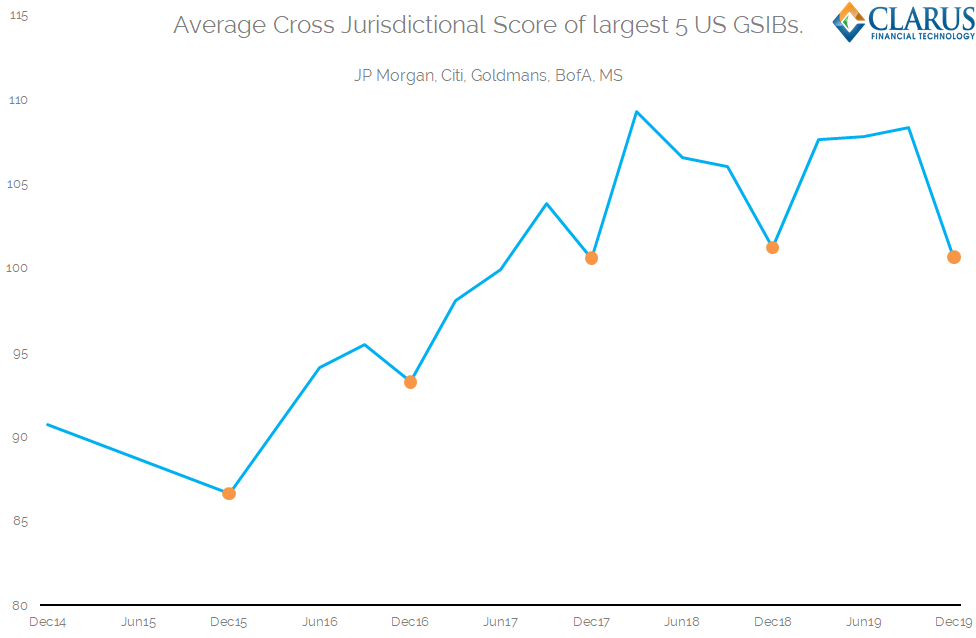

In fact, this behaviour seems to have been ingrained for quite some time. Since 2014, we can see a systematic reduction of the Cross Jurisdictional indicator at year-end for the largest 5 US GSIBs:

Other GSIB Indicators

Our users of GSIBView can now analyse the other components impacted by repo – Interconnectedness and Size – to see if this behaviour is replicated there.

If you want to perform the analysis yourself, please contact us for a free trial of GSIBView.

The idea is to make these indicators more transparent. The combination of these blogs to explain the indicators and an extended time-series of data should allow all market participants to better understand the GSIB regime.

In Summary

- There is strong evidence that banks conduct window dressing at year-end reporting dates to minimise their GSIB scores.

- One particular activity that is curtailed around key reporting dates is repo due to the fact it is short-dated and directly impacts GSIB scores.

- GSIBView allows us to identify and analyse the extent of this contraction in repo activity per bank.