The conversation seems to be heating up again about the topic of anonymous order books for the OTC swap market. The topic has been out there for well over a year, however really had not been in the press or acknowledged by the CFTC until SEFCON V in November 2014. It remains un-addressed.

The CFTC did however provide some language that they were thinking about it. I will not bother to go back to the transcripts, but I left thinking this was squarely on their radar.

I’d like to define the issue and then look at some data to see how we might go about adopting a change.

THE ISSUE

So here is the issue as I see it.

The CFTC interpreted the G20 & DFA objectives as moving OTC swaps to a futures-like world, complete with “exchange trading” and clearing. As such, when they wrote rules for “exchange trading”, these SEF’s (the “exchanges”) required an order book (like futures), and allowed off-venue block trading (like futures) and after some deliberation, also catered for RFQ.

If you follow the Clarus blogs, you’ll know the On-SEF trading of swaps has plateaued. The most optimistic perspective is USD vanilla swaps, where generally 50% – 60% of swaps trade on-SEF every month. The balance of trades done off-SEF are either products that are not required to be traded on a SEF (known as “non-MAT”), or things like block trades.

And once you go beyond USD, the amount of EUR, GBP, and other products trading on-SEF is quite low. Hence the “exchange trading” part of the requirement has not been adopted as vigorously as many had wished.

The issue, however, is not the lack of volume on-SEF, rather it is the behavior of the SEF-executed volume. It would seem that the inter-dealer market is still traded only on the IDB-run SEFs (what Clarus SEFView categorize as “D2D”) and the client market is still traded only on the legacy “client” SEFs such as Bloomberg and Tradeweb (what Clarus SEView categorizes as “D2C”).

Clients trading on the “client” SEFs are trading primarily via name-disclosed RFQ to a list of banks. Dealers are trading on the IDB SEFs generally over voice, although there does seem to be a growing portion of electronic order books on IDBs, yet this remains the minority. All of this (voice, RFQ, order book) is fine by the letter of the law.

But the CFTC envisioned “all-to-all” trading, where Bob’s Hedge Fund should be able to trade anonymously with JP Morgan in a 5-lot equivalent.

So if the IDB’s have an active order book, and that’s where the banks are transacting in wholesale prices, why doesn’t Bob’s Hedge Fund just go join up at the SEFs run by ICAP, Traditions, Tullets, and BGC? Well, GFI did encourage just that last year, and as you can see they are no longer in my list of IDBs! (Joking aside, as the BGC-GFI buyout had nothing to do with that incident).

What seems to happen is banks don’t want Bob trading with them in the interdealer market. Banks trade with Bob elsewhere, where the protocols allow them to see its Bob asking for a price in a 5-lot equivalent (an RFQ on a D2C SEF).

There are plenty of analogies for this behavior. If you live next door to the Ford factory, can you just stop in and buy a truck at wholesale price, and not pay all the dealer fees that get generated? I don’t think you can.

Oddly however in SEFs, I believe there is in fact nothing stopping Bob from joining any of the IDB SEFs. I think as long as he signs up, agrees to terms, and very likely pays some monthly fees (that all SEF members pay), he’s in and trading. There no longer seems to be any issue with technology, self-clearing, etc.

The issue is when Bob does his first trade. As soon as the trade is executed, his name is revealed to the other side. Let’s assume that other side is Bank ABC. Bank ABC has various other relationships with Bob, handles funding for Bob, gives Bob a bunch of free services, all because Bob is – or in this case was – a client.

Not to mention that Bank ABC then writes an email to their IDB with a subject line “Dude, what’s Bob doing here”.

WHAT MIGHT CHANGE

So the debate is that last step. The order book doesn’t need to change function. The legal paperwork doesn’t need to change. It’s just that last legacy OTC swap remnant of disclosing who you traded with, that is the debate.

WILL THIS WORK

While I can see how removing name-disclosure would work in principle, I’d have to think that, at least in the context of the IDB SEFs, the monthly fees for IDBs would be prohibitively high, at least in my example of Bob’s Hedge Fund. As you move across the spectrum from Bobs Hedge Fund to PIMCO, the dynamics might change.

Alas I will not debate whether it will work. I think it’s going to happen, and I’d like to prognosticate on how the CFTC will go about this.

PHASING OR TRIALS

I think there are two possibilities for how this change to an anonymous order book gets started.

- Phases. Most everything the CFTC have done has been phased in over time, with the only debate being who/what goes first.

- Trial. The other option I’d suggest is a trial. I recall the SEC is trialing / has trialed some of their proposed rules, most recently on minimum increments for illiquid names.

Technically the approach will not matter, as in both cases you still have to find some sub-set of products that you phase in first / single out for a trial. Only because the CFTC seem to phase in everything (have they ever trialed anything?), I’ll go with the first option.

But like I say, what do you single out to phase in first? Let’s look at some headline data to see if there are any obvious answers.

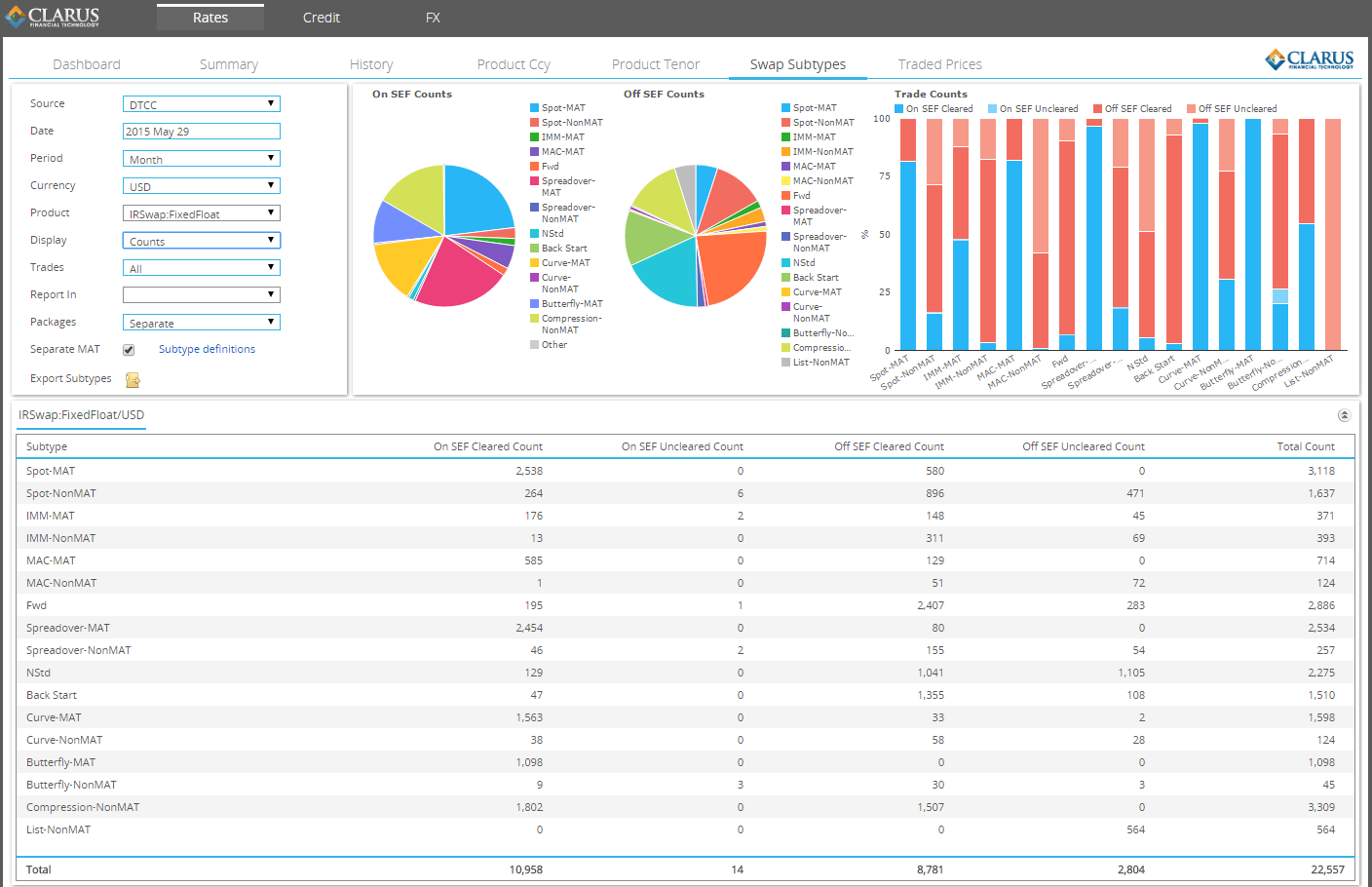

Let’s look at USD Fixed/Float swaps. Clarus SDRView enriches the trade data here to classify each trade as spot starting, fwd starting, IMM, MAC, etc. It further enriches trades so we can tell those that belong in packages, and lastly classifies them as MAT or not.

Here is May 2015 USD data, in trade count:

We can see there are over 22,000 USD Fixed/Float trades reported in May. Of these, roughly 11,000 were On-SEF. There is that 50% On-SEF figure we’re used to seeing. Surely that universe is too large to start with, so we need to find something smaller to start with.

Of course you need to rip out non-Order-bookable products like list/compression trading. And while you are at it, all packages such as curves, butterflies and spreadovers should be removed (heck it took them a while to be required to be traded on SEF in the first place). That leaves outrights. In the universe of outrights, you then have MAC, IMM, and other Fwd start swaps.

How about non-MAC IMM swaps? We can see 371 MAT’d IMM swaps traded, of which 176 were On-SEF (the balance likely as blocks). This 176 trades is a nice small universe (under 1% of all USD swaps).

Looking further, there were 714 USD MAC swaps traded in May, 585 of them On-SEF. Perhaps this, representing ~2.5% of trade activity, is a good place to start? Right sort of magnitude. The further benefit here is the anecdotes I’ve heard from the faster-money businesses that if they were to start trading swaps, they’d start with a highly standardized product like MACs. And of course they are accustomed to trading in order books.

Or do you step up to the universe of outright, Spot starting swaps? We can see 3,118 of these traded, accounting for ~15% of trades in May, of which 2,538 were traded on SEF. (Again the balance should be largely blocks).

So that ~10% of the USD swaps market might be the place to start.

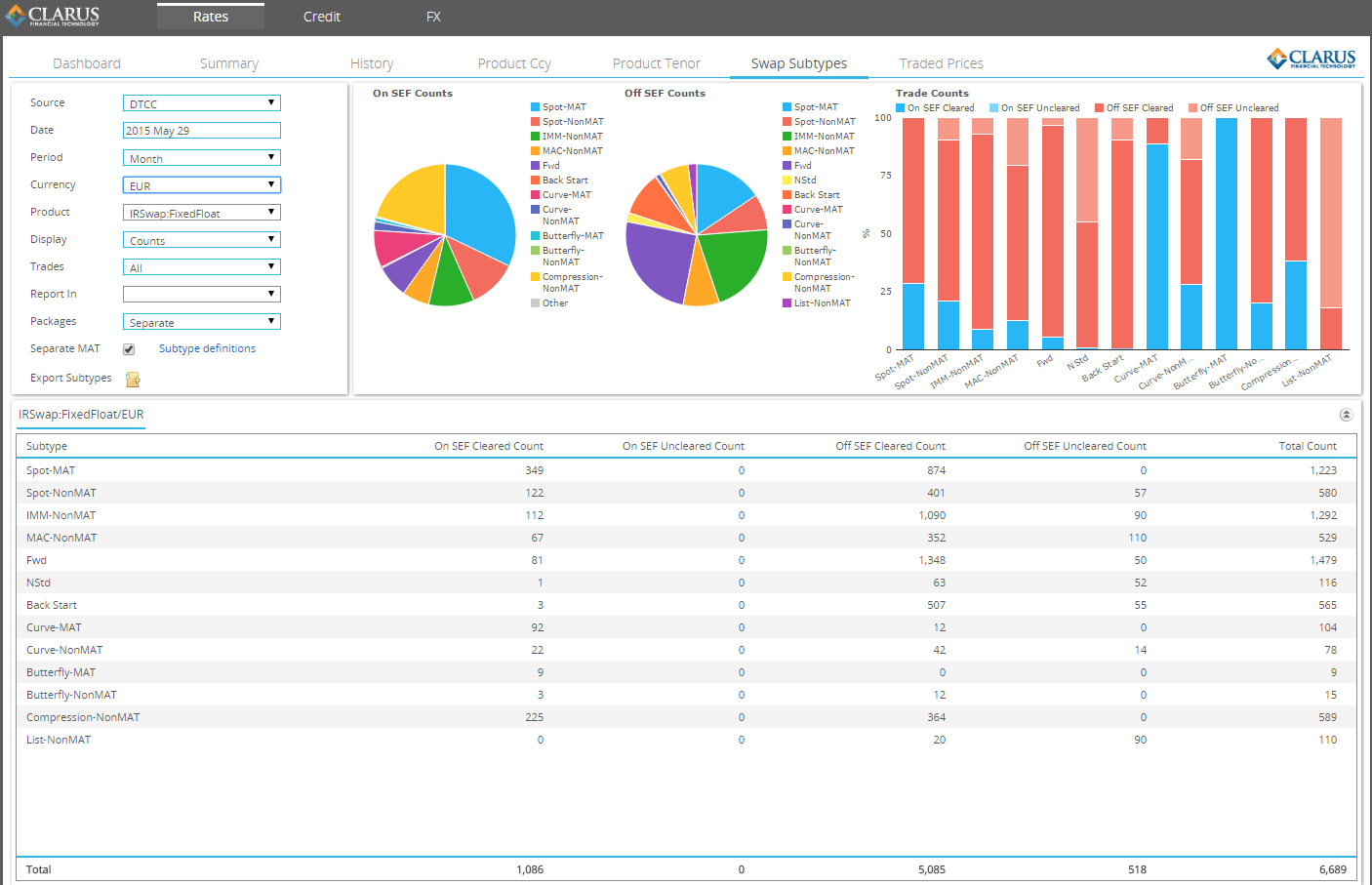

Or maybe there is some worry that we should not tinker with USD swaps, but rather start with another MAT’d currency’s set of products. The list here is short, just EUR and GBP. Let’s look at EUR:

The universe of trades here is much smaller, at just over 6,500 trades. And the number of MAT’d EUR Spot starting swaps traded on-SEF is roughly 5%, half that of USD spot starting in percentage terms.

Unfortunately, EUR MAC swaps are not MAT, as that might be the best place to start, as there is a healthy 529 total MAC swaps traded in the month, meaning MAC represents a good portion of EUR trading.

MY BET

OK, so I won’t prognosticate. Rather, I will go with my heart and declare the most exciting thing we could see is if all MAC swaps require no name-disclosure. Most exciting as I believe you’d see interest from some new parties, and those new parties would not need to get their heads around the ugly nuances of bespoke swaps (such as line items & compression).

Of course, the opposing force here is I can’t say whether there are any active MAC order books at the moment (I fear not). So this might just end up killing any chance of dealer order book liquidity in MAC swaps. Any initiative might require a product where there is a semblance of an order book to begin with. In which case we’d need to step up to outright spot starting swaps.

However it’s done, or even if it is done, remains to be seen. But we need some excitement around here!