Swap Execution Facilities (SEFs) and Swap Data Repositories (SDRs) mean that it is now possible to implement effective Trade Surveillance in the OTC Swaps market and to do so in an analogous manner to the Futures market.

Swap Dealers or Major Swap Participants can and should compare their executed trades with the trades reported in the market, a role that usually falls to a Surveillance manager in the Compliance department.

In this article I will look at post-trade surveillance, both historical and real-time.

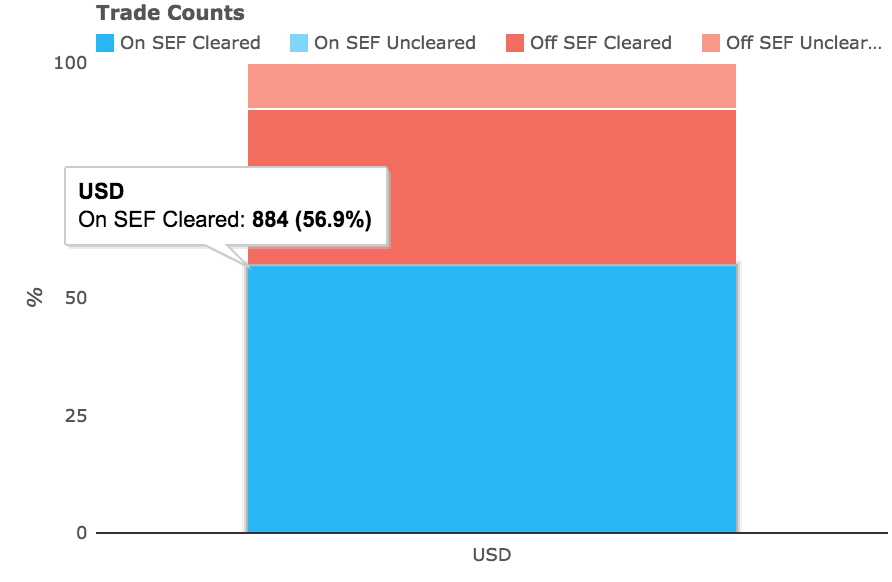

USD Swaps on March 9, 2015

Lets start with the trades reported to US SDRs on March 9, focusing just on USD Fixed Float Swaps.

Which shows that out of the 1,553 trades reported to DTCC and BSDR, 884 or 57% were On SEF Cleared.

So is it as simple as starting with these and identifying which are our trades and comparing their prices and notionals with the rest?

Unfortunately not for a few reasons:

- Unlike Futures there is no single instrument identifier (e.g. EDH15), but 40+ fields that we need to use to determine what specific type of trade it is.

- Even when looking only at what SDRs term “Price Forming transactions” we need to separate out Package trades such as Compressions, Curves and Butterflies.

- Cancel and Correct transactions need to be accounted for.

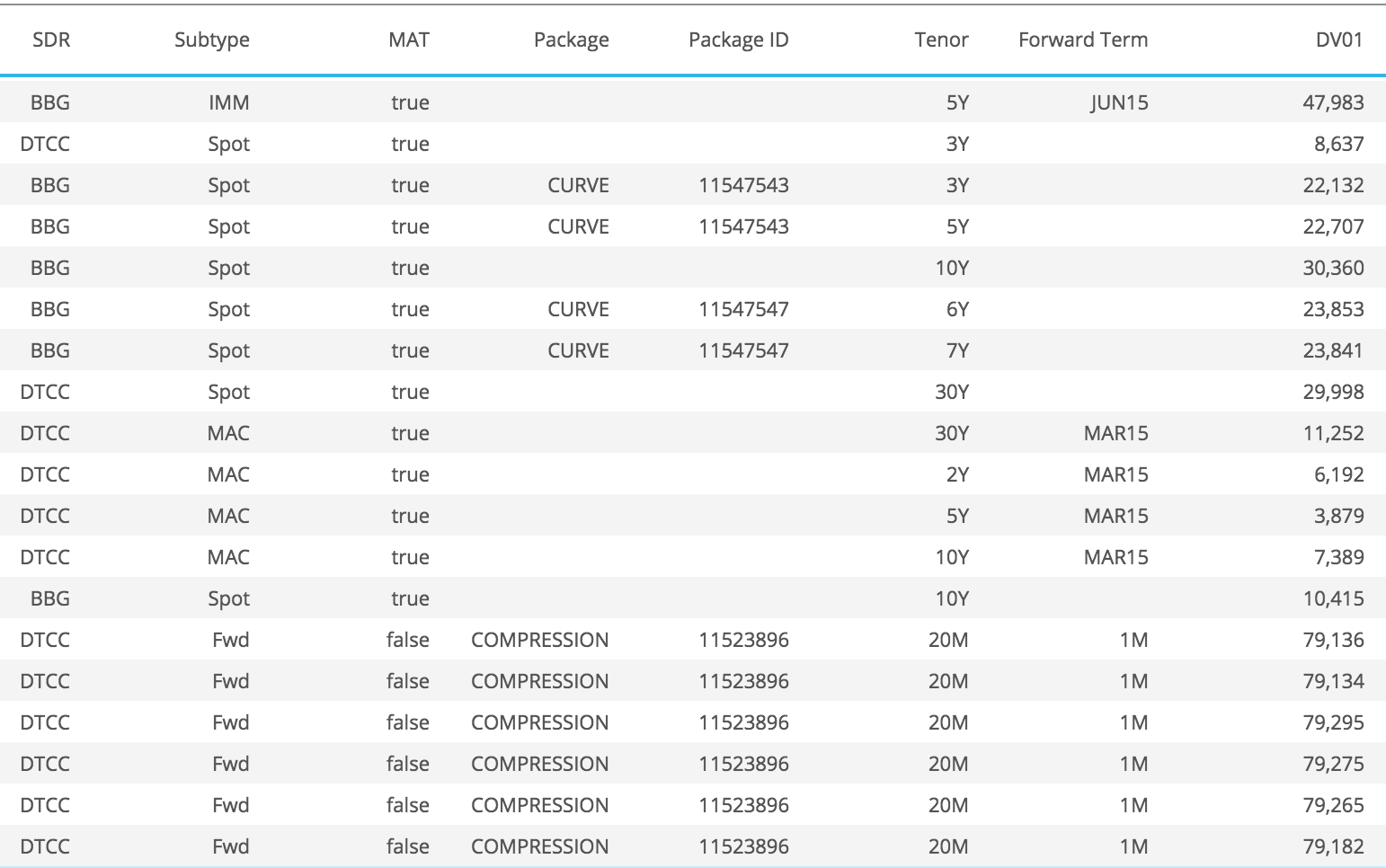

Data Enrichment in SDRView

In SDRView Res we now enrich the SDR public dissemination data with additional fields to address precisely these issues. In the drill-down we show the enriched fields below:

- SDR source, one of DTCC or BBG

- Subtype of the Swap, e.g. Spot for the standard trade or IMM or MAC or Fwd for others.

- MAT as true or false to signify Made Available to Trade

- Package as Compression, Curve or Butterfly

- Package Id to link the trade legs of a package

- Tenor to identify 5Y trades rather than have to use the maturity date

- Forward Term to identify IMM, MAC and Fwd Start term.

- DV01 as a useful risk measure

All of which make our task much easier.

For example if we know we have executed some vanilla 5Y Swaps on March 9, we can now extract just these from SDRView and compare the execution times, prices and notionals of our trades against the market at large:

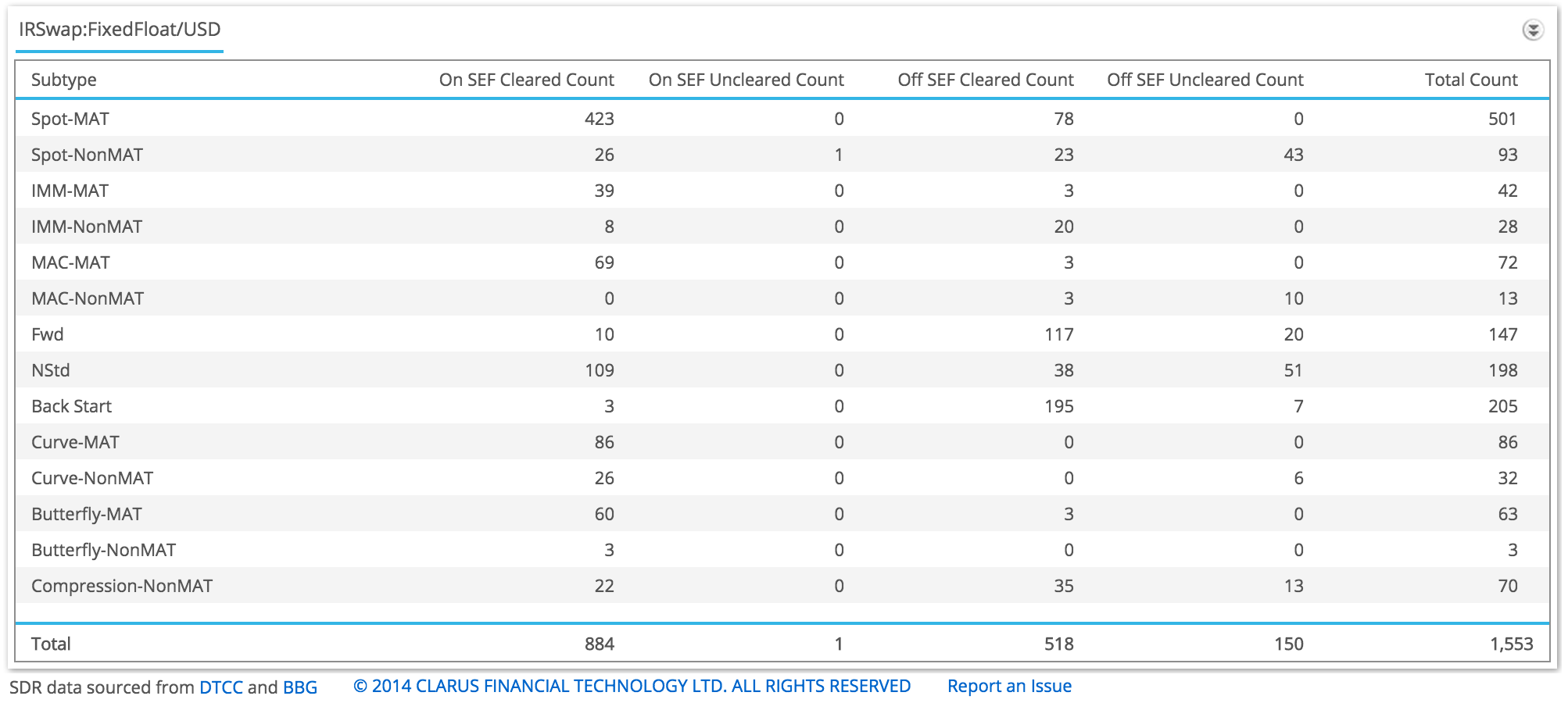

Swap Subtypes

What does the data enrichment do to our population of 1,553 trades? The table below shows precisely this.

- So only 423 out of the 884 trades that are On SEF are standard spot starting vanilla trades in MaT tenors

- These are the ones we should first focus on as it is likely we will find comparable trades to our own

- IMM and MAC with 47 and 69 are also interesting assuming we trade these

- Curves and Butterfly with 112 and 63 legs (56 and 21 packages) are also interesting for comparisons.

But after these types a simple price comparison is not practical or possible.

For Forwards or Non Standard trades we are unlikely to find comparable terms to our own trades and consequently cannot do a meaningful price or size comparison. This means the only course of action is to calculate a fair price for these from the standard trades. Which is a process we are currently working on using the common NPV measure.

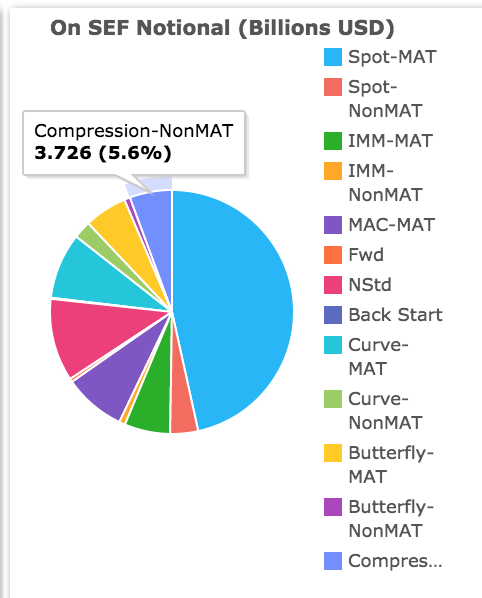

An interesting view is one of gross notional by Swap types and Packages for the same March 9 date.

Historical and Real-time

Surveillance should be performed daily using all todays trades, historically looking for patterns of behaviour and in real-time with alerts for possible off market transactions.

US SDR public dissemination means that most trades are available with a few minutes of execution and as the market is characterised by large trades in low frequency, this is a perfectly adequate time frame for real-time surveillance.

Our SDRView API provides a programmable method to monitor intra-day trading activity for Swaps.

Summary

There are many uses of the SDR public dissemination data.

One of the most interesting is Trade Surveillance.

However this is not easily done on the raw SDR data.

SDRView now provides enriched data.

This serves to isolate packages and differentiate between types of Swaps.

Which makes trade surveillance practical and possible.

Swaps trading firms should now be able to improve their existing surveillance process.

Another benefit resulting from the whole markets’ investment in real-time trade reporting.