Better than an Oasis b-side, we thought what better time to talk about volatility than just after a payrolls report that saw 10 years move by over 12bp? Will the Fed in action be good for the SEF industry?

I think we all know the supposition here. Volatility leads to increased trading, increased trading leads to higher volumes, higher volumes are good for IDBs and everyone in a transactional-based role has a great time. We see frequent references to volatility in both IDB results (such as Tullets recently) and bank results (Citi last quarter for example). So this raises a simple question – can we work out what this relationship is, beyond a simple theory that an increase in one leads to an increase in t’other? Let’s look at the data so far.

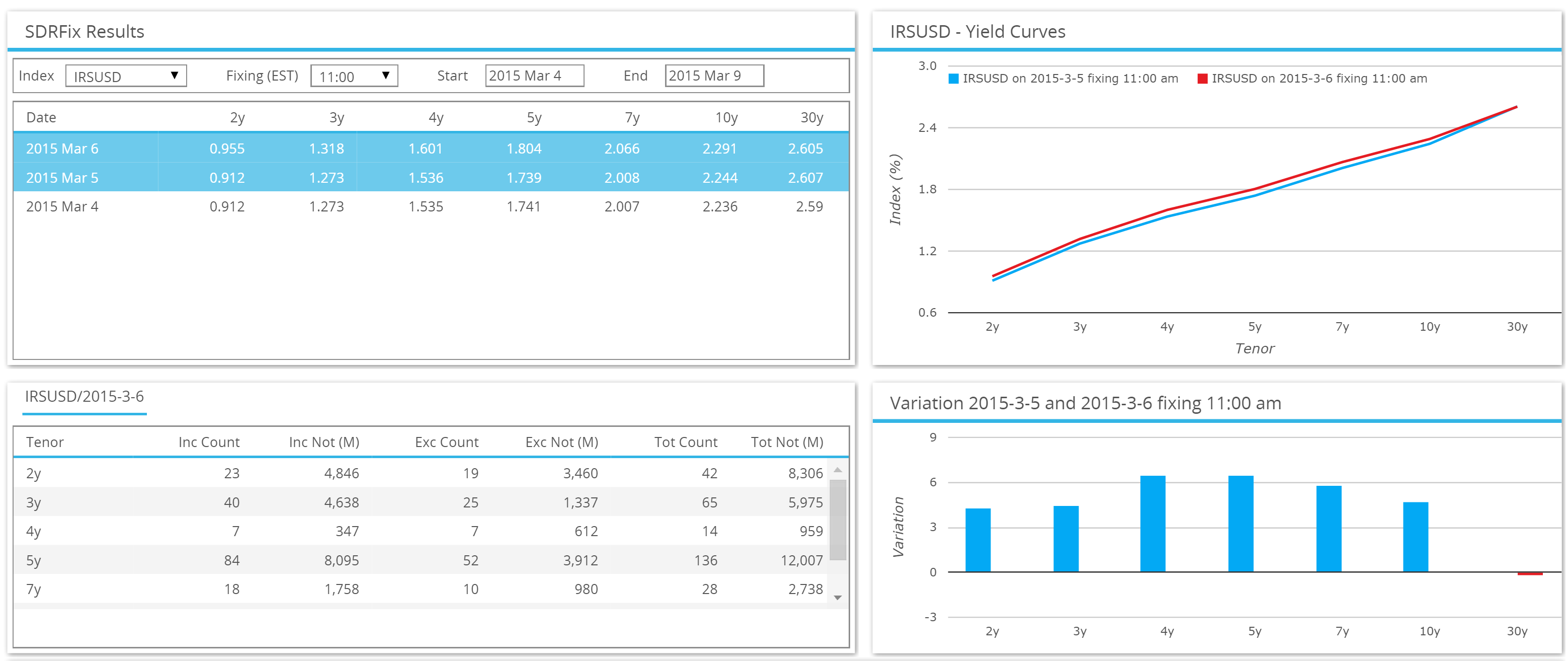

SDRFix

Clarus have a lesser-known product called SDRFix. Following the IOSCO Principals for Financial Benchmarks, we calculate daily fixings for a number of currencies and tenors, based on actual transactions from the SDRs. Screenshot below:

This enables us to easily link our volume data with a very useful market-data repository. The full methodology is outlined here. For the purposes of today’s blog, it is sufficient to recognise that we now have a reliable history of transaction-based prices that allows us to do meaningful analysis over a decent amount of history – yes, mandatory reporting really has been going on for that long!

Volatility begets Volumes

As I said at the top, this all comes from the thought that volatility drives volumes. Therefore, can I derive any exact relationship between volumes and price volatility?

As I said at the top, this all comes from the thought that volatility drives volumes. Therefore, can I derive any exact relationship between volumes and price volatility?

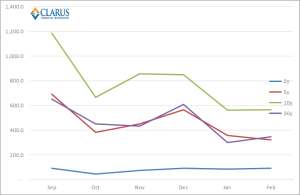

My initial stab in the dark looked very appealing. Using SEFView, I took the discrete monthly volumes of on-SEF USD IRS trading for the past six months, and plotted these as a ratio to the realised volatility during the month (chart to the right).

What this seemed to show is that the relationship between volatility and volume could be different for different tenors on the curve. I decided I might have something here, so I crunched the numbers properly. I looked at the market as a whole to try to come up with a framework to analyse these potential relationships.

Which measure of volatility?

The trouble when talking about volatility is people immediately think it is complicated. But let’s try to simplify, then add clarity. I really wanted a basic measure of volatility. After a little bit of research, I settled on the same measure as used by the Volatility Exchange. I then downloaded our SDRFix history and calculated realised daily returns for the different tenors. Depending on which window of time I am looking at, I annualise using the number of days/252 which gives me a nice amount of flexibility.

So, how has volatility evolved over time?

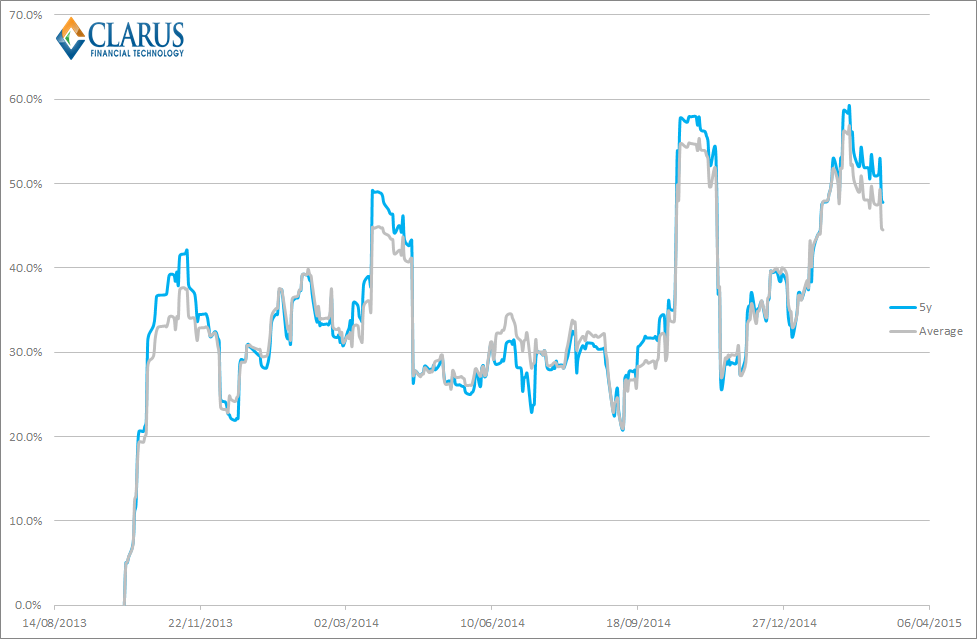

I briefly mentioned this when looking at February’s volumes – we are witnessing a volatile 2015. If we look at the realised monthly volatility for the 5 year tenor, we can see that it is very closely aligned to what is seen on average across all of the tenors we use for SDRFix (2y, 3y, 4y, 5y, 7y, 10y and 30y):

As evidence of how volatile 2015 has been, we see that recent levels have pretty much matched October 2014 and all of its’ shenanigans. That should normally be good for IDBs, SEFs and their core-group of market-making banks. So, how have volumes evolved over the same time period?

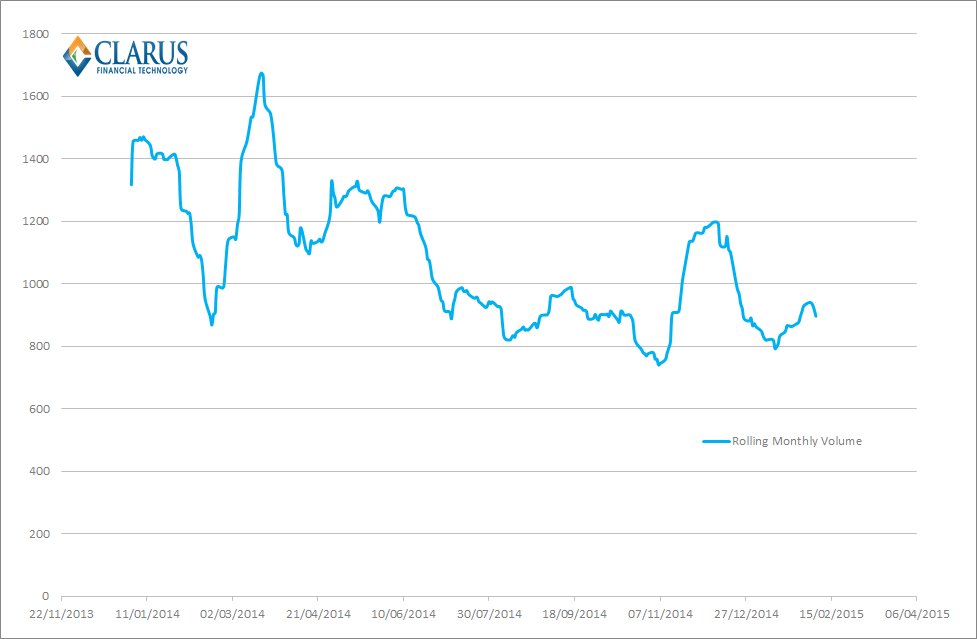

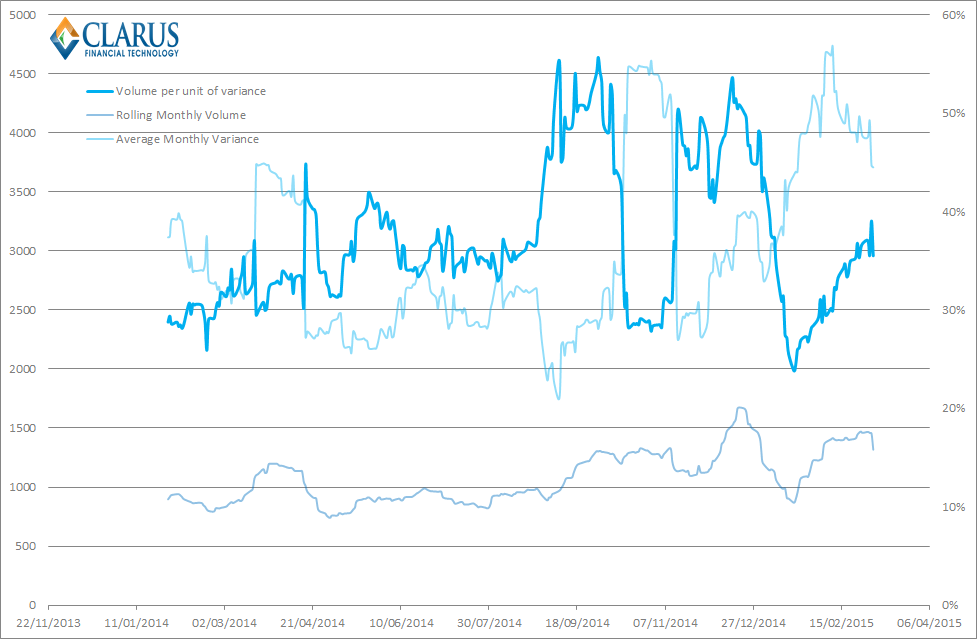

To keep things high-level, let’s look at all SDR USD IRS volumes (On & Off SEF, Cleared & Uncleared). Given that the time-series of 5y volatility is so similar to the average, we shouldn’t lose too much by taking an overall view. So that we can compare across multiple tenors, let’s use the DV01 measure – which is now populated all the way back to the beginning of 2014 in SDRView Researcher. What this allows me to do is generate a different way of looking at the numbers – namely a rolling monthly window (i.e the cumulative 20 -day volumes on a daily basis). This presents a rather interesting time-series:

Lo-and-behold – DV01s traded on-SEF have been plateauing, but we are actually seeing a (general) decrease in overall USD swap volumes at the SDRs.

A bit of an aside

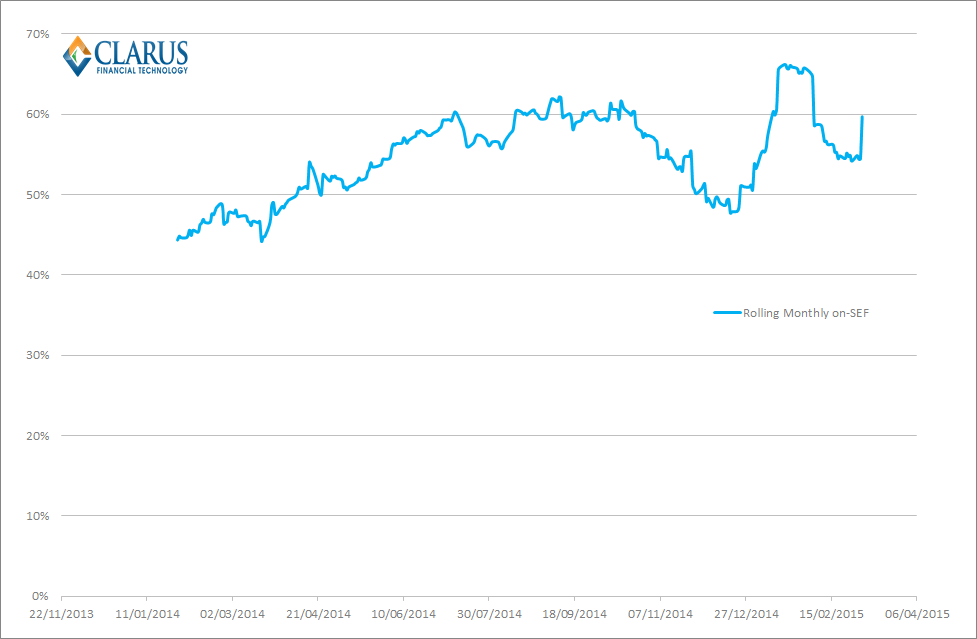

Just because I know people like these stats, we can look at these rolling volumes and compare with the rolling on-SEF volumes too. This allows us to produce another interesting time-series: the percentage of DV01 traded in the past 20-days that was on-SEF. It’s interesting to note that it’s pretty volatile, and had dropped back below 60% in 2015:

This might seem contradictory to the idea that SEF Volumes have been plateauing. But bear in mind that our monthly reports look at discrete time periods – these time-series are looking at every monthly time window since SEF trading was mandated.

There is a school of thought that states as volatility increases, people revert to picking up the phone and trading off-SEF. Indeed, the real story behind this analysis may well be just that – but I feel that deserves a closer look at another time. So for now, I’ll leave that chart there, and of course our Clarus users can explore the numbers themselves.

Back to the studio..

What I really wanted to look at this week were two things:

- Is there a (stable) relationship between volatility and volumes and/or

- What can we say about this relationship?

As the two charts above show – the relationship is anything but stable. If we simply divide our volume figures by our measure of volatility, we see an unstable ratio over time:

Sadly, like much of financial analysis, the signal from this ratio is possibly too noisy to act in a predictive manner. I’m tempted to think the key learning is that volumes are more sensitive to volatility thresholds. For example, with volatility over about 40% we begin to see a commensurate increase in volumes following that event. What does look to be true is that volatility drives volumes, as opposed to volumes driving volatility. Which is maybe not what regulators want to hear, after all their focus on trade reporting!

The show must go on…

I really don’t feel like that tells the whole story however. As we saw with our preliminary analysis, this relationship varies with tenor – when measured on a discrete time interval basis. We also have a lot of noise in our data – including compression runs, curve trading etc – that may be clouding the picture.

Unfortunately, for this blog that is all I have time for – but that is not to say the analysis is over. We continue to refine our data universe, and this is a classic example of why we do this.