After a struggle over many months BGC succeeded in getting majority shareholder agreement for its hostile takeover of GFI as announced in the press recently. CME had pulled out shortly before so I had expected this.

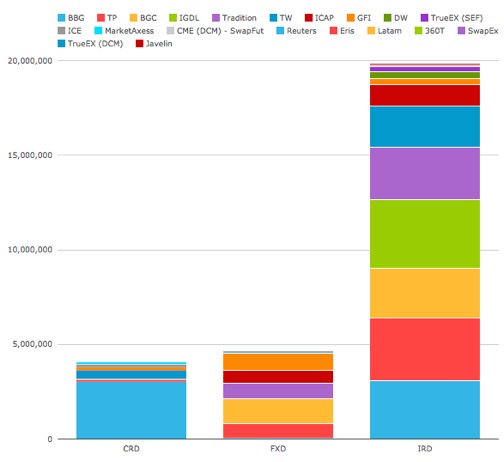

Using SEFView we can get a sense of the purpose of the acquisition. First, let’s look at total SEF volume. You can see the lighter orange below is BGC and the darker orange is GFI

SEF volume 6 months to end February 2015 ($m)

Source: SEFView Currency scope: All Product Scope: 1. FRAs excluded 2. Futures excluded.

You can see if you look at the orange shaded bars that there’s something in all three asset classes.

Basically, GFI had notional volume of about $360bn of Rates, $890bn of FX and $160bn of Credit in the period to add to BGCs $2,660bn, $1,280bn and $12bn respectively.

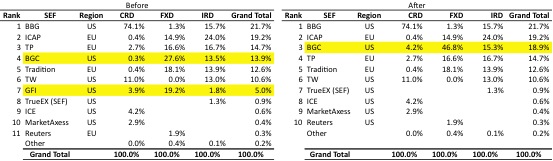

What we really want to know is what happens to their market position. To do this I exported the share % in total and of each asset class. I also combined the two SEFs in each case of ICAP and TradeWeb.

Now you can see that the combination moves BGC up in overall US SEF market share from 4th to 3rd (see chart).

Impact of BGC acquisition of GFI: SEF market shares 6 months to end February 2015

Source: SEFView Currency / Product scope: same as above Notes: 1. ICAP combines both IGDL and ICAP 2. TW combines TW and DW

When we look at asset classes – in the dominant volume asset class Rates, GFI provides BGC a small bump from 5th to 4th – with a share close to the 2nd and 3rd place players Bloomberg and TP though ICAP has a comfortable lead right now.

Perhaps progress in FXD and CRD drove the transaction, assuming these products may attract higher revenue per trade / notional than IRD. In Credit GFI moves BGC from nowhere to tied third with ICE – though Bloomberg dominates US CDS e-trading by miles. In FXD BGC moves from comfortable first to dominant first.

We can only guess what this does to revenues. What we can say though is that retention of GFI clients is critical to extraction of value from the transaction. This is in doubt if you believe this story in the press about significant exodus of GFI brokers if BGC wins the deal.

What I also wonder (in passing) is when we’ll see some exits soon among the 4 firms making up the 0.2% volume share in the “Other” category and the 5 other SEFs with no activity at all.

Takeaway

Consolidation has started at the top end of the US e-Trading market share rankings. Provided they can retain most of the GFI clients, BGC will be close to the leaders Bloomberg and ICAP, having been part of the chasing group before.

Will they retain GFI clients? Time (and SEFView) will tell.

This article is authored by Jon Skinner.