- Our Brexit blogs and June Swaps Review both show that OIS volumes have been very large recently

- We therefore have greater price transparency for short end interest rates

- This is particularly interesting when a central bank may be about to change monetary policy

- The BoE may be about to cut rates in response to the surprise Brexit result

- We analyse FRA and OIS prices to see what the market is currently expecting

Bank of England Meetings

All eyes this week are on the Bank Of England MPC meeting on Thursday 14th July at Midday (London time). This is their first scheduled meeting after the surprise Brexit result. Whilst there has not been any action on Rates or QE taken yet, the BoE have nonetheless already cut the “counter cyclical capital buffer” from 0.5% to 0%. In a speech on the 30th June, Carney also dropped heavy hints that monetary policy will be loosened over the summer months:

In my view, and I am not pre-judging the views of the other independent MPC members, the economic outlook has deteriorated and some monetary policy easing will likely be required over the summer.

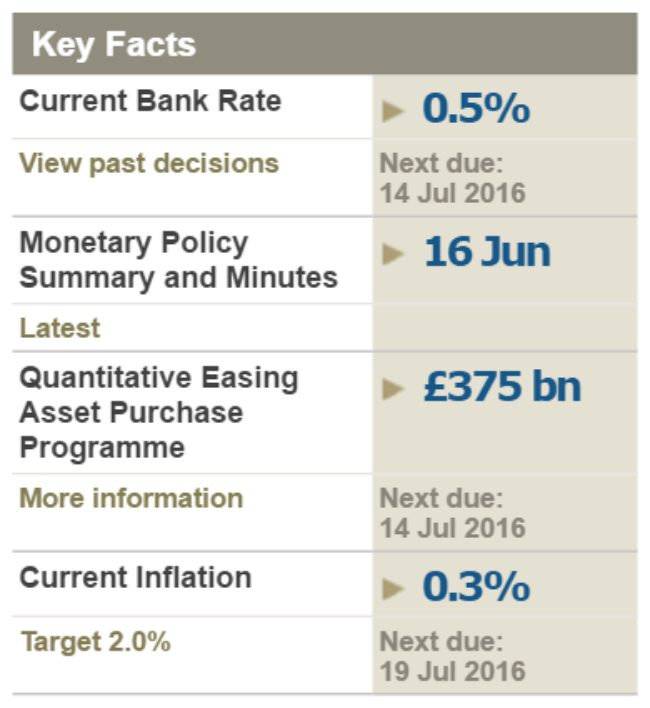

As the BoE website reminds us (see right), the current Bank Rate is at 0.5%. The next meeting date is on Thursday, July 14th.

As the BoE website reminds us (see right), the current Bank Rate is at 0.5%. The next meeting date is on Thursday, July 14th.

A bit of digging into the Maintenance Periods for the BoE shows that any Rate decision taken on Thursday will be in effect immediately and run until August 4th – just a three-week period. The Bank will then meet again on August 4th to decide Monetary Policy for the next Maintenance Period (MP). This MP runs from August 4th until 14th September 2016.

Market participants can take a view on BoE Bank Rate by trading Overnight Index Swaps that match these dates. That’s handy to know when sifting through the SDR trades looking for data concerning market expectations for the BoE at each meeting.

OIS Trade Data

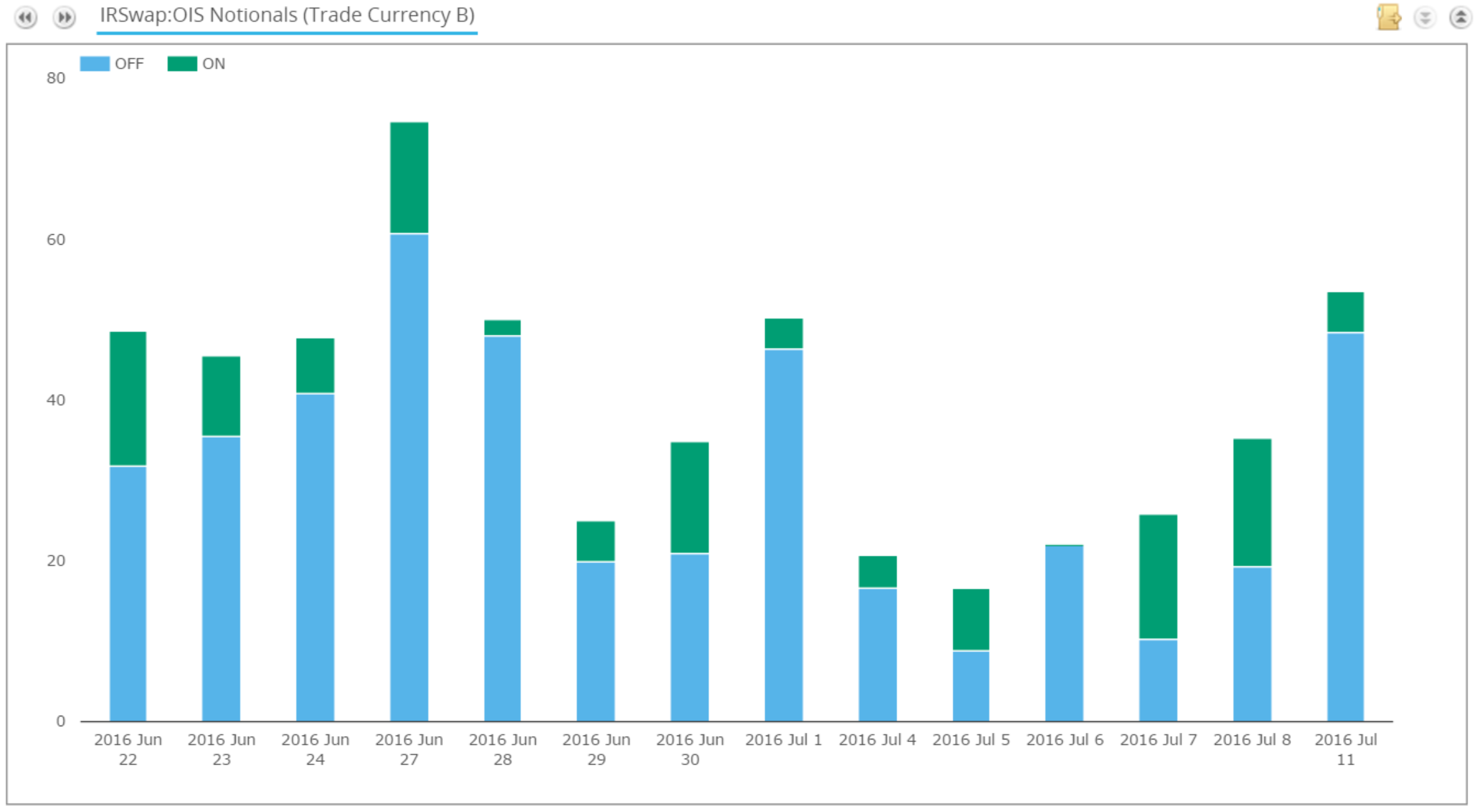

Throughout our Brexit blogs, we kept an eye on GBP OIS volumes. More commonly known as the “SONIA” market, it was very active after the vote – have a look at our June Swaps Review for a complete review of volumes. The chart to the right shows that volumes were consistently above £50bn per day, much of this traded off-SEF.

Throughout our Brexit blogs, we kept an eye on GBP OIS volumes. More commonly known as the “SONIA” market, it was very active after the vote – have a look at our June Swaps Review for a complete review of volumes. The chart to the right shows that volumes were consistently above £50bn per day, much of this traded off-SEF.

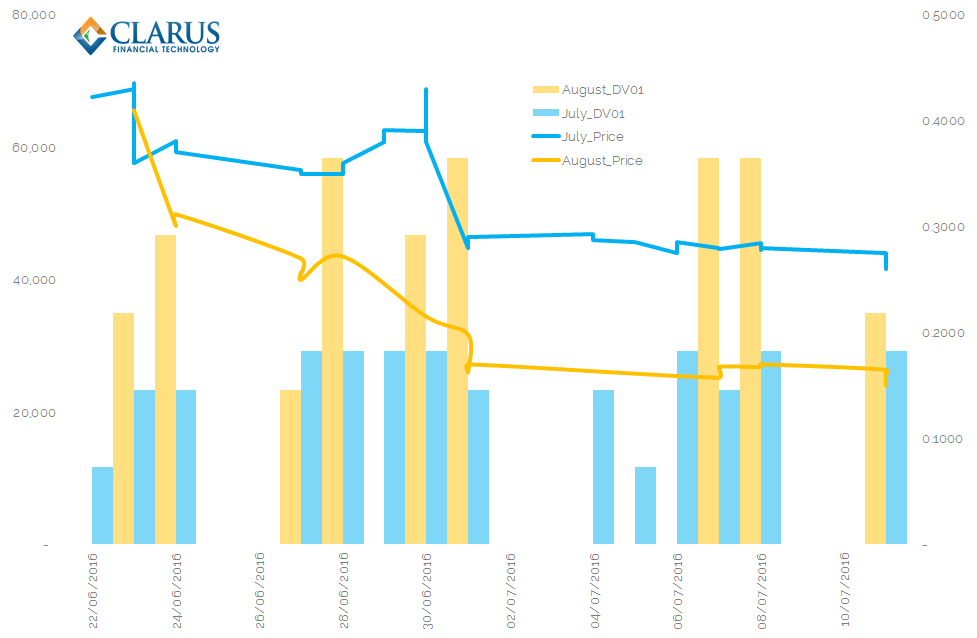

Using SDRView Researcher and Pro we can track the evolution of market expectations by looking at OIS trades with matching dates for any Maintenance Period. The chart below summarises the data for the July and August MPs:

Showing;

- Before the result of the vote was known, July MPC Sonia was trading at 0.435% and August was trading at 0.41%.

- On June 24th, July traded as low as 0.37% (6.5 b.p. lower) and August at 0.30% (11 b.p. lower)

- Both structures have seen their prices continue to move lower since.

- The last trade in July MPC was at 0.26%, a total of 17.5 basis points lower than before the vote. August MPC last traded at 0.15%, 26 basis points lower.

- The volumes of each trade are also shown on the chart. We can see that trading in July MPC has been more frequent but in smaller DV01 than August. This is because the July MP is unusually short (only 3 weeks), whilst the August is longer (over a month). Therefore for a given notional, an August trade represents a larger risk than a July trade.

Overall, we can see that the Sonia market is fully expecting a cut in rates by the August meeting. If we use 42 basis points as the “anchor” price (i.e. July and August were both trading around 42 before the vote and this has been a fairly consistent price for 1 month SONIA this year) then we have the following implied probabilities for rate cuts:

- (42-26)/25 = 64% in July

- (42-15)/25 = 108% in August (i.e. more than 25 basis points is priced in)

FRA Trade Data

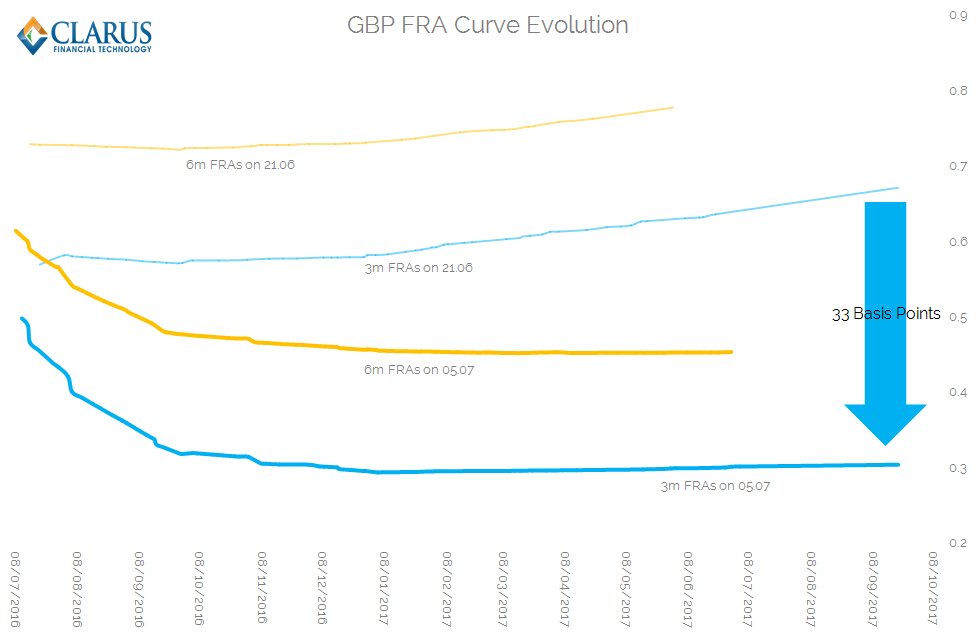

The SONIA market is not the only short-end instrument that we can monitor. As we looked at before the vote, we can also analyse the whole of the FRA curve. The chart below shows the 3m and 6m FRA curves at two points in time:

Showing;

- Between the 21st June and 5th July (i.e. over the Brexit referendum), the 3m GBP FRA curve dropped by 11.5 basis points for FRAs in July, 25 basis points for September FRAs and 33 basis points for FRAs maturing in the middle of 2017.

- Similarly, the 6m FRA curve also saw large drops – 14bp in July, 24 bp in September and up to 32 basis points next year.

- The move lower continued this week in the final FRA matching runs before the BoE meeting. This is not shown on the chart above.

- GBP 6m FRAs maturing next week are now at 0.55%, 3 basis points lower than on the 5th.

- GBP 3m FRAs maturing this month are as low as 0.4175%, about 1.5 basis points lower than last week.

Wrapping Up

- In USD markets, we have the CME’s Fed Watch Tool to monitor expectations of Fed action. This is a popular monitoring tool, receiving around 17,500 unique views each week.

- Using our SDR data, we can create very similar metrics.

- OIS trade data shows that there is a 64% chance of a rate cut tomorrow, with at least a 25 bp rate cut fully priced in by the August MPC meeting.

- FRA trading data also agree with those assessments.

- Changes in FRA/OIS spreads can cloud the picture painted in FRA markets, therefore we prefer the transparency offered by OIS markets.