Clarus Top Blogs of 2017

For my last blog article of 2017, I wanted to highlight our top blogs and view statistics for the year. Top 10 New Blogs in 2017 Starting with the most popular new blogs that we published this year.. Mechanics of Cross Currency Swaps MiFiD II: Instrument Reference Data Bitcoin meets OTC Derivatives Basel III Leverage Ratio FRTB […]

FSB Survey on Derivatives

The Financial Stability Board, in conjunction with the BCBS, CPMI and IOSCO have launched a broad survey about Cleared derivative markets. The survey looks at regulatory impacts to both cleared and uncleared derivative markets. The survey is split by market participant type – Dealer, FCM, CCP or Client. There are plenty of questions about the […]

Swaps Data Review: FX Options – candidate for a clearing mandate

My Monthly Swaps Data Review for Risk Magazine was published this week. This looks at: Vanilla FX Options reported to US SDRs Vanilla FX Option volumes on SEFs Barrier FX Options reported to US SDRs Please click here for free access to the full article on Risk.Net

G10 FX NDF Clearing

CCPView data reveals that NDFs in deliverable major currency pairs are being cleared. Contracts in EURUSD, GBPUSD, AUDUSD, CHFUSD and USDJPY have been reported. LCH ForexClear have made these available to clear, alongside their more traditional EM currency NDFs. The LCH press release suggests these are being used to optimise bilateral ISDA SIMM margins. Clearing […]

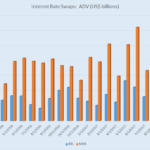

Nov 2017 Swaps Review in 16 Charts

Continuing with our Swaps review series, let’s look at volumes in November 2017. Summary: SDR USD IRS volumes similar to prior months USD IRS On SEF Compression close to monthly highs USD OIS volume similar to the gross notional of IRS Our new Daily Briefing for USD Swaps is now available EUR, GBP, JPY IRS volumes similar GBP On SEF Compression up from prior […]

LIBOR Reform – Latest Developments

Clarus will be talking about Libor reforms at the FoW Derivatives World event in London tomorrow, December 6th 2017. For more information on the event and to register, please check out the link below. It should be free to attend for most of our readers. FoW Derivatives World London Libor Reform Before we end 2017, […]

OCC Quarterly Report on Bank Derivatives Activities

Our regular readers will know that the Clarus Blog focuses on Derivatives and the new regulations introduced after the Financial Crisis of 2007-08. The massive increase in availability of data on OTC Derivatives markets is of great interest to us. However at times we are guilty of not paying enough attention to older data sources. […]

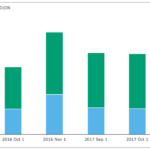

Latam Swaps: Trends in IRS and NDF Data

I last looked at Latam swaps back in February this year, with the focus on Interest Rate swaps. We learned that both BRL and MXN swaps had migrated to a primarily cleared market at CME. We also then looked at CME margin requirements for these swaps and noted they were more expensive than similar USD swaps. […]

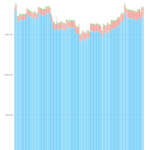

What is going on in Uncleared Derivative Markets?

We look at data from the BIS on Uncleared IRS. Notional Outstanding of Uncleared derivatives has been constant for the past year. The Gross Market Value of these derivatives has decreased by around 40%. The reduction in market value seems to be related to rates moving higher. Both Cleared and Uncleared markets have seen large […]

We found the CHF SARON Swaps!

The first CHF SARON swaps have appeared in SDR data. This reflects broader uptake of SARON across more trading counterparties. We are keeping a close eye on SARON volumes as it is somewhat of a test case for broader Libor reforms. Cleared data shows increased Open Interest at LCH, but daily volumes continue to be […]