- CCPView data reveals that NDFs in deliverable major currency pairs are being cleared.

- Contracts in EURUSD, GBPUSD, AUDUSD, CHFUSD and USDJPY have been reported.

- LCH ForexClear have made these available to clear, alongside their more traditional EM currency NDFs.

- The LCH press release suggests these are being used to optimise bilateral ISDA SIMM margins.

Clearing FX

As we wrote about recently, there is a lot happening in the FX Clearing space right now. Uncleared Margin Rules have made clearing of NDFs (which are now subject to bilateral IM and VM) attractive. This is because multilateral netting of counterparty and market risks should reduce margin consumption when compared to bilateral trading.

What we didn’t expect to see was a new market develop. However, last week we saw some strange volumes reported for FX at LCH ForexClear – NDFs trading on deliverable currency pairs.

Volume Data from CCPView

CCPView shows that volumes were reported across five currency pairs, with most of the volume in GBPUSD:

Showing;

- A couple of test trades were reported on both 8th Nov and 14th Nov – in very small size (less than $10,000 in notional).

- On the 29th November, these volumes suddenly jumped.

- There was $49m of AUDUSD, $54m EURUSD, $5m USDCHF, $65m USDJPY and $200m GBPUSD.

- This is particularly surprising as all of these currencies are deliverable. Why would you want to trade an NDF on a deliverable currency pair? (See below).

- All of these trades added to Open Interest. We do not know the maturity of these trades (LCH do not provide tenor information for volumes), so it will be interesting to see if we can see these trades maturing before new volumes come into the service to infer their maturity.

- There was also $12m traded on the 6th December (not shown above) – across all five currency pairs. This also added to Open Interest.

“G10” Clearing At LCH ForexClear

We had to wait a couple of days to see an explanation for these volumes. Eventually LCH published a press release here:

![]()

From the full text, we infer that;

- Five new currency pairs are live – AUDUSD, EURUSD, USDCHF, USDJPY and GBPUSD.

- The volumes were generated by a “multilateral risk reduction run”.

- It looks like market participant’s goal is to reduce ISDA SIMM bilateral margin arising from bilateral FX Option positions.

ISDA SIMM FX

Clarus have written a whole host of ISDA SIMM related blogs. We have previously highlighted the FX risks associated with Cross Currency Swaps under ISDA SIMM here (which are minimal). But we have not blogged about our solutions for NDFs or FX Options.

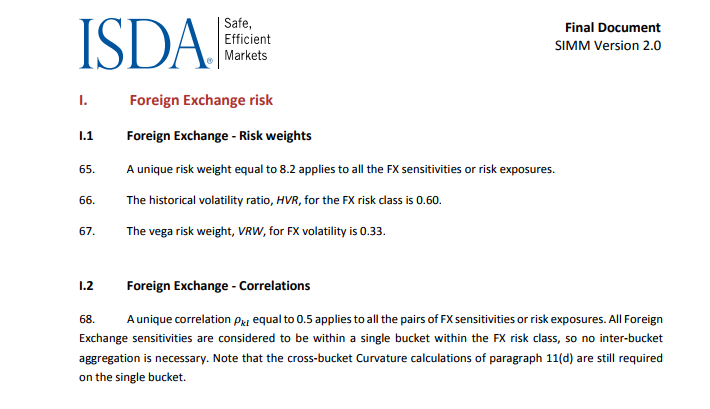

From an implementation perspective, ISDA SIMM for FX deltas is pretty straightforward. SIMM 2.0 shows all the inputs that we need:

Armed with our trusty covariance equation, we can simply consolidate across currency pairs.

Armed with our trusty covariance equation, we can simply consolidate across currency pairs.

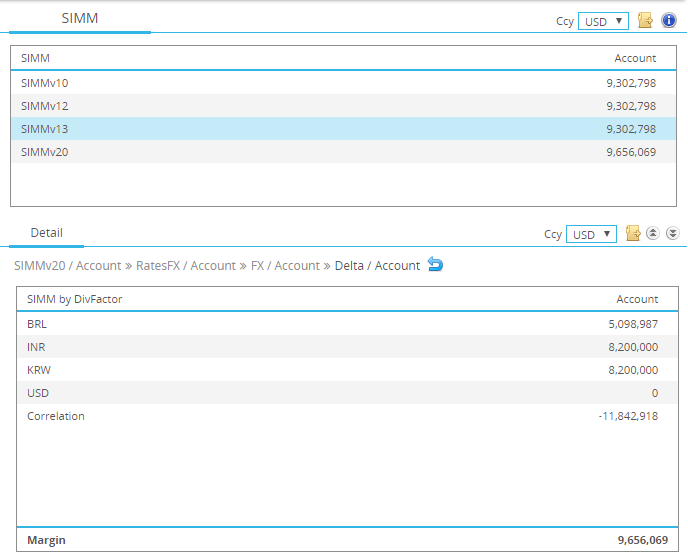

Our Initial Margin calculation, optimisation and management software is called CHARM. It employs sophisticated risk analysis and calculation engines to provide high performance margin calculations. FX products in SIMM are of course supported, and our calculations are very efficient:

Showing;

Showing;

- ISDA SIMM margin for an FX portfolio.

- Calculations are performed versus all versions of SIMM, including the recently launched ISDA SIMM 2.0.

- We can see the sources of IM per currency, plus the diversification benefit.

When we wrote our ISDA SIMM module for FX, we focussed on NDFs – consistent with our recent blogs about FX Clearing.

Physical FX trades (e.g. FX spot, FX Forwards, FX Outrights, even Cross Currency Swaps) do not generate an FX delta under the Uncleared Margin Rules – they are exempt.

However, you can still end up with an FX Delta input to ISDA SIMM for a deliverable currency pair. Typically, this will be driven by FX Options portfolios.

How do you optimise this FX Delta if the physical FX products are exempt from IM?

The industry answer is to trade an NDF on a deliverable currency pair!

Execution

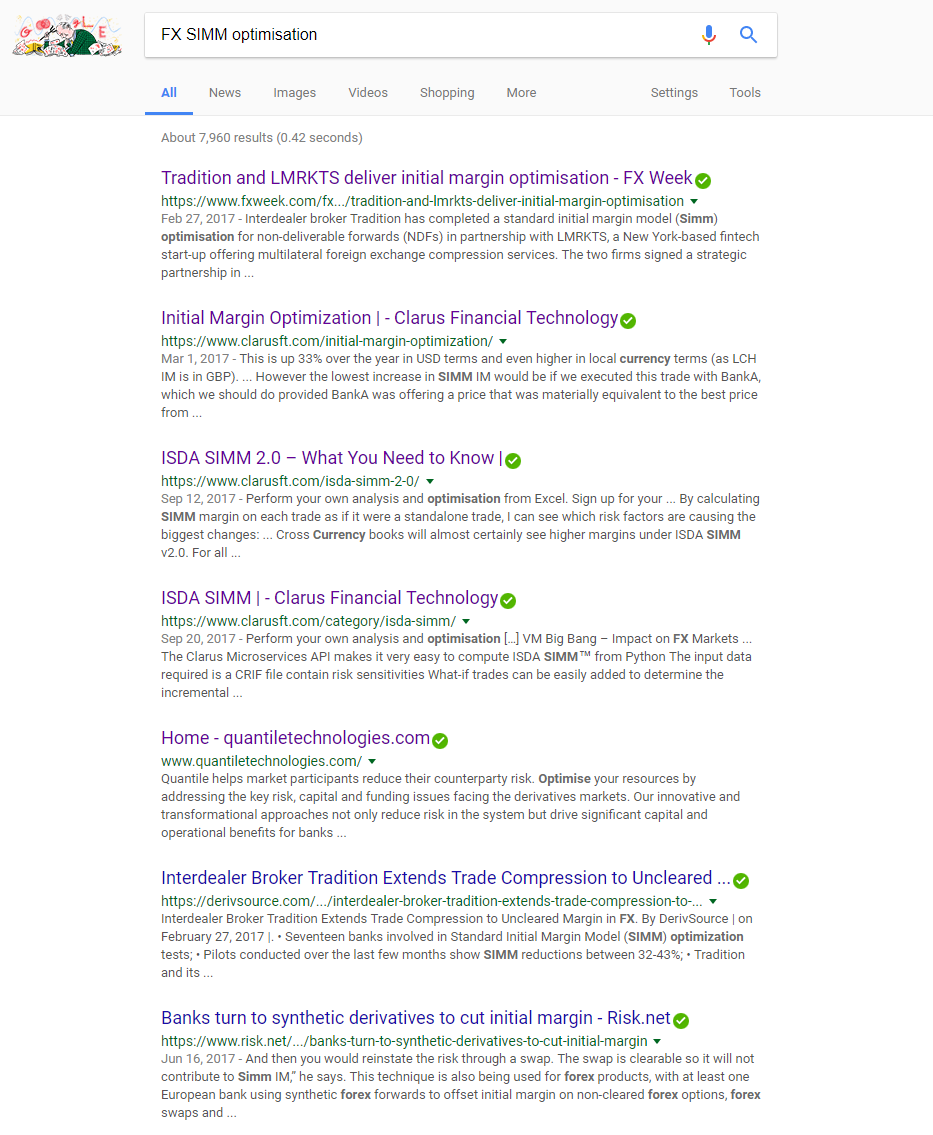

We’ve not seen any press on who may have helped execute these NDFs. A simple Google on “FX SIMM Optimisation” is pretty instructive though. Someone called “Clarus” is pretty interested in this (!), but we also see LMRKTS and Quantile as possible execution providers.

We’ve not seen any press on who may have helped execute these NDFs. A simple Google on “FX SIMM Optimisation” is pretty instructive though. Someone called “Clarus” is pretty interested in this (!), but we also see LMRKTS and Quantile as possible execution providers.

Evolving Markets

These new cleared volumes are another industry evolution in response to the Uncleared Margin Rules. We make that three “innovations” that this regulation has led to:

- Increased clearing of eligible products – Inflation swaps, OIS and “vanilla” NDFs.

- Bilateral Optimisation

- New product initiatives – NDFs on deliverable currencies.

Stay tuned to the Clarus blog to stay on top of any more changes to the market.

In Summary

- LCH ForexClear now offers clearing in five NDFs on deliverable currencies.

- These are GBPUSD, AUDUSD, EURUSD, USDCHF and USDJPY.

- Close to $400m in these NDFs traded on the 29th November.

- The LCH press release suggests that this volume was generated from a multilateral risk reduction exercise.

- Clarus provides tools to calculate, manage and optimise your ISDA SIMM risks, including support for FX products.