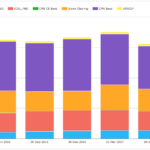

CCP Disclosures 2Q 2017 – What the Data Shows

Central Counterparties recently published their latest CPMI-IOSCO Quantitative Disclosures and in this article I will highlight what the data shows, similar to my article on 1Q 2017 trends. Background Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more […]

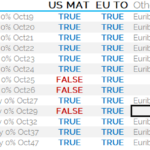

MIFID II – ESMA Finalises the Trading Obligation

ESMA have published the final report for the Trading Obligation. Interest Rate Swaps in EUR, GBP and USD will have to be traded on venue from 2018. There has been convergence with the swaps that are currently MAT in the US, potentially simplifying the global regulatory regime. 8y and 9y EUR swaps versus EURIBOR 6m […]

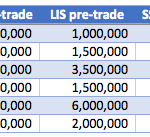

MiFID II Bond Transparency Calculations

As Jan 3, 2018 is now just three months away, I wanted to update my February 2016 article MiFID II and Transparency for Bonds, in particular as ESMA have now published Transparency Calculations and compare these to transparency in the US Corporate Bond market with FINRA TRACE. Background Post-trade transparency and pre-trade transparency for Bonds is meant […]

Has Swaptions Clearing Begun?

We’ve written quite a bit about swaptions clearing in our blog. I was surprised to see that the first article was over 4 years old – back when the industry (and Gensler!) began talking about it: July 2013 – Swaptions Clearing – Why Is It Important November 2013 – Swaptions Clearing – A More Detailed […]

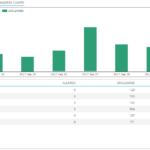

AUD Swap Markets in August 2017

Time to re-acquaint ourselves with the world’s 4th/5th largest cleared swap market – the mighty Aussie dollar. August is traditionally a quiet month, so does quality come to the fore when execution is more difficult in thin markets? About 30% of new risk is transacted on a SEF. We take a look at the volumes. […]