- ESMA have published the final report for the Trading Obligation.

- Interest Rate Swaps in EUR, GBP and USD will have to be traded on venue from 2018.

- There has been convergence with the swaps that are currently MAT in the US, potentially simplifying the global regulatory regime.

- 8y and 9y EUR swaps versus EURIBOR 6m are the most noticeable difference between the two jurisdictions.

The Trading Obligations

For background to this post, please refer to my original post and our response to the consultation. Otherwise, I will assume that our readers know what I am talking about when I refer to the Trading Obligation under MIFID II!

Last week, we were very pleased to see a significant convergence between the US and European regimes when we skipped to the final Annex of the latest RTS from ESMA.

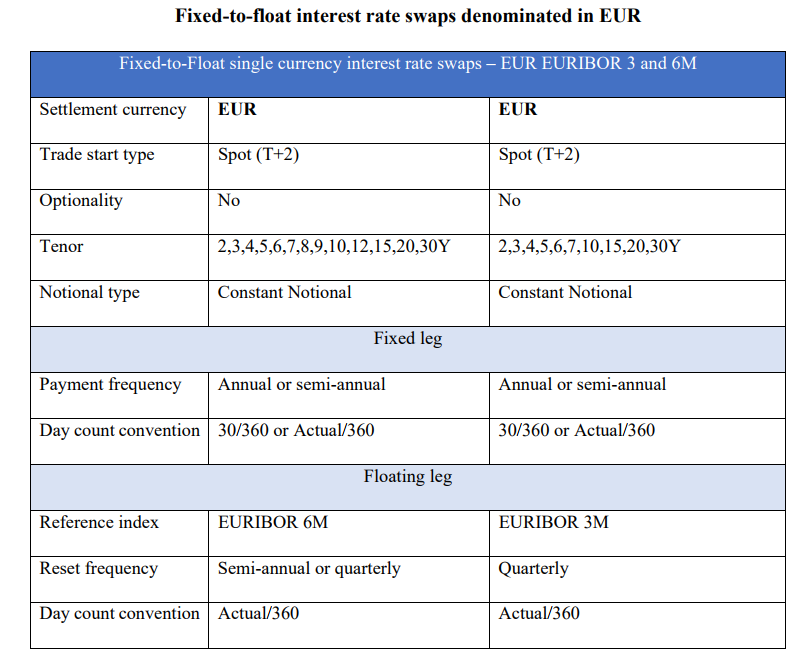

This is the European Trading Obligation (the Annex of Annex IV in the RTS) for EUR denominated swaps:

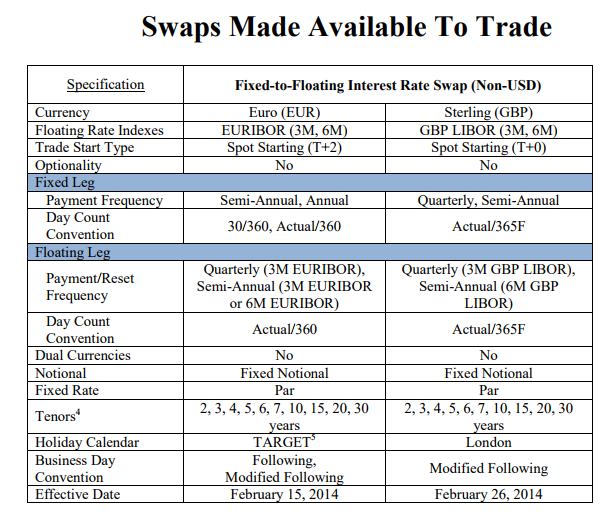

And this is the MAT ruling from the CFTC from way back in February 2014 (has it really been that long?):

They aren’t that easy to compare, are they? Still, it is useful for two purposes;

- Everyone will want to see the originals at some point. Consider this your resource for hard-to-find regulatory documents that you like to paste into presentations/blogs/research.

- It highlights that you need the Clarus Compliance microservice to keep on top of this. I wouldn’t want to keep that information in my head. This is the output of our Compliance checker:

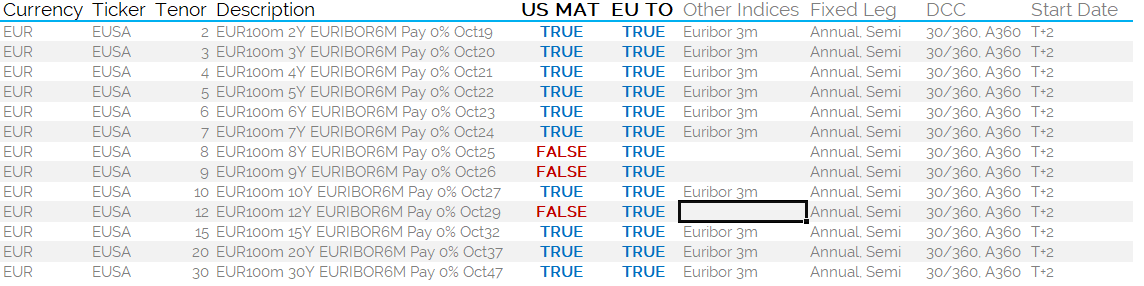

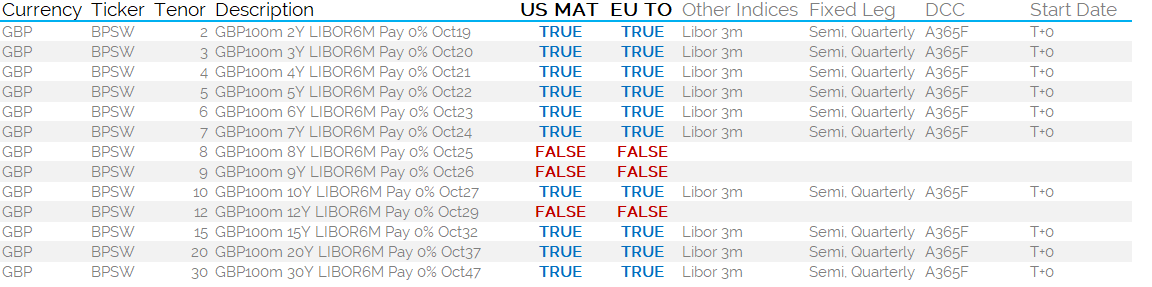

EUR Swaps Compliance

Given the difficulties of comparing the two regimes, I thought I should build a little widget for myself in Excel. I built this via our Clarus Excel add-in, giving me access to all of our cloud-hosted Microservices within my favoured Excel environment. I could equally have built this in Python or R, but I wanted some pretty tables which are easier to format in Excel.

Showing;

- EUR IRS trades that are subject to the Trading Obligation under MIFIDII have a big blue TRUE next to them under the EU TO column.

- EUR IRS trades that are MAT in the US and hence subject to the Execution Mandate (meaning that they must be transacted on-SEF by a US Person if below block size) have a big blue TRUE next to them under the US MAT column.

- There is considerable overlap between the two jurisdictions. This is a good thing as it simplifies all of our lives.

- Only spot starting swaps are covered.

- There are 3 EUR IRS trades that are not MAT in the US but are subject to the European TO.

- These are spot starting Fixed-Float EUR swaps versus Euribor 6m with tenors of 8 years, 9 years or 12 years.

- Note that EUR swaps versus both Euribor 6m and Euribor 3m are subject to the execution mandates in both jurisdictions (apart from the 3 additional tenors under the EU TO).

- I wonder if this new EU TO will motivate SEFs in the US to post new MAT filings to align the two jurisdictions? That strikes me as a good idea…

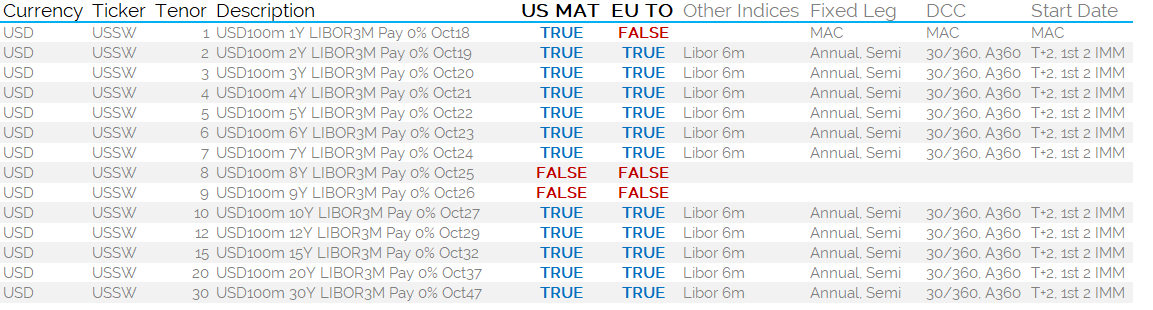

USD Swaps Compliance

What about USD swaps? See table below:

Showing;

- An almost universal alignment of execution mandates in Europe and the USA.

- Neither 8y nor 9y USD swaps are subject to an execution mandate in either jurisdiction.

- 12y USD swaps are subject to the execution mandates of both jurisdictions.

- The one area of divergence is for MAC swaps. MAC swaps are not subject to any execution requirements in Europe (to the extent that their coupons are not “at-market” for an IMM dated USD swap…) but they are in the US.

- In addition, 1y MAC swaps are MAT in the US but do not get any mention under the European TO.

- Note that USD swaps versus both Libor 6m and Libor 3m are subject to the execution mandates in both jurisdictions (apart from MAC swaps in the US which cover only Libor 3m).

- Both jurisdictions have decided to cover USD swaps that start out of the first two IMM dates, as well as spot starting swaps.

GBP Swaps Compliance

Both jurisdictions cover only 3 currencies. The final currency is GBP swaps, likely cementing its’ position as the third most traded currency amongst Interest Rate Derivatives.

Showing;

- The trading requirements in GBP swaps are identical* across both jurisdictions.

- It’s nice to finish on a simple example.

*A note on ‘identical’

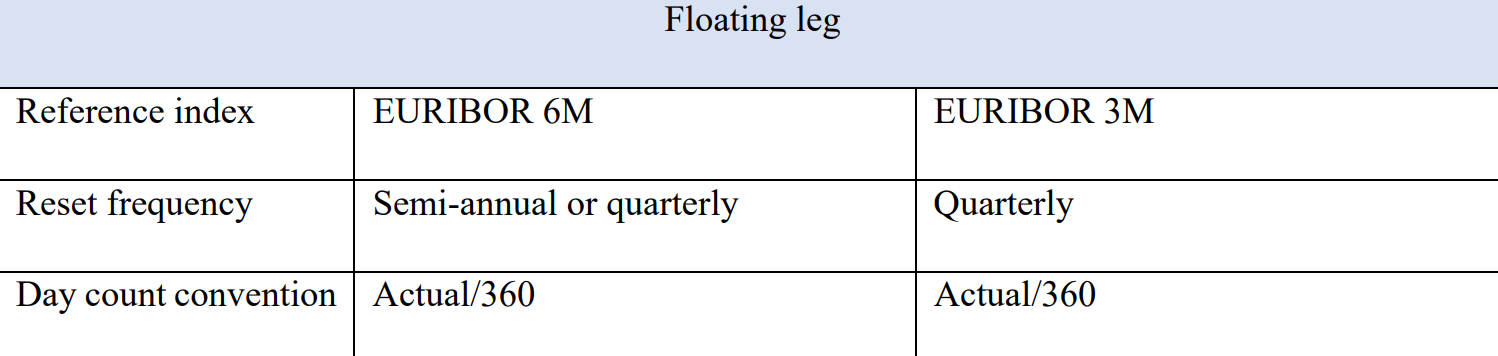

The ESMA document includes the following language for all 6 month indices:

Showing;

- A trade that is reset on a 6m index, but that resets quarterly, is subject to the TO.

- To be clear, these swaps are not MAT in the US.

- These swaps would not be considered linear products on a swaps desk because they have convexity associated with them. This occurs whenever the resetting floating index is of a longer tenor than the reset frequency. The reset rate hence incorporates an element of market expectations for the future path of rates past the point of a subsequent reset.

It seems that ESMA would have liked a quantitative proof as to why contracts that reset quarterly on a 6 month index are convex. Maybe we should have just called it a CMS swap? The ESMA response does acknowledge the market’s concern regarding this point: Unfortunately, these concerns were not upheld because;

Unfortunately, these concerns were not upheld because;

Therefore if we can learn two things it is;

Therefore if we can learn two things it is;

- When responding to a consultation, always answer the question.

- When responding to a consultation, always provide as much data as possible. Clarus have the data products, and our response (which is mentioned several times in the final TO) included 11 charts along with the data to back them up.

We would therefore like to take this opportunity to encourage all market participants to include data wherever possible to get your point across. Clarus data subscriptions are simple to get….just contact us.

In Summary

- We are very happy to see a convergence of the European and American trading obligations.

- This simplifies market structure as well as setting a “gold standard” internationally for other jurisdictions to aim for.

- Spot starting USD, EUR and GBP swaps across most maturities will trade on-platform during 2018.

- There are just 4 swaps that do not have a dual trading obligation (EUR 8y, 9y, 12y plus USD 1y MAC swaps).

- Clarus Microservices provide the most simple way to compare, contrast and keep on top of these new trading rules.

- Clarus data products provide the ideal platform on which to base responses to regulatory consultations, and we implore the industry to follow ESMA’s data-driven approach. Subscribe now!