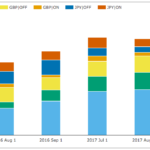

Sep 2017 Swaps Review in 16 Charts

Continuing with our Swaps review series, let’s look at volumes in September 2017. Summary: SDR USD IRS volumes similar to prior months USD IRS SEF Compression and Rolls with much higher volumes USD OIS volume subdued and down to similar gross notional to IRS Our new Daily Briefing for USD Swaps is now available EUR IRS and OIS volume up from […]

Bitcoin Meets OTC Derivatives

I attended the FIA event last week in Chicago. Much of the same stuff. Bank capital, swaps regulation, clearing, MIFID. And the obligatory panel on bitcoin. Over the past couple years, Bitcoin panels in our industry have tended to start out with the moderator making clear “we’re not going to talk about bitcoin the currency, […]

Public Hearing RE: Examining the 2017 Agenda for the Commodity Futures Trading Commission

Congressman Collin Peterson cited our recent blog, “MIFID II transparency will leave us in the dark”, during a committee hearing in Washington. The session in the public hearing was recorded and is available below. The Clarus citation is around 24m02.

SA-CCR Calculator

SA-CCR for Excel calculates the Standardised Approach for Credit Risk Use it to reconcile your calculations Or assess the impact of moving to SA-CCR And perform pre-trade what-if analysis Free 14-day trials are available for all financial firms. Background In March 2014, the Basel Committee on Banking Supervision published bcbs279, the Standardised Approach for measuring Counterparty […]

Swaps Data Review: Basis Swaps Galore

My Monthly Swaps Data Review for Risk Magazine was published last week. This looks at some of the less well traded IRD products: In USD, EUR, GBP, JPY, AUD, CAD Basis Swaps USD FedFunds and Libor 1m v3m Cross Currency Inflation Swaps Caps and Floors Exotics Please click here for free access to the full […]

Trade Validation: A simple version of FpML rule IRD12

Trade representations in CSV or FpML often have issues with stubs. FpML validation rule IRD12 has simple alternative for a wide range of cases. A form of FpML IRD12 can be represented in XPath for a wide range of cases. During proof-of-concept trials we are often asked to load up a prospects portfolio; either a […]

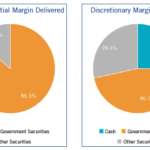

非クリアリング・デリバティブ取引のマージン

非クリアリングについての当初証拠金(IM)に係るルール(UMR)がスタートして1年経過した。

ISDAマージン・サーベイ2017は、IMについて差入れ・差出し額のスナップショットを公表している。

上記は2017年3月31日時点で、いわゆるフェーズ1対象金融機関の間でのやりとりで、それぞれ、472億米ドル(ドル)、466億ドルとなっている。

Summary Of Treasury’s Capital Markets Report to Trump

Shortly after Trump became president, true to his campaign promises to “roll back regulation”, he issued an executive order for a review of the American Financial system, with some core principles around making regulation smarter and fostering growth, among others. The US Treasury is responding to this order by providing 4 reports covering Banking, Capital […]

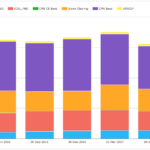

CCP Disclosures 2Q 2017 – What the Data Shows

Central Counterparties recently published their latest CPMI-IOSCO Quantitative Disclosures and in this article I will highlight what the data shows, similar to my article on 1Q 2017 trends. Background Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more […]

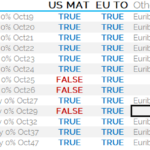

MIFID II – ESMA Finalises the Trading Obligation

ESMA have published the final report for the Trading Obligation. Interest Rate Swaps in EUR, GBP and USD will have to be traded on venue from 2018. There has been convergence with the swaps that are currently MAT in the US, potentially simplifying the global regulatory regime. 8y and 9y EUR swaps versus EURIBOR 6m […]