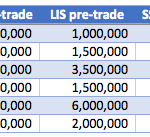

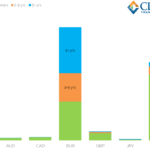

MiFID II Bond Transparency Calculations

As Jan 3, 2018 is now just three months away, I wanted to update my February 2016 article MiFID II and Transparency for Bonds, in particular as ESMA have now published Transparency Calculations and compare these to transparency in the US Corporate Bond market with FINRA TRACE. Background Post-trade transparency and pre-trade transparency for Bonds is meant […]

Has Swaptions Clearing Begun?

We’ve written quite a bit about swaptions clearing in our blog. I was surprised to see that the first article was over 4 years old – back when the industry (and Gensler!) began talking about it: July 2013 – Swaptions Clearing – Why Is It Important November 2013 – Swaptions Clearing – A More Detailed […]

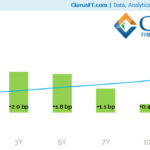

AUD Swap Markets in August 2017

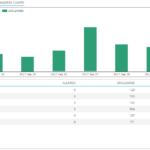

Time to re-acquaint ourselves with the world’s 4th/5th largest cleared swap market – the mighty Aussie dollar. August is traditionally a quiet month, so does quality come to the fore when execution is more difficult in thin markets? About 30% of new risk is transacted on a SEF. We take a look at the volumes. […]

Initial Margin Attribution

Initial margin is an important portolio measure Attributing it to constituent business units is not simple Diversification benefit between units is a key concept The choice of methodologies can align or mis-align incentives An example explains what you should know Initial Margin and Diversification Benefit IM is a portfolio risk measure and one that is […]

Libor Reform – What You Need to Know

Libors and Risk Free Rates are going through a period of change. Regulators and industry working groups are identifying their preferred Risk Free Rates in preparation for a post-Libor world. Over the next 4 years, derivatives market liquidity will transition into products referencing Risk Free Rates instead of Libors. This will impact new trades and […]

Introducing Our Daily Briefing, Direct to your inbox

Introducing the new Clarus Daily Briefing. Curated market information direct to your inbox. Swap rates, volumes and Central Bank rate expectations every day. Make sense of daily trading activity in less than 2 minutes. We offer a free two-week trial before your paid subscription starts. Daily Market Commentary We always aim to improve the general […]

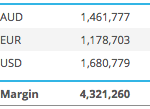

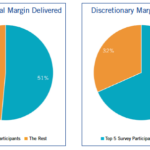

Margin for Non-Cleared Derivatives

Uncleared Margin Rules (UMR) for IM have now been in force for one year The ISDA Margin Survey 2017 provides a snapshot of IM delivered and received $47.2 billion and $46.6 billion respectively, between Phase One firms (March 31, 2017) I look at how the figures compare to an $800 billion estimate from 2012 What […]

CME Halts CDS – Where’s The CDS Business?

Last week, CME announced it would end it’s clearing offering for Credit Default Swaps, and instead focus it’s effort on other innovations in clearing services for Interest Rate and FX, including: FX Options launched by 2017 year end Interest Rate swaps for 3 more currencies – CNY, CLP, and COP by early 2018 Further capital […]

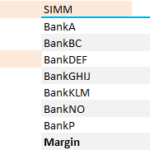

ISDA SIMM 2.0 – What You Need to Know

ISDA SIMM version 2.0 is coming in December 2017. Re-calibration and new risk factors will mean Initial Margin changes for all portfolios. SIMM for Excel gives you the tools to understand and model these changes. Quickly compare before/after SIMM levels in Excel. Drill-down into Counterparty and Risk Factor levels. Perform your own analysis and optimisation […]

MiFID II: Why Research is in the News

There have been many recent articles on Banks having to charge for Research as required under MiFiD II, see here, here and here, so I thought I would look into the detail. Inducements The relevant text in the EU Commission Delegated Directive is in Chapter IV: Inducements, the title providing a clue to the intent. This Chapter […]