- The Swedish Banker’s Association is looking to introduce an Alternative Reference Rate for SEK markets.

- At the moment, STIBOR is the underlying index for SEK swaps.

- There are on-going consultations to introduce a Risk Free Rate in Swedish markets.

- We take a look at the details.

SEK Markets Today

As it stands today, there are two Interest Rate Swaps commonly traded in Sweden;

- Fixed SEK Annual 30/360 vs Floating SEK STIBOR 3m. This is the vanilla IRS and…

…and well, truth be told, that is it really.

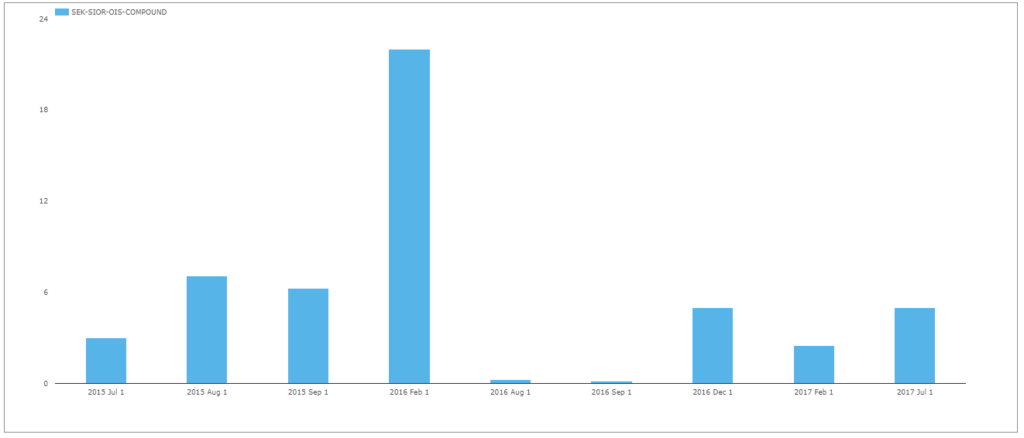

I thought that OIS vs STINA was a relatively active market in Sweden. But when I look at our data, I find the following in SDRView:

Showing that there are many months that can pass by (last trade reported in July 2017….!) without a single STINA OIS being reported to a US SDR.

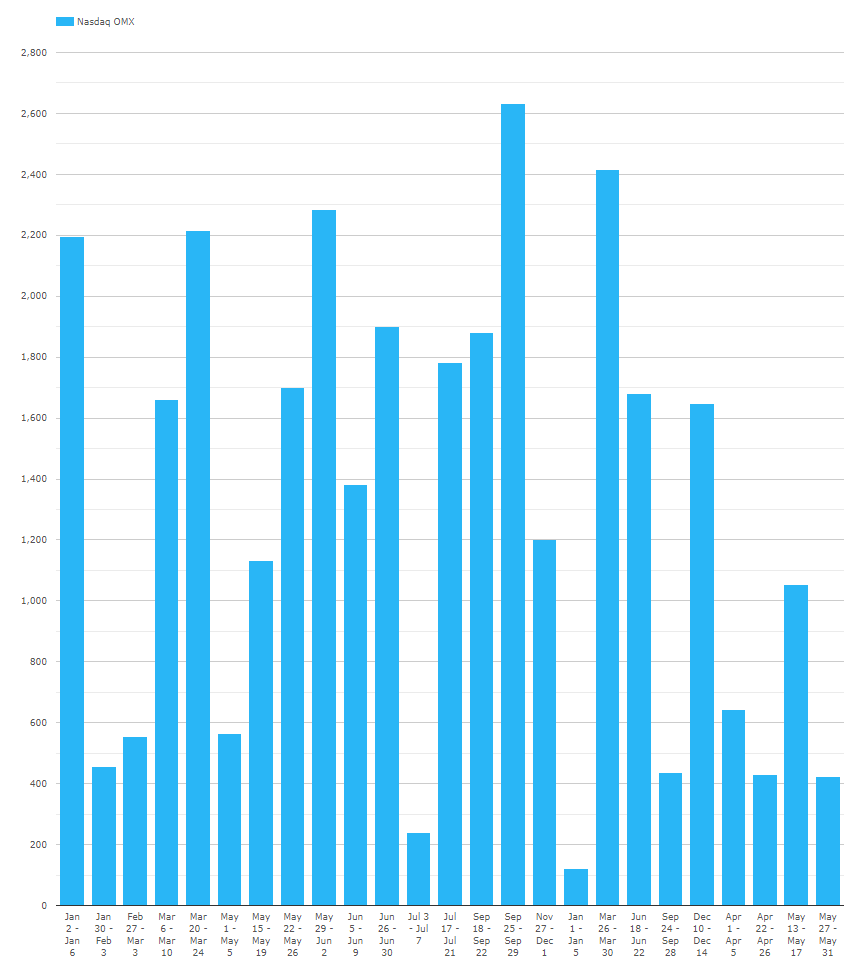

And from CCPView, which covers the global market, we see further evidence of a substantial lack of activity;

Showing that there has at least been some cleared activity in SEK STINA OIS at Nasdaq in 2019. However, open interest in STINA has decreased from a peak of $17bn equivalent to $2.5bn currently at Nasdaq.

Through this research, I found that LCH doesn’t even clear STINA swaps:

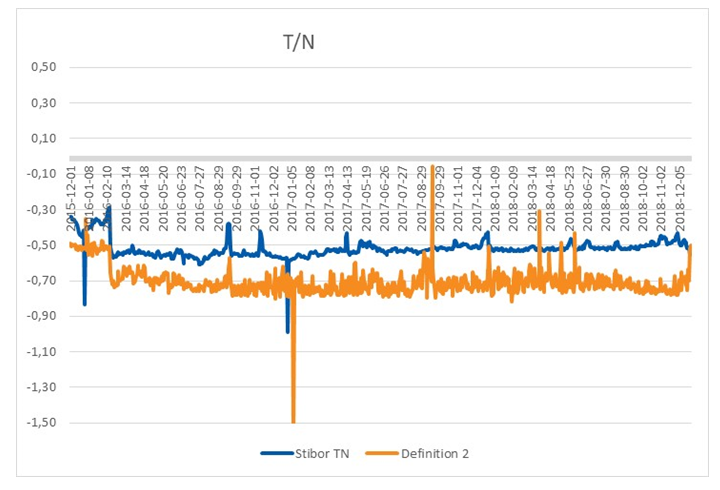

I did at least find out that STINA is not a “true” OIS rate. It is the compounded T/N fixing from the STIBOR panel banks. So it is still a survey-based rate (unlike SONIA, SOFR, Fed Funds etc).

STIBOR Today

This preliminary research led me to discover that there is a process underway to also introduce an alternative reference rate to STIBOR.

(I’m beginning to think that there isn’t a single ‘IBOR out there that isn’t going through some type of reform!).

Before we get there, here is a quick overview of where we currently stand with STIBOR:

- It is administered by a subsidiary of the Swedish Bankers Association. This subsidiary is called Financial Benchmarks Sweden.

- STIBOR is currently a survey-based rate covering seven banks.

- It is published for 6 maturities each day.

- It is not transaction based, but interestingly it does have an “entitlement” element.

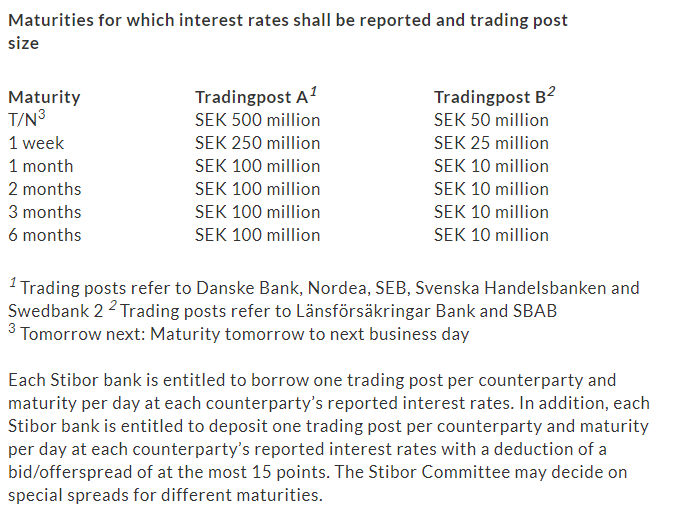

I have not seen this entitlement in other ‘IBORs before (readers, please correct me if I’m wrong). According to the below, each STIBOR bank can actually transact with another STIBOR bank on the fixing for that day in up to SEK500m:

Entitlements aside, this all seems pretty similar to other ‘IBORs around the globe. So let’s move on…

STIBOR Reform

A process to reform STIBOR – or rather to find an alternative reference rate for the Swedish market – is now underway. So far:

- There is a Working Group for Alternative Reference Rates.

- They have held a preliminary consultation.

I think it is therefore very early days for STIBOR reform or for any new rate. I do wonder if they have half an eye on EURIBOR, with some thinking that if EURIBOR can survive, maybe other term ‘IBORs are not quite doomed yet. But that is probably a discussion for another day….

STIBOR Reform Details

The consultation on Alternative Reference Rates is interesting, because the Swedish Bankers Association (the current administrator of STIBOR) have explained in pretty good detail why they have ended up focusing on unsecured lending in their final proposal.

The consultation is very much based on a data-collection exercise from the 7 STIBOR member banks. This involved:

- All secured and unsecured transactions from 2015-2018.

- Both interbank and customer trades.

- Both secured and unsecured.

- Covering tenors from overnight and tom-next to three months.

In a similar manner to the Norway consultation, the working group is looking for a rate that:

- Has transactions every day in “large enough volume” across a wide cross-section of the reporting banks.

- Moves in an expected manner, for example when the central bank (Riksbank) changes interest rates.

- Is not too volatile. I guess this is aimed especially at Repo rates that might jump at month/quarter/year ends.

- Is consistent with other RFRs around the globe but reflects the “particular conditions of the SEK market.”

All of this is designed to provide a reliable, transaction-based near Risk Free Rate for the SEK market. Whilst the consultation makes it very clear that STIBOR will continue to be published and is not expected to cease, this Risk Free Rate could serve as an important fallback in case anything does change….

Unsecured or Secured?

I found the consultation section on Secured lending transactions particularly interesting. What they found was:

- Most Tom-Next trades were Repos (i.e. secured lending).

- On average, 39 T/N trades were reported each day averaging SEK 17.7bn. Seems pretty good?

- However there were five days with fewer than five transactions during the three year period. It’s not great to need a fallback for your fallback rate on these days….

- The rate is evidently more volatile than the current Tom-Next STIBOR fixing and has a few surprising moves in the data history. We don’t get any particular explanation of why it moved on those days – anyone know the SEK Repo market well enough to comment below?

Let’s compare to the Unsecured transactions, which were:

- Mainly overnight transactions.

- On average, 50 O/N trades were reported each day averaging SEK 42bn. Even better!

- Between 5 and 7 banks participated every day.

- There were no days with less than five transactions.

And like that we end up with a pretty solid proposal to base any alternative reference rate in Sweden on overnight unsecured lending. It’s great when that decision can be arrived at thanks to solid data!

The Proposals

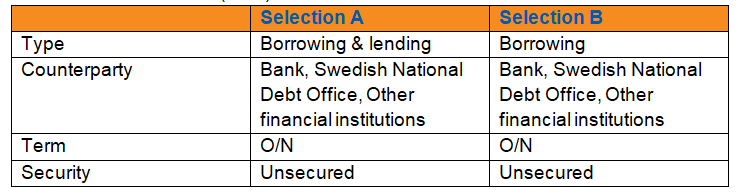

The Working Group still needs to finalise the details – namely whether the new rate (dubbed alt-STIBOR at Nordea) should be based on borrowing and lending data, or just data that results in the reporting bank lending money.

This new overnight rate must be a prime contender to become a discount rate in the future for swaps exposures – because it would make sense to have CSAs (and PAI calcs at CCPs) reference this rate. Should that be a “mid” market rate or a bank lending rate – discuss!

In Summary

- I’ve learnt that there is very little SEK OIS currently traded.

- There is work underway to launch an alternative reference rate for the SEK market.

- This is not expected to replace STIBOR, but rather to act as a fallback.

- The rate will be based on unsecured overnight transactions.

- At some point in 2019, the details will be finalised as to which exact transactions will make up the rate.