USD Fed Funds and the FHLBs

Get ready to geek out on some short-end USD Rates background. Fed Funds Fed Funds (as I know it), or the more official sounding “Effective Federal Funds Rate (EFFR)”, is a key overnight interest rate for USD. It didn’t quite cut the mustard as the official Risk Free Rate though – that title goes to […]

‘Dear CEO’ letters – Customer Impacts

Last month I wrote a blog that described the ‘Dear CEO’ letters sent to many financial firms from regulators in UK, EU, Switzerland, Australia and Hong Kong. Also the US FED has added a Libor component to their regular supervisory requirements to assess the transition from Libor to other benchmarks for firms they supervise. In […]

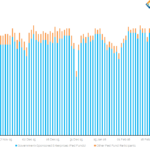

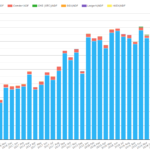

USD SOFR Swaps volumes on the up in Aug 2019

SOFR Swap trade volumes picked up significantly last week Trade counts in one week were half of the combined May and June totals Outrights were all executed Off SEF and the majority were cleared Basis were all executed on On SEF and were all cleared We show how Clarus Data Products can be used to […]

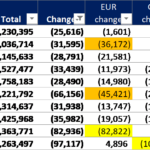

Compression in cleared Inflation Swaps

Since 2016, uncleared margin rules have driven a steady rise in cleared inflation swaps open interest and CCP IM. In July TriOptima announced their first cleared inflation swap compression run, so let’s look at what data on cleared volumes in CCPView tells us. Inflation swaps in the context of overall IRD volumes Inflation swaps are a somewhat specialised corner of the IRD […]

Swaps Data: Fed’s change of tack on rates fuels volume rise

My monthly Swaps Review looks at Q2 2019 volumes and CCP market share for: USD, EUR, JPY Swaps Credit Default Swaps Non-Deliverable Forwards Please click here for free access to the full article on Risk.net.

RFR Swaps and Futures Volumes July 2019

We recently added an RFR view in CCPView to show volumes and open interest of Swaps and Futures that reference risk free rates (RFRs), covering SOFR, SONIA, SARON and AONIA. Lets look at what the data shows for July 2019 and prior months. SOFR Futures Showing July 2019 a new high at CME with $2.25 […]

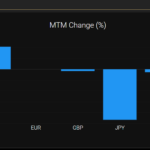

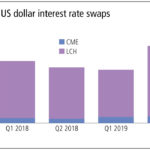

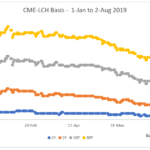

CME-LCH Basis narrows to four year low

Our recent blog, CCP Basis – The Cost of Clearing Fragmentation, proved very popular and while this was published on July 30, 2019, it was actually written a few weeks earlier. As is often the case with these things, there have been major new market developments in the CME-LCH Basis, meaning we need to do […]

FXD Counterparty Risk Optimization and Q2 2019 Volumes

FX Derivatives (FXD) participants face a tricky choice across a patchwork of clearing and uncleared optimization techniques, trading off funding and capital usage with infrastructure spend and operational risk. In earlier posts, we showed you how FX IM optimization via NDFs and FX Options clearing developed in Q1 2019. Here I update the volumes for […]

CCP Basis – The Cost of Clearing Fragmentation

Staff Working Paper No. 800 from the Bank of England was published in May 2019. Titled “The Cost of Clearing Fragmentation”, the paper lays out a quantitative process to model the level of CCP basis. We’ll give you a layman’s guide to the paper here and show how our own data from CCPView can be […]

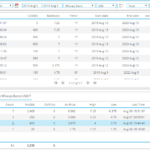

CPMI-IOSCO Quantitative Disclosures 1Q 2019

Clearing Houses 1Q 2019 CPMI-IOSCO Quantitative Disclosures are now available, so lets look at what the data shows, similar to my CCP Disclosures 4Q 2018 article. Summary: IM is up for IRS, CDS & ETD with YoY growth of 6%, 15%, 10% respectively Quarter-on-Quarter IM in CDS was flat ICE Europe F&O and ASX CLF IMs were […]