Key takeaways:

- SDRView capabilities to analyze trade packages and platforms bring IRD compression activity and market share into sharp relief.

- 2024 US reported IR derivatives (IRD) compression activity was one-third of all IRD trades – by no means a niche activity.

- This activity is dominated by was cleared compression shared mainly among D2C platforms (TradeWeb, Bloomberg), D2D platforms (BGC, TP ICAP, Tradition, GFI), reset compression platforms (Reset, Matchbook) and off-platform bilateral compression.

- The much smaller uncleared compression activity is mostly off-platform, with on-platform (TradeWeb, Bloomberg, BGC) making up only 10%.

Data background

For 8+ years, SDRView data has included the package type field to allow compression to be broken out from outright and other package types. In late 2022 we used the CFTC reporting upgrade to immediately add platform id which allows platforms’ compression market share to be analyzed. Platform id values consist of 4-letter market identifier codes (MICs) each of which represent a platform legal entity or off-platform category. MIC codes can be googled or looked up on TradingHours.com to find the legal entity name from which you can deduce the group ownership, type of platform and location etc. To help you read this post without looking up one by one, here is a quick summary:

| platform type | platform owner or category (platform ids/MIC codes) |

| off-platform (NA) | platform tradeable product bilateral trade (BILT) non-platform tradeable product (XXXX, XOFF) |

| dealer to dealer SEF/OTF/MTF (D2D) | BGC (BGCD, BGCO) GFI (GFIC, GSEF) OSTTRA Reset (REST) TP ICAP (ICOT, IMRD, IOIR, ISWE, ISWV, TIRD, TPIR, TPSE) Tradition (TCDS, TSEF) |

| dealer to client SEF/OTF/MTF (D2C) | Bloomberg (BBSF, BMTF, BTFE) TradeWeb (TREU, TRWB, TWEM, TWSF) |

| single dealer platform (SDP) | BNP (BNPS) |

Note 1: SDRView includes non-US platforms (such as European OTFs and MTFs) but excludes trades not reported to SDRs (where both parties are not US-reporting entities). By contrast, SEFView excludes non-US platforms but includes trades not reported to SDRs. Sorry, the regs just work that way!

Note 2: two prominent compression types are not reported to SDRs: CCP blending and CCP vendor compression. These are reg reported through other channels than SDRs.

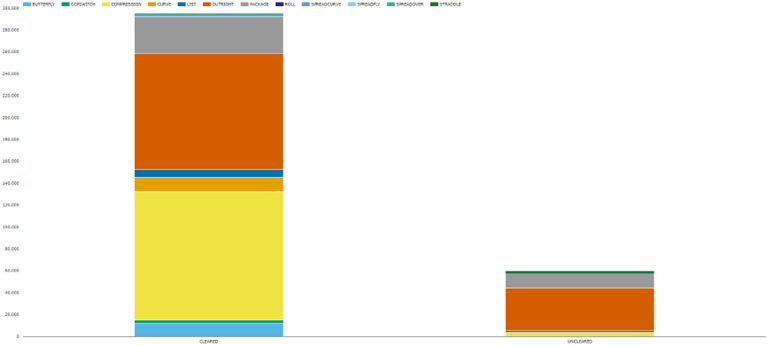

2024 OTC IR trades

We start by putting compression in the context of all 2024 US reported IR trades. These amounted to $355.4 trillion notional, of which compression was a solid one third.

Chart 1 – 2024 US reported G4 OTC IR trades by package type (notional $billions)

Source: SDRView

The larger components we see are:

- Outright cleared trades of $106 trillion (30%).

- Compression of cleared trades of $117 trillion (33%).

- Other cleared package types of $72 trillion (20%).

- Outright uncleared trades of $39 trillion (11%).

- Compression of uncleared trades of $3.5 trillion (1%).

- Other uncleared package types of $18 trillion (5%).

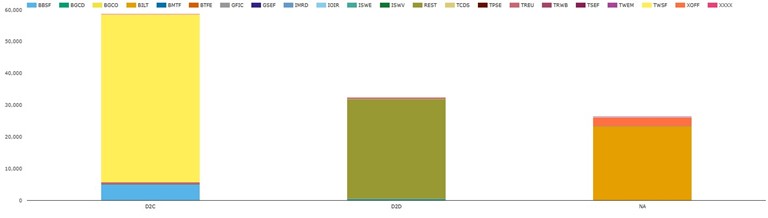

Cleared compression by platform

Analyzing by platform type and platform id shows the $117 trillion of cleared compression activity in sharper relief.

Chart 2 – 2024 US reported G4 cleared IRD compression by platform (notional $ billions)

Source: SDRView

We see:

- D2C SEF compression: 46% is TradeWeb (TWSF, TREU, TRWB, TWEM) with $53 trillion, 4.4% is Bloomberg (BBSF, BMTF, BTFE) with $5.2 trillion.

- Reset and cash flow compression: 27% is OSTTRA Reset (REST) with $32 trillion, TP Matchbook activity is embedded in the D2D SEF compression of TP ICAP below.

- D2D SEF compression: 1.2% is BGC (BGCD, BGCO) with $351 billion, 0.0% is TP ICAP (ICOT, IMRD, IOIR, ISWE, ISWV, TIRD, TPIR, TPSE) with $208 billion, 0.0% is Tradition (TSEF, TCDS) with $142 billion and 0.0% is GFI (GSEF) with $62 billion.

- Off-platform bilateral compression (NA): 22% of cleared is bilateral (BILT) with $26.5 trillion, 2.6% is off-platform (XOFF, XXXX) with $3.1 trillion.

Without including product charts, I can say that most cleared compression activity is OIS while EUR FRA dominates the OSTTRA Reset activity.

Cleared compression types outlined

Taking each type in turn:

- Cleared D2C SEF compression was created as a form of list trading aiming to help participants, especially hedge funds when they have completed a trading strategy and the associated portfolio is risk-flat and profit is locked-in. Ordinarily, the portfolio would run several years to the maturity releasing the cash profit over time. SEF compression allows the portfolio to be assigned to a dealer with minimal risk transfer and releasing the NPV as a cash fee. In the cleared case, the buy side firm submits the required set of offsetting trades are submitted as a list trade RFQ. Once executed and cleared then pairs off and terminates in firm’s client clearing account effectively transferring the trades to the dealer counterparties clearing account.

- Reset and cash flow compression was created by OSTTRA Reset and TP Matchbook as a multilateral run based services to enable are participants (mostly banks) to streamline near-term settlements and reset risk inherent in their OTC IRD portfolios. Their multilateral periodic runs solve for mutual settlement and reset reduction, minimal IR risk change per participant and at the same time do not reveal participants’ positions to one another.

- Cleared D2D SEF compression was created by BGC, TP ICAP, Tradition and GFI and works similarly to D2C SEF compression. The volumes are lower than D2C SEF compression, I think, because dealers would rather permanently GSIB notional reduction via CCP blending and vendor compression.

- Off-platform bilateral compression even predates CCP blending and vendor multilateral compression as the original form of cleared IRD compression.

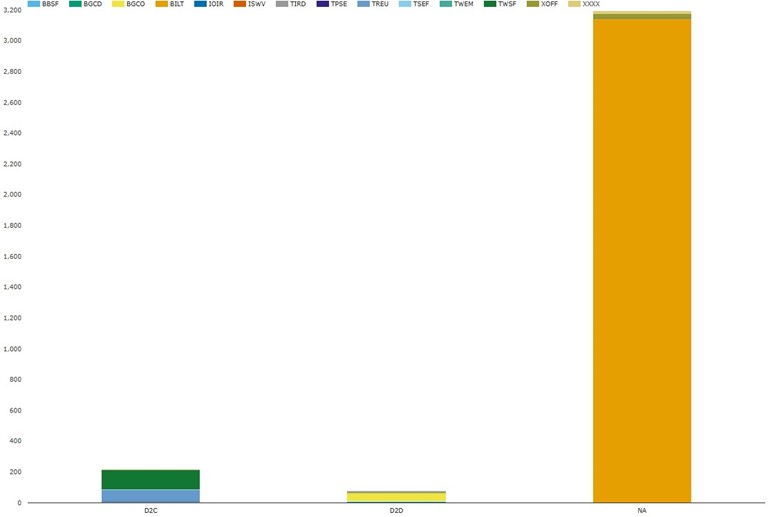

Uncleared compression by platform

Now we look at platform type and platform id level at the 2024 reported $3,487 billion notional of uncleared compression.

Chart 3 – US SDR reported 2024 G4 uncleared IR compression by platform (notional $ billions)

Source: SDRView

We see:

- Off-platform bilateral compression: 90.2% is Bilateral (BILT) with $3,141 billion (of which $2,892 billion is OIS and $237 billion is swaptions), 1.5% is off-platform (XOFF, XXXX) with $52 billion (almost all OIS).

- Uncleared D2C SEF compression: 5.9% is TradeWeb (TWSF, TREU, TWEM) with $204 billion (almost all OIS), 0.3% is Bloomberg (BBSF) with $1.1 billion (all OIS).

- Uncleared D2D SEF compression: 1.9% is BGC (BGCD, BGCO) with $66 billion (all swaptions), 0.2% are the other D2D platforms with $7.7 billion.

All three categories of uncleared compression generally work by good, old-fashioned terminations with original party or assignment to a third party. These relatively costly and cumbersome processes limit the practicality of more material volumes. The only exception here is the BGC volumes which are all swaptions. The monthly periodic spikes can be seen if you do a daily plot of D2D package type uncleared activity by platform id. These suggest BGC swaption compressions arise mainly from periodic runs of Capitalab’s swaption-based multilateral IR IM optimization service (which I blogged about before here).

Summary

When used in conjunction with the other parameters and analysis capabilities of SDRView, the platform id and package type fields allow us to know much about compression volumes and platform market share.

Showing as a third of all SDR reported activity, compression is much more than an esoteric activity.

For those thirsty for more compression analysis, please look at:

- Daily plots showing activity spikes of multilateral compression services such as Reset and Capitalab.

- Product specific compression analysis showing where non-OIS products are being compressed.

- Comparison of SDRView plots with those from other ClarusFT data products to corroborate compression patterns shown.

Please contact us for information on any of SDRView, SEFView or CCPView or more details on any of the above.