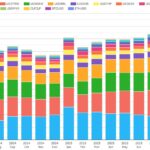

FX derivatives volumes at the end of Q3 2025

This blog covers the volumes of FX derivatives (FXD) in September 2025, as reported by CCPs and to US SDRs. Key takeaways: A year-on-year (YoY) comparison of volumes between September 2025 and September 2024 shows that: Analysis by product group showed that clearing rates for NDFs on deliverable pairs are aligned with those for FX […]

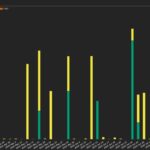

Rates IM optimization and swaption terminations

In our June blog on rates IM optimization, we used SDR-reported swaption trade volume spike days from BGC’s London-based OTF platform to spot rates Capitolis IM optimization runs. Today, we look for signs of similar services from other optimization vendors in Q2 and Q3 2025 swaption volumes. Key takeaways Background There are three main players […]

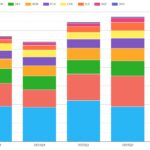

Q3 2025 CCP volumes and share in IRD

Clarus CCPView has daily volume and open interest (OI) data published by each CCP, which is filtered, normalized, and aggregated to allow meaningful volume comparisons. This blog looks at single-sided gross notional volume in vanilla cleared rates swaps referencing IBORs and RFR indexes for quarter three (Q3) 2025 and the prior four quarters in all major currencies and regions. Key takeaways: […]

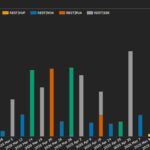

Reset optimization: part 2 – SPS activity

In part 1 of this blog, we promised to follow up with part 2. Here it is. Key takeaways Background In Part 1, we estimated that, of the $31.1 trillion SDR-reported FRA activity in H1 2025, reset optimization-driven FRA spike days from OSTTRA’s Reset service and Tullett Prebon’s Matchbook service (formerly “tpMatch”) totaled $25.0 trillion. […]

Reset optimization: part 1 – FRA activity

Our recent blog noted that FRA compressions were $18.8 trillion of the total $97.4 trillion SDR-reported in H1 2025. The $18.8 trillion FRA compressions were dominated by the EUR currency and by the OSTTRA REST platform. I skipped further analysis to tee up a separate analysis in this blog. Key takeaways Background Multilateral reset optimization […]