In our June blog on rates IM optimization, we used SDR-reported swaption trade volume spike days from BGC’s London-based OTF platform to spot rates Capitolis IM optimization runs. Today, we look for signs of similar services from other optimization vendors in Q2 and Q3 2025 swaption volumes.

Key takeaways

- We can use SDRView to identify the main monthly runs of each rates IM optimization vendor.

- BGCO D2D platform volume spike days in new swaption trades (excluding compressions) show us the main Capitolis runs. There were six such run days in Q2 and Q3 2025.

- Off-platform trade compression volume spike days show us the main runs of the other two vendors – Quantile and TriBalance. There were twelve such runs in the same period.

Background

There are three main players in uncleared rates IM optimization. Though not directly relevant here, all three have been subject to recent merger and acquisition activity (with links to sample press releases):

- Capitolis rates IM optimization was part of Capitolis’ December 2024 acquisition of Capitalab from BGC.

- Quantile rates IM optimization was part of LSEG’s December 2022 acquisition of Quantile.

- TriBalance rates IM optimization was part of CME’s November 2018 acquisition of NEX. In September 2021, TriBalance became part of OSTTRA. In October 2025, KKR acquired OSTTRA.

To save detailed re-reading of the prior blog, here are the key points on which I base today’s analysis:

- In that blog, we used swaption new trade volume spikes under platform id BGCO in SDRView to spot the Capitolis runs earlier in the year.

- Capitolis rates optimization runs produce spikes days in the volumes of new swaption trades (executed via BGC’s London OTF), and of swaption terminations (executed via post trade affirmation vendors, such as MarkitWire).

- For IM optimization runs, the terminations volumes represent the removal of new swaptions put on in the prior run.

- For LIBOR swaption conversion runs, the terminations represent the removal of the LIBOR swaptions being converted.

- Each vendor has one main rates IM optimization run per month.

In addition, we assume that no two rates IM optimization runs by different vendors occur on the same date, and that the main rates IM optimization runs of Quantile and TriBalance also produce material volumes of swaption new trades and terminations.

For this blog, we cover Q2 and Q3 2025, but we start on 31 March and end on 28 September to include whole groups of days from Monday to Friday.

Terminations terminology

Being uncleared, swaptions terminations are a type of trade amendment – agreed between the original two parties to the trade – which brings the trade maturity date forward from its future date to the present. A fee is settled between the parties to compensate for the change in value of the trade.

A cleared swap SEF compressions result in termination for one party and a new trade for the other party, that is, a “one-sided termination”. However, unlike cleared swaps, there is really no SEF compression market for swaptions. Other one-sided terminations, like assignments and step-ins, are not separately coded in the SDR-reporting. I suspect that they are low in volume, given the operationally cumbersome nature of the transactions. For simplicity, we assume all SDR-reported swaptions compressions (trades with compression package type) and all SDR-reported swaptions terminations (terminations with any package type including outright, package, and compression) are two-sided terminations.

Simply put, Banks can report a swaption termination resulting from a vendor IM optimization run as, either a “trade compression” (a trade with package type compression), or a “termination” (a termination with any package type).

New swaptions trades

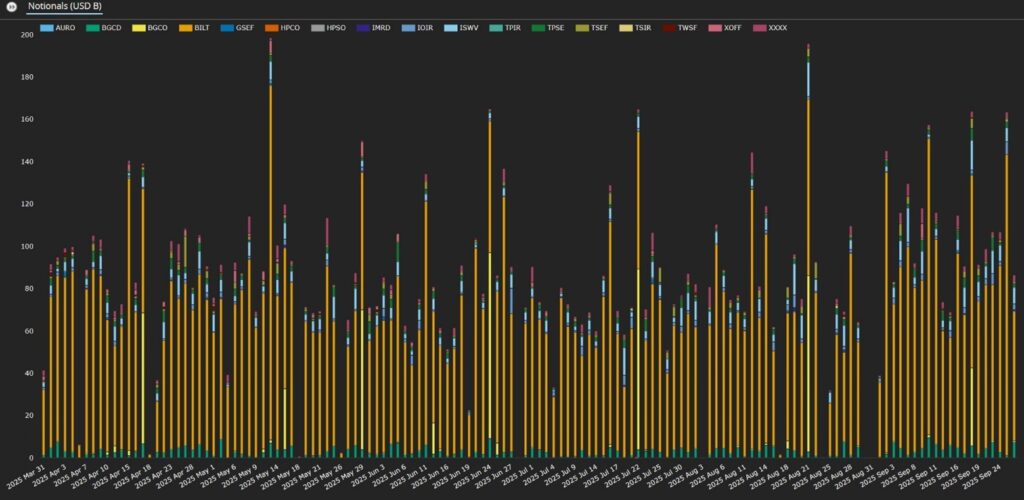

We start with an updated chart of swaption new trade volumes by platform (excluding compressions).

Chart 1: SDR-reported new swaption trades (excluding compressions) by platform (notional $ billions). Source: SDRView.

As we saw in the recent blog, chart 1 naturally highlights the Capitolis runs in the form of spike days in BGCO platform new swaptions.

- Once a month, we see larger BGCO spike days (in yellow), following the IM optimization run frequency Capitolis confirmed. These were typically on Thursdays, ranged between $37 billion and $88 billion, and totaled $421 billion.

- There are two smaller BGCO spike days in May and June (between $15 billion and $29 billion).

- Activity from other D2D platforms is much smaller in volume, but hard to analyze at this scale.

- Off-platform activity – mainly BILT (in orange) – dominates the rest of the volume, both on and off Capitolis run days. We could speculate that these figures include new swaption trade spike days from Quantile and TriBalance runs. However, the regular daily volume is large enough to make it hard to draw a line between optimization run days and other days.

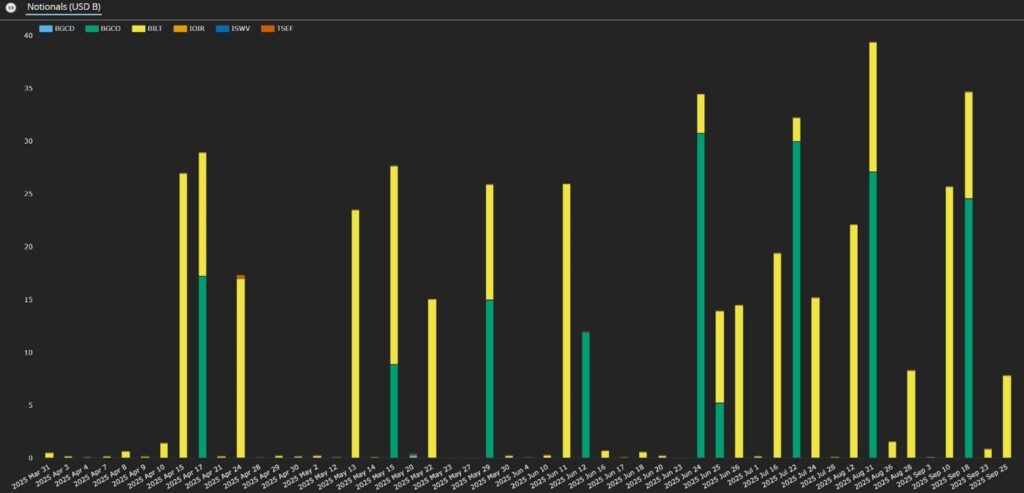

Let us focus on trades on D2D platforms only.

Chart 2: SDR-reported new D2D platform swaption trades (excluding compressions) by platform (notional $ billions). Source: SDRView.

Chart 2 shows that:

- The BGCO new trades have spike days on the same eight days as observed in chart 1.

- Other D2D platforms’ activity is more visibly delineated, and there are no clear spike days.

Swaptions terminations

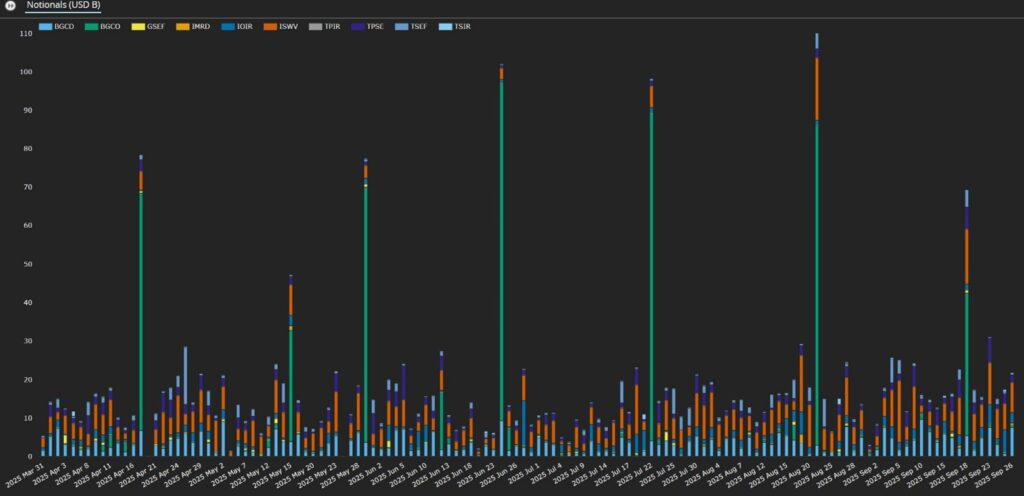

Now, we turn to terminations, starting with trade compressions.

Chart 3: SDR-reported swaption trade compressions by platform (notional $ billions). Source: SDRView.

Chart 3 is the trade compression subset of the volumes from chart 1, that is only trades with package type “compression”.

- BGCO / Capitolis has trade compressions on only nine days in the period (between $5 billion and $31 billion). These included the eight days identified in chart 1, plus 25 June, which may be a MarkitWire processing spillover from 24 June.

- Other D2D platforms had trade compression on only four days in the period (between $7 million and $336 million).

- Off-platform (BILT) trade compressions were above $2 billion on seven of the eight Capitolis run days (between $3 billion and $19 billion).

- Off-platform (BILT) trade compressions were also above $2 billion on twelve further days each month (between $7 billion and $27 billion), typically Tuesdays or Thursdays.

- Off-platform (BILT) trade compressions occurred on only 26 of 89 other days in the period (between $4 million and $1.54 billion)

I elaborated the analysis to show the sparseness of the volumes outside those days above $2 billion.

I suggest the twelve further days highlighted are likely to be the main rates IM optimization run days for Quantile or TriBalance.

Now, we look at the second kind of swaption terminations (with all package types).

Chart 4: SDR-reported swaption terminations (all package types) by platform (notional $ billions). Source: SDRView.

Chart 4 shows a mixed picture of IM optimization activity and non-IM optimization daily terminations.

- BGCO / Capitolis has termination volume on only 11 days in the period of which eight are above $1 billion and correspond to the eight Capitolis run days identified in chart 1.

- Off platform – mainly BILT (in yellow), XOFF, and XXXX – dominates the regular daily volume but also has above $2 billion on seven of the eight Capitolis days noted in chart 1, and on the twelve Quantile and TriBalance main run days noted in chart 3.

Overall, the terminations in charts 3 and 4 fit the expected pattern of one main run per month per vendor. It looks like Capitolis run terminations are reported as either BGCO or off-platform trade compressions or terminations, while Quantile or TriBalance run terminations are reported as off-platform trade compressions or terminations.

The off-platform volumes of new trades (chart 1) and terminations (chart 4) are co-mingled with regular daily activity. Thus, it is more difficult to estimate the fraction of those volumes produced by optimization runs, and arrive at precise run volume estimates. I will leave those of you with SDRView to have a go if you like.

End note

- To recap the key takeaways, jump back to the section near the top.

- We expect to update regularly on IM optimization in the future.

Contact us if you are interested in a subscription.