Today, we look at trading platforms’ September 2025 market shares of volumes of OTC interest rate derivatives (IRD). If you prefer, you can skip to the end for a summary of market share statistics before returning to the start to read the details.

Volume context for platform market shares

Throughout this blog, we look at the volumes and platform shares of SDR-reported rates OTC trades over the 15-month period from 01 July 2024 to 30 September 2025. This timeframe allows year-on-year (YoY) and quarter-on-quarter (QoQ) comparisons of September 2025 volumes.

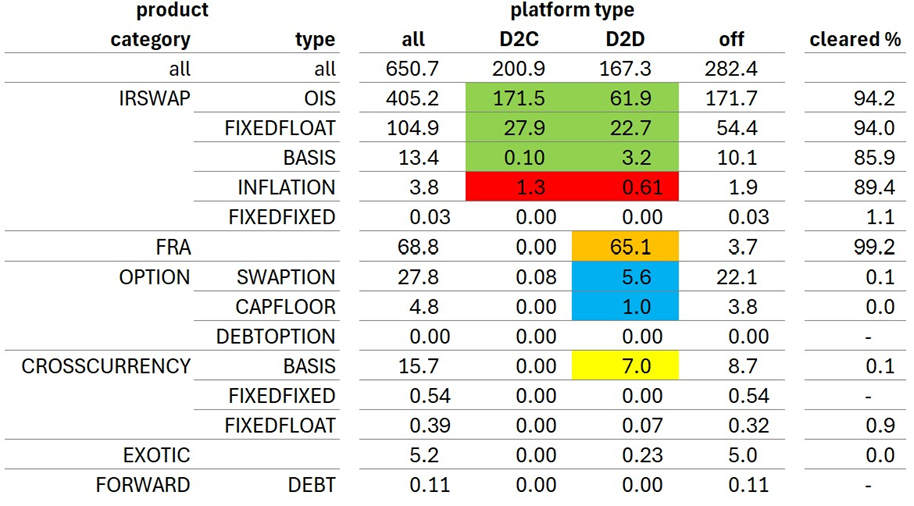

Table 1: 15-month period total SDR-reported IRD volumes by product type and platform type (notional $ trillion). Source: SDRView.

Table 1 comes from a single query in SDRView. For more visibility of smaller but important product and platform combinations, I downloaded, pivoted, and manually highlighted the statistics.

The table shows total SDR-reported IRD for the 15-month period of $651 trillion. There was on-platform activity comprising $201 trillion dealer-to-client (D2C) platform activity, and the $167 trillion dealer-to-dealer (D2D) platform activity. We focus on the amounts color-highlighted in the table, while omitting further analysis of the unhighlighted D2D and D2Camounts, which total $0.37 trillion.

As not all currencies have ceased using their IBOR index, we combine OIS, fixed-float swaps, and basis swaps (highlighted in green) as “core rates swaps”. These combined for $287 trillion. Without analyzing by currency in a chart, take my word that the major six currencies dominate volumes of on-platform rates trading in each product.

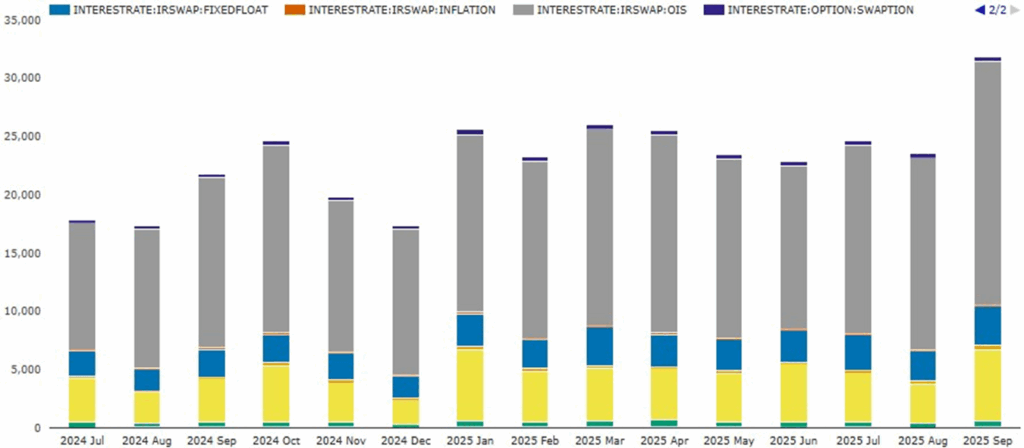

As context for market shares below, we look at the month-by-month on-platform volumes over the same 15-month period as in Table 1.

Chart 1: 15-month period on-platform SDR-reported volumes by material product (billions of $ notional). Source: SDRView.

Chart 1 shows the month-by-month breakdown of the combined $201 trillion D2C-executed and the $167 trillion D2D-executed trade volumes. 2025 has seen “new normal” volumes with all months in 2025 beating most months in 2024 and before. September 2025 on-platform volumes totaled $31.9 trillion, up 46 percent YoY, and up 39 percent QoQ. September 2025 was a record month — with volumes up 22 percent from the previous record of $26.1 trillion set in March 2025.

- Core rates swaps (combining OIS in gray, fixed float swaps in blue, and basis swaps in light orange) totaled $24.5 trillion in September 2025 — up 43 percent YoY, and up 45 percent QoQ.

- Inflation swaps (dark orange) had $137 billion, down 8.0 percent YoY, and down 4.5 percent QoQ.

- FRAs (yellow) were $6.2 trillion, up 64 percent YoY, and up 25 percent QoQ.

- Rates options (swaptions in navy blue plus cap/floors in sky blue) had $545 billion, up 35 percent YoY, and up 9.9 percent QoQ.

- Cross-currency basis swaps (green) had $497 billion, up 32 percent YoY, and up 10.1 percent QoQ.

Now, let us look at platforms’ market shares in each product in September 2025.

Core rates swaps platform shares

Here, we home in further on core rates swaps trading. To do this, we split out compression packages into separate charts, move single-period swaps (product subtype SPS) out of core rates swaps, and combine them with FRAs in the later section instead.

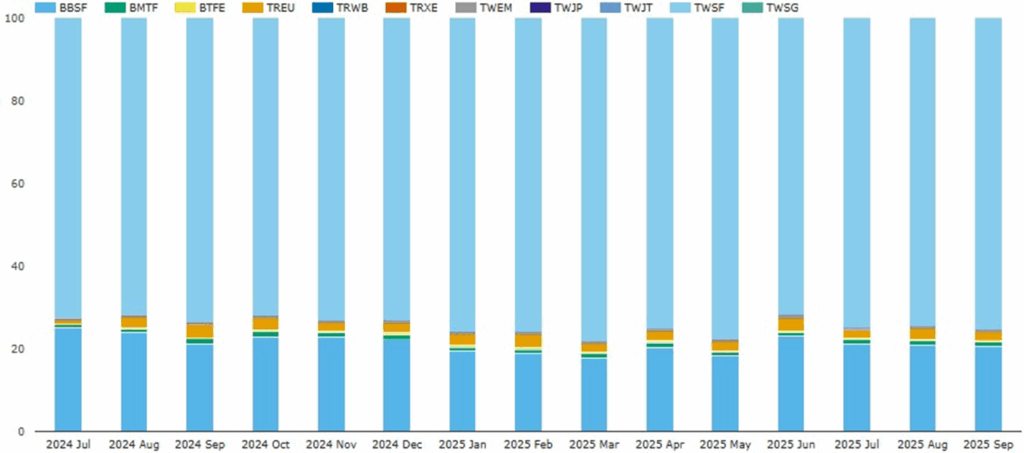

Our next chart is therefore D2C platform shares of core single-currency swaps trading.

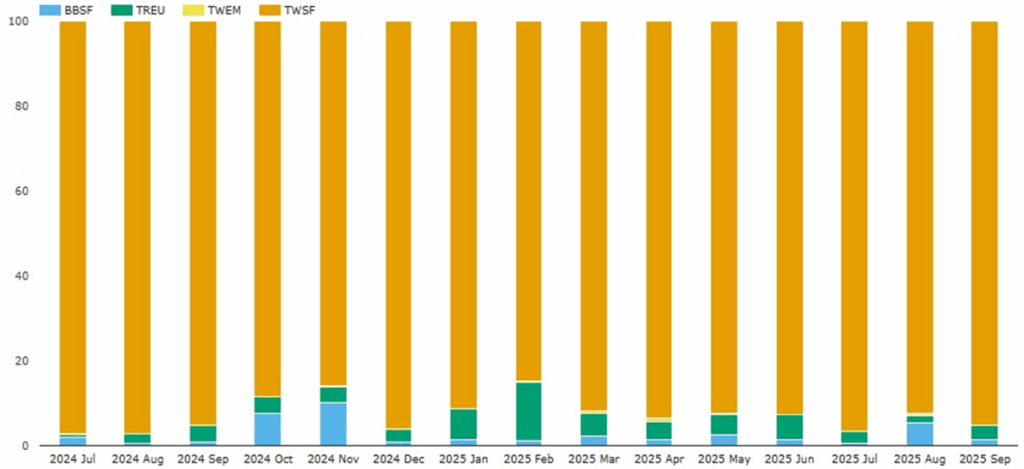

Chart 2: SDR-reported D2C platform share of core rates swaps trading (notional percentage). Source: SDRView.

Chart 2 shows TradeWeb dominating September 2025 D2C platform core single-swaps trading.

- TradeWeb (mainly TWSF in sky blue, but also TREU, TWEM, TWJP, TWSP, TWJT) led with a combined 82.4 percent share – down from 83.3 percent YoY and down from 84.8 percent QoQ.

- Bloomberg (mainly BBSF in mid blue, but also BMTF and BTFE) had a combined 17.5 percent share – up from 16.6 percent YoY and up from 15.1 percent QoQ.

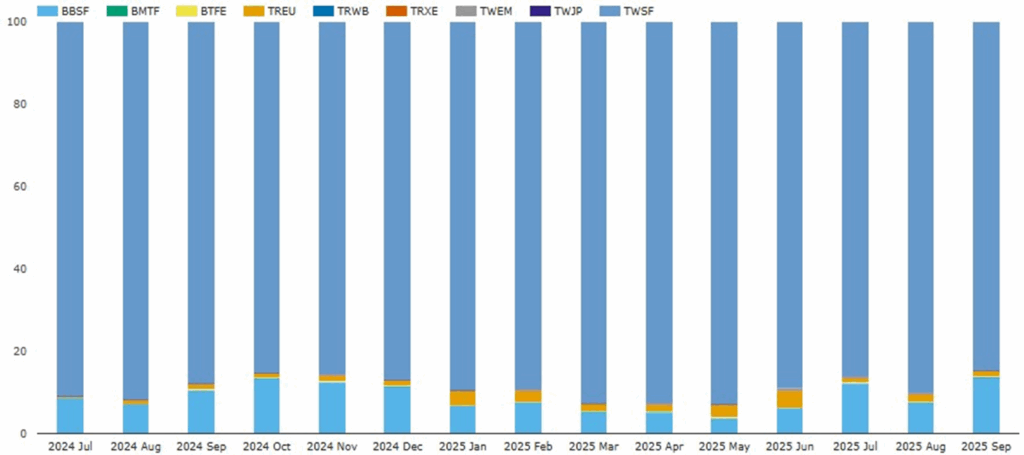

We move onto D2C platform shares of core single-currency swaps compression.

Chart 3: SDR-reported D2C platform share of core rates swaps compression (notional percentage). Source: SDRView.

Chart 3 shows Tradeweb dominating September 2025 D2C platform core single-swaps compression.

- Tradeweb (mainly TWSF in darker blue, but also TREU, TRWB, TWEM, TWJP) led with a combined 86.3 percent share — down from 89.4 percent YoY, and down from 93.7 percent QoQ.

- Bloomberg (mainly BBSF in mid blue, but also BMTF and BTFE) had a combined 13.7 percent share — up from 10.6 percent YoY, and up from 6.3 percent QoQ.

Next, we have D2D platform shares of core single currency swaps trading.

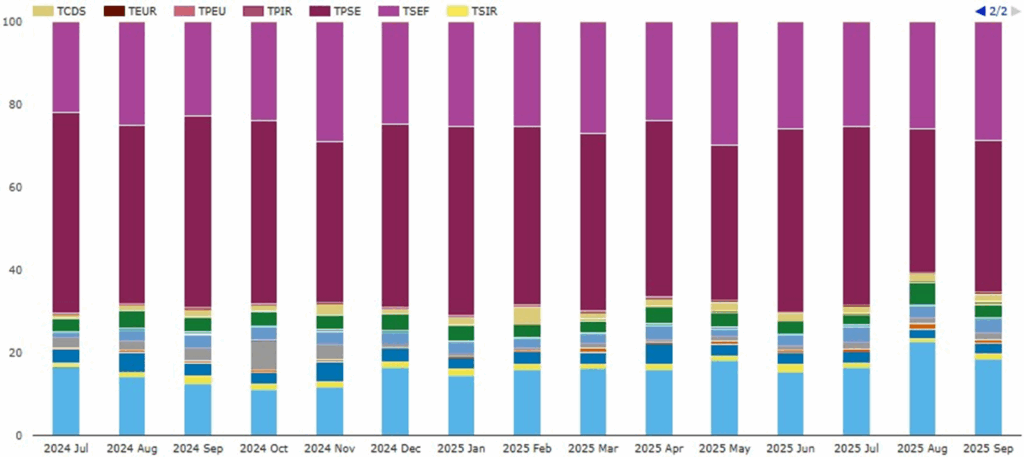

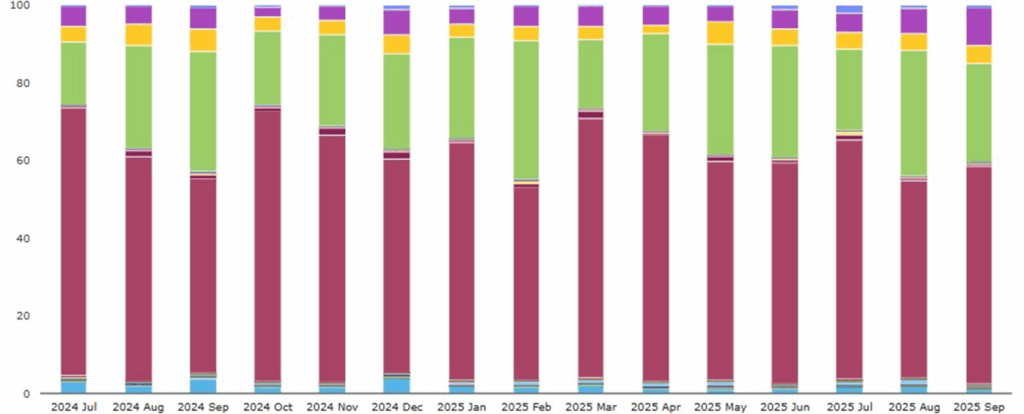

Chart 4: SDR-reported D2D platform share of core rates swaps trading (notional percentage). Source: SDRView.

Chart 4 shows the September 2025 D2D platform market shares of core rates swaps trading shares in comparison with the other months in the 15-month period.

- TP ICAP (mainly TPSE in magenta, but also IMRD, ISWV, ISWE, TPIR, TWJT) led with a combined 43.4 percent share – down from 53.8 percent YoY, and down from 50.0 percent QoQ.

- Tradition (mainly TSEF, but also TCDS and TEUR) took a combined 31.0 percent share — up from 24.8 percent YoY, and up from 27.9 percent QoQ.

- BGC (mainly BGCD, but also BGCO, BGCF, GSEF, GFSO) took a combined 22.3 percent share — up from 18.0 percent YoY, and up from 18.7 percent QoQ.

- Dealerweb (DWSF) was the only other platform above 1 percent, taking 2.6 percent share — down from 3.1 percent YoY, and down from 2.9 percent QoQ.

During the 15-month period, BGC and Tradition between them steadily took away about 10 percent of TP ICAP’s market share.

Now, we look at D2D platform shares of core single-currency swaps compression.

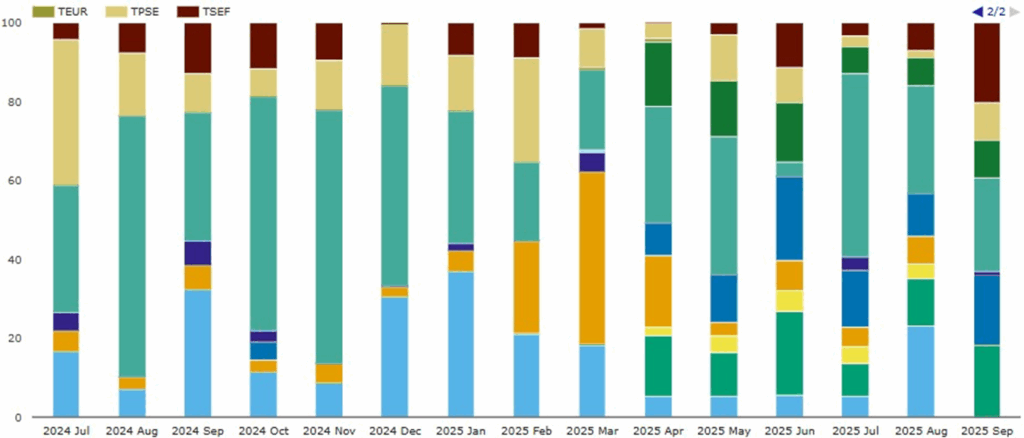

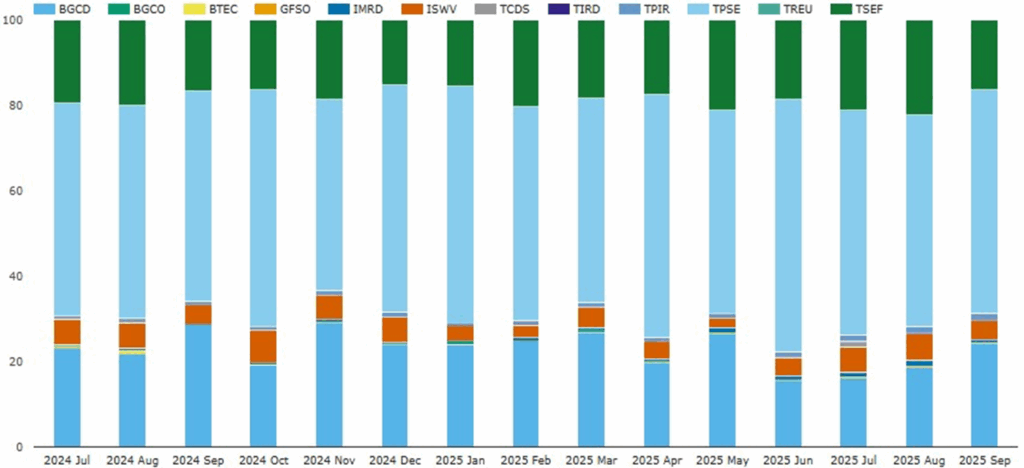

Chart 5: SDR-reported D2D platform share of core rates swaps compression (notional percentage). Source: SDRView.

Chart 5 shows the September 2025 D2D platform market shares of core rates swaps risk compression in comparison with the other months in the 15-month period.

- Tradition (mainly TSEF, but also TCDS and TEUR) took a combined 29.9 percent share — up from 11.5 percent YoY, and up from 26.2 percent QoQ.

- TP ICAP (mainly TPSE, but also IMRD, ISWV, IOIR, ISWE) had a combined 28.3 percent share — up from 14.4 percent YoY, but down from 29.8 percent QoQ.

- Reset (REST) took a 23.6 percent share — down from 39.6 percent YoY, but up from 4.6 QoQ.

- BGC (mainly BGCD, but also BGCO, BGCF, GSEF, GFSO) had an 18.1 percent share — down from 34.4 percent YoY, and down from 39.4 percent QoQ.

Though at platform ID level, the chart shows constant shifts in share, at group-level over the period we have seen each of Tradition and TP ICAP take away 14 percent or more from each of Reset and BGC.

Inflation swaps platform shares

We start with D2C platform shares.

Chart 6: SDR-reported D2C platform share of inflation swaps volumes (notional percentage). Source: SDRView.

Chart 6 shows the September 2025 D2C platform market shares of inflation swaps trading in comparison with the other months in the 15-month period.

- Tradeweb (mainly TWSF, but also TREU, TWEM) had a combined 98.6 percent share — down from 99.1 percent YoY, and down from 98.7 percent QoQ.

- Bloomberg (BBSF) took a 1.5 percent share — up from 0.9 percent YoY, and up from 1.28 percent QoQ.

We move onto D2D inflation swaps.

Chart 7: SDR-reported D2D platform share of inflation swaps (notional percentage). Source: SDRView.

Chart 7 shows the September 2025 D2D platform market shares of inflation swaps trading in comparison with the other months in the 15-month period.

- BGC (mainly BGCD, but also BGCO, BGCF, GSEF, GFSO) took a combined majority share of 72.4 percent – up from 66.2 percent YoY, but down from 77.2 percent QoQ. A sizable chunk of BGCDs share shifted from BGC’s GFI SEF GSEF) in August and September 2025.

- TP ICAP (TSIR, TPIR, IMRD, IOIR, and TPSE) took a combined 17.6 percent share — down from 18.2 percent YoY, but up from 14.5 percent QoQ.

- Reset (mainly REST, but also RESF) had a combined 9.5 percent share — down from 14.2 percent YoY, but up from 7.9 percent QoQ.

- Tradition (mainly TSEF, but also TCDS and TEUR) took a combined 0.6 percent share — down from 1.3 percent YoY, but up from 0.4 percent QoQ.

D2D inflation shares were stable with the main shift being within BGC from BGCD to GSEF.

FRAs and SPS D2D platform shares

We move onto FRAs and single-period interest rate swaps (SPS). Both products are used for reset exposure hedging and management.

Chart 8: SDR-reported D2D platform share of FRAs and SPS combined (notional percentage). Source: SDRView.

Chart 8 shows the September 2025 D2D platform market shares of FRAs and SPS combined in comparison with the other months in the 15-month period.

- OSTTRA Reset FRAs and SPS (mainly REST FRAs in deep pink) had a combined 56.6 percent share — up from 51.0 percent YoY, but down from 57.6 percent QoQ. Exclusively, these FRAs are from scheduled reset optimization runs.

- TP ICAP FRAs and SPS (mainly TSPE FRAs in light green and TPSE SPS in orange) had a combined 30.6 percent share – down from 37.7 percent YoY, and down from 33.8 percent QoQ. A large chunk of this share is partly from scheduled reset optimization runs.

- Tradition FRAs and SPS (mainly TSEF FRAs in light purple) had a combined 11.1 percent share — up from 6.6 percent YoY, and up from 6.7 percent QoQ.

- BGC FRAs and SPS (mainly BGCD FRAs in pale blue) had a combined 1.6 percent share — down from 4.6 percent YoY, and down from 1.9 percent QoQ.

D2D FRAs and SPS shares were stable over the period. See our recent blogs on reset optimization with FRAs and SPS for deeper volumes analysis.

Rates options D2D platform shares

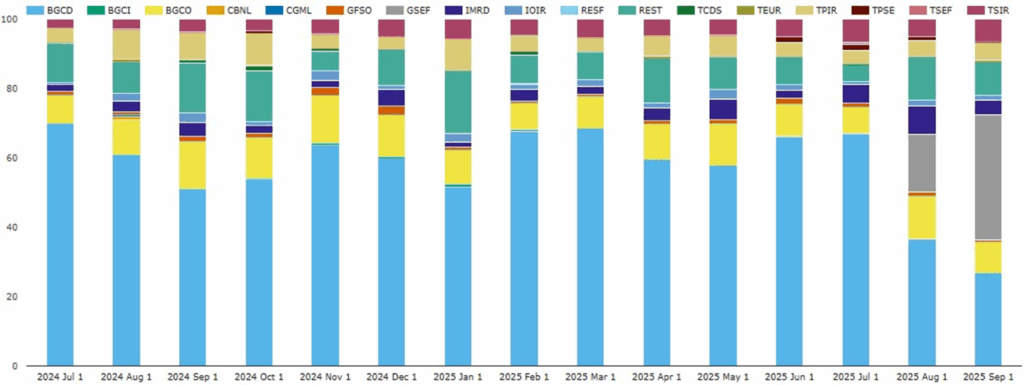

Chart 9: SDR-reported D2D platform share of rates options (notional percentage). Source: SDRView.

Chart 9 shows the September 2025 D2D platform market shares of rates options in comparison with the other months in the 15-month period.

- TP ICAP (mainly ISWV, but also BTEC, IMRD, IOIR, TPIR, TPSE, and TSIR) led with a combined 53.6 percent share —down from 56.2 percent YoY, but up from 40.1 percent QoQ.

- BGC (mainly BGCD, but also BGCO and GSEF) was next with a combined 34.2 percent share — up from 28.3 percent YoY, but down from 50.5 percent QoQ. This share would have been helped by Capitolis rates IM optimization run volumes — see our recent blog for more information.

- Tradition (TSEF) had an 11.4 percent share — down from 14.9 percent YoY, but up from 8.9 percent QoQ.

Options D2D platform market shares were up and down during in the period.

Cross-currency basis swaps D2D platform shares

Chart 10: SDR-reported D2D platform share of cross-currency basis swaps (notional percentage). Source: SDRView.

Chart 10 shows the September 2025 D2D platform market shares of cross-currency basis swaps in comparison with the other months in the 15-month period.

- TP ICAP (mainly TPSE, but also BTEC, IMRD, ISWV, and TPIR) led with a combined 58.8 percent share — up from 54.1 percent YoY, but down from 65.6 percent QoQ.

- BGC (mainly BGCD, but also BGCO and GFSO) was next with a combined 24.6 percent share — down from 28.7 percent YoY, but up from 15.8 percent QoQ.

- Tradition (mainly TSEF, but also TCDS) had a combined 16.7 percent share — down from 18.6 percent YoY, but up from 17.1 percent QoQ.

Cross-currency basis swaps D2D platform market shares were relatively stable in the period.

Summary of market shares

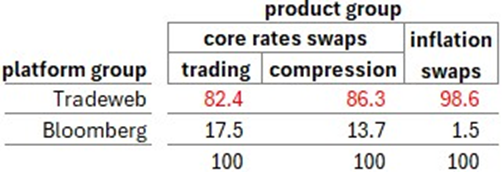

Tradeweb led all three September 2025 D2C platform product-group volumes – as highlighted in red in Table 2.

Table 2: September 2025 D2C platform shares of each product-group (notional percentage). Source: SDRView.

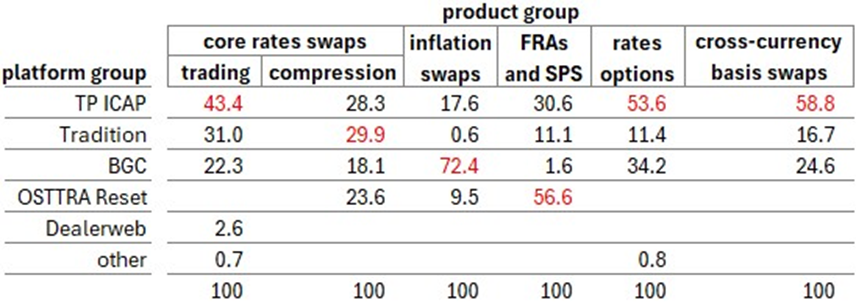

TP ICAP led three D2C platform product-group volumes in September 2025, with Tradition, BGC, and OSTTRA Reset leading one each led— as highlighted in red in Table 3.

Table 3: September 2025 D2D platform shares of each product-group (notional percentage). Source: SDRView.

We used ten charts and three tables to cover SDR-reported D2D or D2C on-platform IRD products with volumes above $250 billion.

You can find a lot more data in SDRView. Click the link to view a summary of the range available.

Contact us if you are interested in a subscription.