The final no-action relief of SEF packages is due to expire November 15, 2014. Many folks have turned to us asking if this will be something that significantly impacts the amount of trades being dealt On-SEF.

BIT OF HISTORY

Back when the no-action relief was first given in May, the November 15 date was by far the longest relief given. Other packages were given a matter of weeks to months before they became MAT, but Invoice Spreads were deliberately given a seemingly long 6 months. Why such a delay for these trades?

I had appreciated that because we’re talking about packages from two separate markets (OTC swap packaged with Listed Futures), that it could be quite complex. Since then, I’ve also been hearing that it’s simply not possible under current laws. But before I try wrapping my head around all of that, I wanted to first understand these products better, and assess just how many of these packages we can see.

THE BASICS OF INVOICE SWAPS

Fundamentally, invoice swaps are a flavor of spread trades, whereby the investor is taking a view on the spread between US government debt and a similarly dated OTC interest rate swap. Essentially a play on the riskiness of the US government vs that of banks.

There are a few manifestations of playing this spread, be it:

- Spread-over-treasuries. Cash bond vs spot starting, standard tenor, OTC swap, which have been MAT’d in June. This is the garden variety for the inter-dealer market.

- Matched maturity cash bonds vs swaps. A variation of the above but where the swaps maturity date matches that of the treasury. The start dates can be either spot or IMM. This is the garden variety for hedge funds.

- Invoice spreads. OTC swap with effective date matching the delivery date of a CME bond future, and a maturity date matching that of the future’s CTD bond.

Liquidity and cost-effectiveness would seem to determine which choice the investor takes. For example, ERIS offers what I would presume to be a very cost effective play on invoice spreads whereby both legs are futures (a CME bond future with an Eris Flex swap future).

SOME DATA

So how big is this market? I pulled the August 2014 data for USD Fixed/Float swaps from SDRView, for which there were a total of 25,871 matching swap trades reported. That’s the entire USD market in the month.

BRIEF DIVERSION

Peter Madigan of Risk Magazine published an article this past week claiming that ISDA is not finding the gurth of forward starting swaps that we’ve reported on a couple occasions. The facts are still there in the August numbers I pulled. 33% of these 25,000+ trades are not a MAT’able start, and when looking at what’s traded Off-SEF, that number is 71%. I’ll also repeat what I said in my detailed post on this topic: this scale of forward starting swap behavior existed before SEF’s started.

BACK TO DATA

From the universe of 25,871 trades in August, I have first pulled out the 3,652 trades that are “Previous” starting, as these can generally be assessed to be from compression or similar process.

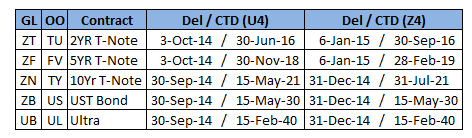

I then looked for swaps matching the following dates, expressed as “Effective Date / Maturity Date” which would match the Futures delivery date and underlying CTD maturity date:

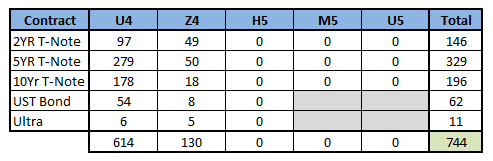

Out of the 22,219 trades in the analysis, I found 744 hits, or just over 3% of the trades done in August. The vast majority of these trades are in the first futures contract (614 trades), and nearly half of them against the 5Yr T-Note Future. I was not able to find any for the 3rd, 4th, or 5th futures contract. Note that the Treasury Bond and Ultra bond only go out to 3 contracts:

Interesting to note that of these 744 trades, 163 of them were flagged as blocks.

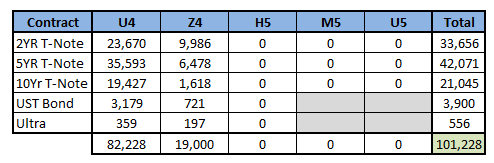

Finally, in Notional terms:

538

So will these be SEF-tradeable in November? The confusion seems to revolve around CME rule 538.

When a futures/OTC package is traded, it is done away from the exchange. This requires an “EFR” (I liken to an EFP) to get the futures registered at CME. That all works. However the new CME rule 538 says you can not do an EFR if it is a futures trade that was executed with a SEF-eligible swap.

Therein lies the rub. Dodd-Frank is saying you have to execute the OTC leg with the future. CME is saying you can’t register a future that was executed with an OTC leg.

Rule 538 went into effect in August. Prior to this, SEF’s like Tradition actually listed such OTC/Futures packages on their SEF. Alas they can no longer do that.

I presume the only reason this has not been a larger issue to date is that, except in extremely rare cases, the underlying swap for invoice spreads are not MAT, and hence not required to be executed on SEF.

SUMMARY

- Invoice spreads are one way to express views on the spread between US debt and swaps

- Invoice spreads are a significant portion of the market (3%+)

- What is going to happen come November? Particularly if more products become MAT’d, this could really be an issue.

Hi Tod,

Thanks very much for an engaging post! Regarding 538, do you think the FAQ section of the CME guidance addresses this issue? I think the CME is going to allow ‘transitory EFR’s’ in the case of swaps, but I may be misunderstanding the interpretation on transitory efrp’s here.

Answer to Q3:

Where the related position component of an EFRP is an instrument defined as a swap pursuant to federal regulations, or is another OTC derivative transaction, the transaction must be submitted as an EFR or an EOO transaction type, as applicable, and must be reported as required under Parts 43 and 45 of Commodity Futures Trading Commission Regulations.

Q14: Can a swap be negotiated to settle via an EFR?

A14: Parties to a swap may agree to settle the swap via an EFR provided that the determination of the settlement value of the swap (floating price) is subject to market risk that is material in the context of the transaction. For example, parties may negotiate a swap to settle via EFR on a specific date in the future at the futures settlement price or the average settlement price over a prescribed time period.

Q15: Can an EFRP incorporate multiple legs on the Exchange component of the transaction or incorporate multiple legs on the related position component of the EFRP?

A15: An EFRP may incorporate multiple Exchange components provided that all of the Exchange components have the same market bias (long or short). For example, a Eurodollar futures strip versus equivalent exposure in an interest rate swap may be executed as an EFR.

EFRP transactions incorporating multiple Exchange components with different market biases (long and short) are permitted only where the Exchange components are legs of a recognized intercommodity spread involving a product and its by-products. For example, a party may execute an EFR buying crude oil futures and selling gasoline and heating oil futures versus a crack spread swap, or an EFR buying soybean futures and selling soybean oil and soybean meal futures versus a soybean crush swap.

An EFRP may incorporate multiple related position components provided that the net exposure of the related position components is approximately equivalent to the quantity of futures exchanged or, in the case of an EOO, the net delta-adjusted quantity of the OTC option components is approximately equivalent to the delta-adjusted quantity of the Exchange-listed option.

Thanks Jon. Your comment spurred me to read some of the comments from late 2013 here as well as the May advisory notice here.

What firms took offense to is addressed further down in Answer 3:

A swap that is traded on or subject to the rules of a designated contract market (“DCM”) or a

swap execution facility (“SEF”) is ineligible to be the related position component of an EFR or

EOO transaction executed pursuant to Rule 538.

The above-referenced exclusion does not apply to swaps that are bilaterally negotiated and

submitted for clearing-only to a DCO provided such swaps have a reasonable degree of

correlation to the underlying CME Group Exchange product.

If I read that right, CLOB-executed SEF/DCM swaps cannot be done as EFR. Which is fine because not much is clob. However I would also infer that RFQ-arranged SEF trades are not bilaterally negotiated, and hence not eligible for EFR.

Which would leave non-MAT, but clearing eligible swaps that are bilaterally negotiated to be done as EFR.

Alas I am not an expert on this, so would be interested in any thoughts you or others have.

Tod-

I would tend to agree with your interpretation and the analysis of Citadel & TW.. Thanks for providing. TBH I am very surprised the CME did not remove this requirement after the comment period. Their prohibition encourages more off-SEF activity, increasing the opacity of the swaps market. Additionally, it seems to increase the odds that a party will struggle to hedge their future transaction if they wait until the swap is no longer a ‘transitory efr’. Have you noticed any drop off in volume for Invoice Spreads since Aug 4th? Perhaps there will be no impact until November 16th area when these packages are MAT… Please let me know your thoughts.. Really appreciate the thread

I think if you are CME, you’d want to limit the amount of futures being dealt away from the exchange. Would have to think that is primary concern for them. Regarding August activity, I pulled data for July and oddly August seems to be an uptick. I don’t have trends from previous months but the data is there to do the research. I have also received some private comments that many invoice spreads are done without perfectly matching dates. My research here required final delivery and CTD dates to exactly match the swap dates, so my 3%+ is seemingly the floor on the market size.