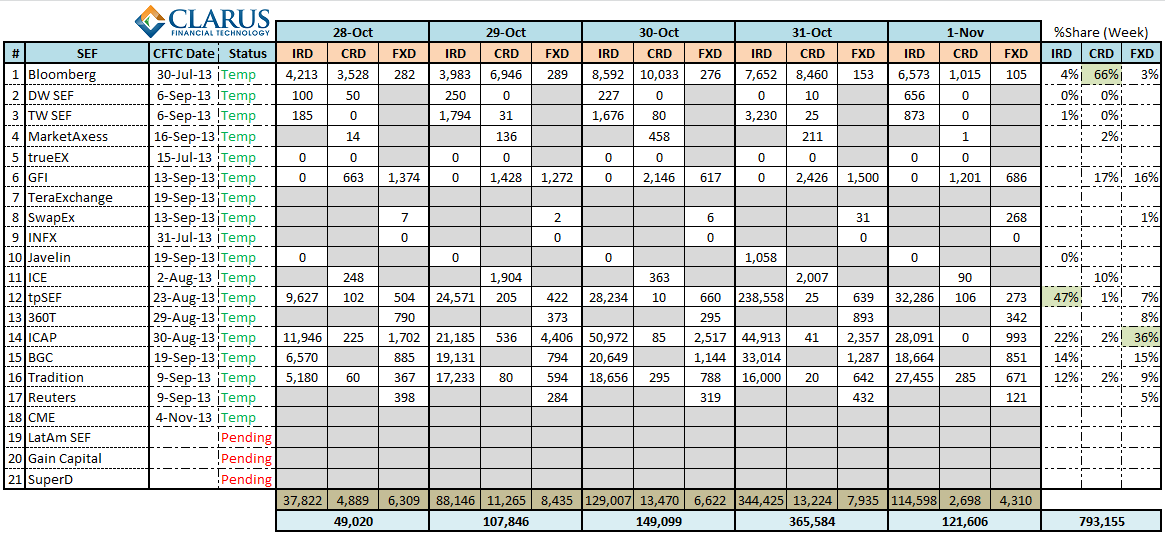

The fifth week of SEF activity is completed. Once again we have collated the various SEF reports. Here is this weeks summary (click on the picture for a larger version) :

THE DATA

BIG NUMBERS

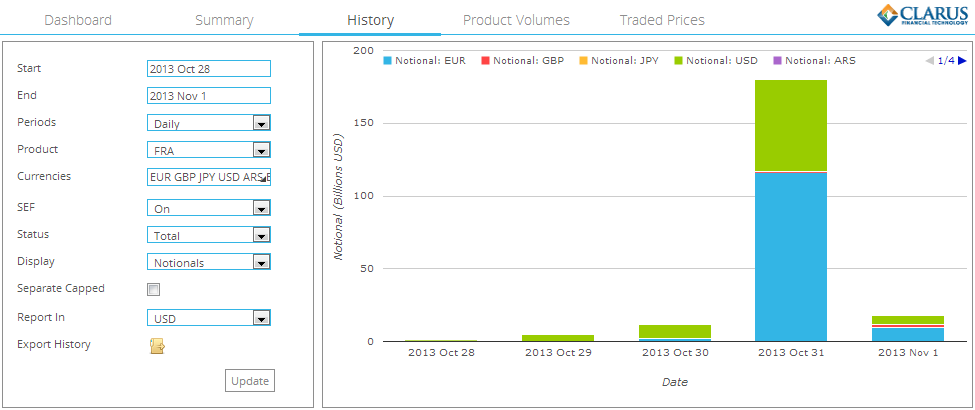

As I mentioned in last weeks report, these numbers seemed to be skewed by FRA’s, particularly the TPMatch and ICAP Reset activity. I decided to have a closer look at this. I began by using the SDRView history tab to quickly discern the FRA volumes for each day in the week, as officially reported to the SDR. You can see the large jump on Thursday.

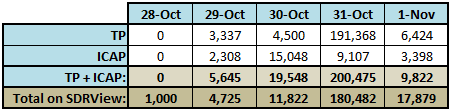

I then made a simple table to compare this to the SEF reported data. The first two rows show FRA volumes, as reported by the particular SEF (TP & ICAP). Next is simply the sum of these reported values, and the final row is the data collected from SDRView:

The bottom two rows should match, with some caveats:

- I am only looking at TP & ICAP SEF data from the reports. The SDRView data looks at all SEF activity, however the vast majority is these two SEF’s

- While SDRView has execution dates and times for every trade, there is no telling the cutoff date/time for SEF reported data (note my best practice recommendations on this topic here).

- While SDRView is easy to interpret, there may be some misinterpretation of the SEF data from the various formats they supply.

- Cap sizes in the SDR may understate the volume, however this is only the case for exceptionally large trades (FRA’s have a cap of 2.1bn USD)

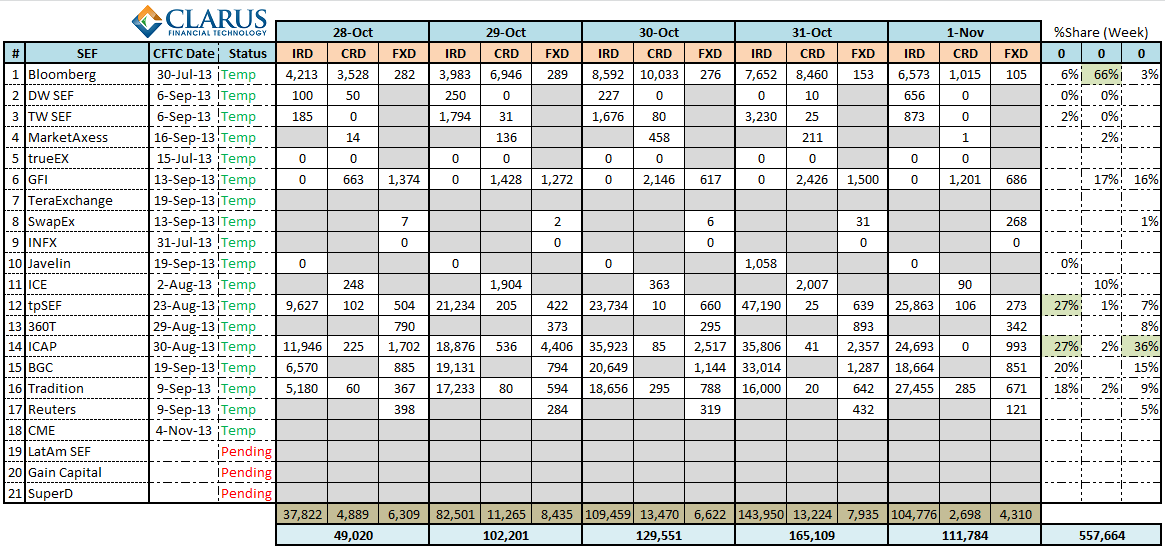

We are able to conclude that the SDR data does corroborate the SEF activity. I thought it worthwhile to also publish an updated table, ex-FRA activity, below:

D2 Who?

I’ve had a few comments over the past weeks from people wanting to understand the split between dealer-to-dealer platforms vs dealer-to-client platforms. I’ve assumed that Dealerweb, ICE, and the IDB’s are predominantly D2D business, and everything else is D2C. I’d welcome comments on whether this is a safe assumption. I (like many) believe that this separation will blur as the new market environment takes hold.

BUSY WEEK

Please feel free to give us your comments below, or if you happen to be attending the FIA event in Chicago, you can find me and give them to me in person!

UPDATE

This weekly issue of SEF updates is not the most current. To see all SEF posts, including the most recent, please click through to the SEF Category.

Great report and the removal of the FRA compression runs makes perfect sense. I feel though another adjustment that needs to be made to the notional numbers is duration equalisation. ie 1bn 2 year is equivalent to 400m 10 year but the way its reported as just notional does not reflect this. Accordingly numbers are heavily skewed to brokers who do more business at the short end of the USD mkt and therefore somewhat misleading.

Indeed that could be an interesting analysis. Send us your contact information (your comment was sent as anonymous) and we might be able to come up with something.