With inflation front and centre of everyone’s mind, let’s test a simple hypothesis. If inflation expectations are becoming entrenched – i.e. people expect inflation to be elevated for a longer period – is there evidence of this in trading activity?

What evidence might we see? There are two potential signals:

- More trading activity in Inflation Swaps.

- The Weighted Average Life of activity in Inflation Swaps increases, as market participants lengthen the time horizon over which inflation is hedged.

And just in case we have any readers who are not aware of the inflationary backdrop to this blog, I recommend checking out the BIS highlights from earlier this week:

If you need any reminding about Inflation Swaps more generally, please check out some of our recent posts on the subject:

- G3 INFLATION SWAP VOLUMES ARE ON THE UP

- BIG VOLUMES IN CREDIT AND INFLATION PLUS EUROPEAN EQUIVALENCE

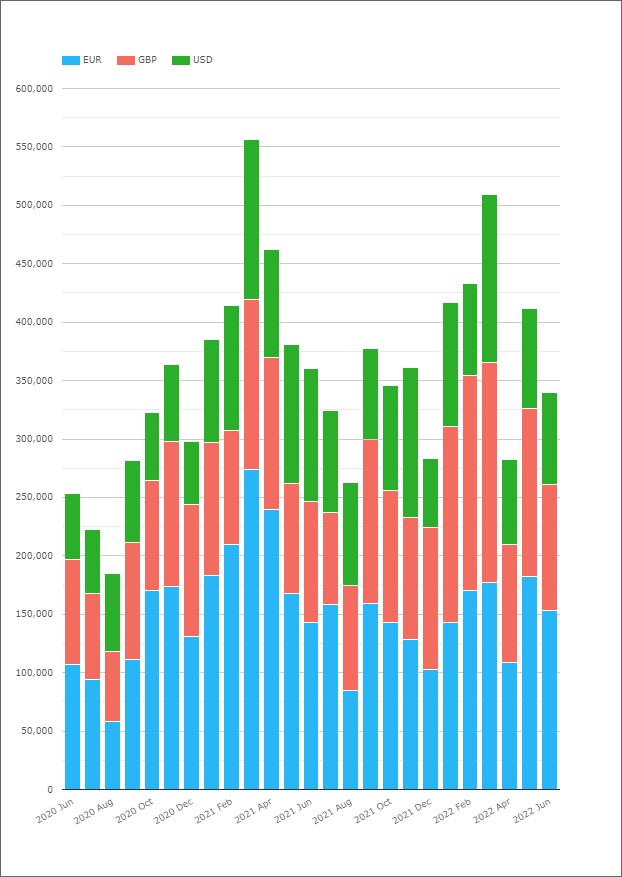

Monthly Cleared Inflation Swap Volumes

Monthly volumes of cleared inflation swaps topped $500 Billion for the first time in March 2021. That was basically double the monthly volumes that traded in 2020. Some would argue that the market has been all over this inflation story for quite some time!

Cleared inflation volumes have not quite reached those giddy heights again. Looking at cleared volumes for the past 2 years from CCPView does show very healthy volumes however:

Showing;

- Cleared volumes in EUR, GBP and USD inflation swaps per month. Volumes are shown in USD notional equivalents.

- For context, February 2020 was the first month that global cleared volumes had surpassed $300bn.

- Now, the 2022 monthly average volume is $400bn (with 4 more trading days left in June 2022!).

- And 2022 can add another $0.5Trn month to the record books, with $510bn notional traded in March 2022, within 9% of the all time record monthly volume traded in March 2021.

- The volumes in H1 2022 (so far) are some 22% higher than the volumes in H2 2021. Is H1 seasonally a larger volume period? Let us know in the comments below.

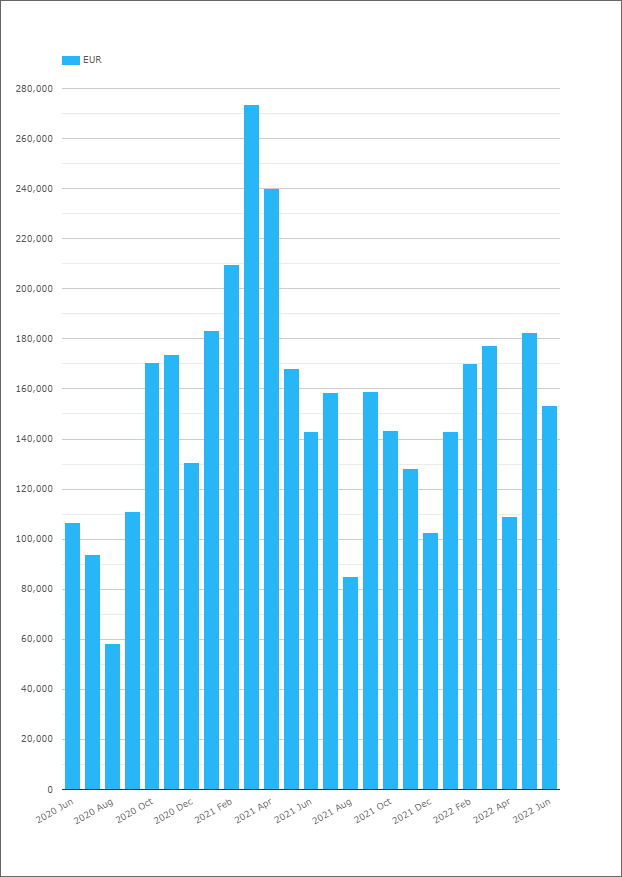

EUR Inflation Swap Clearing

Looking at each currency in turn, the EUR Inflation swaps market is an interesting beast:

As the chart shows:

- The record 3 months in 2021 (Feb-April) really stand out in EUR Inflation activity.

- These three months are the only months on record when volumes were larger than $200bn+ notional equivalents.

- Those 3 months drove average monthly activity in EUR inflation swaps to $166bn in 2021, although this was somewhat lower in H2 2021 at $130bn.

- Average monthly volumes so far in 2022 sit at $150bn.

- In 2022, cleared EUR Inflation Volumes tend to account for about 40% of total global volumes. It is still the largest Inflation market by notional volume.

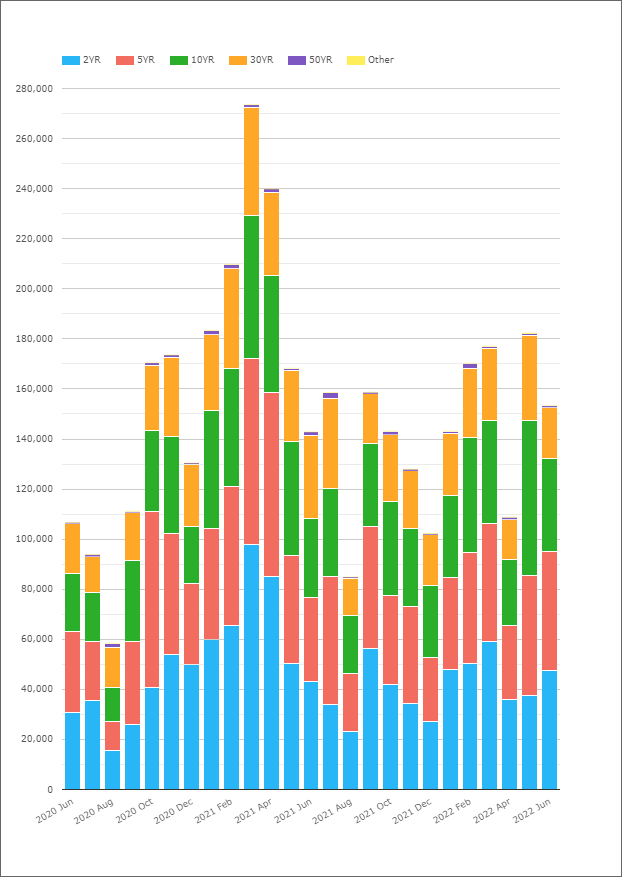

CCPView also includes a break-down of tenors traded.

Showing;

- May 2022 saw large volumes in EUR inflation swaps. Will June 2022 beat it?

- In particular, May 2022 saw the largest amount of 10Y EUR swaps ever cleared. It is the only time in our data history that more than $60bn equivalent of 10Y EUR inflation swaps have been cleared in a single month.

- That is about 20% larger than during the record months back in 2021.

- Is that a sign that the average tenor of inflation hedges is extending?

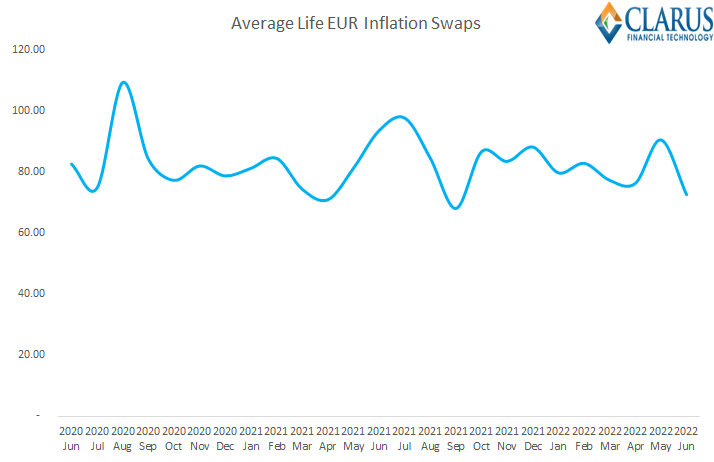

We can plot the weighted average life of EUR Inflation swap trading using our tenor data:

Showing;

- Weighted average life of cleared EUR Inflation Swaps. This is calculated as (Tenor in Months * Notional) / Total notional. This is very similar to some of the methodology we use in the RFR Adoption Indicator.

- The longest weighted average life we have seen recently was in one of the lowest volume months – August 2020 – at 110 months (9 years).

- Aside from that, June and July 2021 saw an average life longer than 7.5 years (i.e. quite a bit shorter than August 2020), and May 2022 comes in as the 4th longest tenor, at 7.55 years, in our time-series.

Overall, I’m not convinced that there is a strong signal that trades are getting longer in EUR.

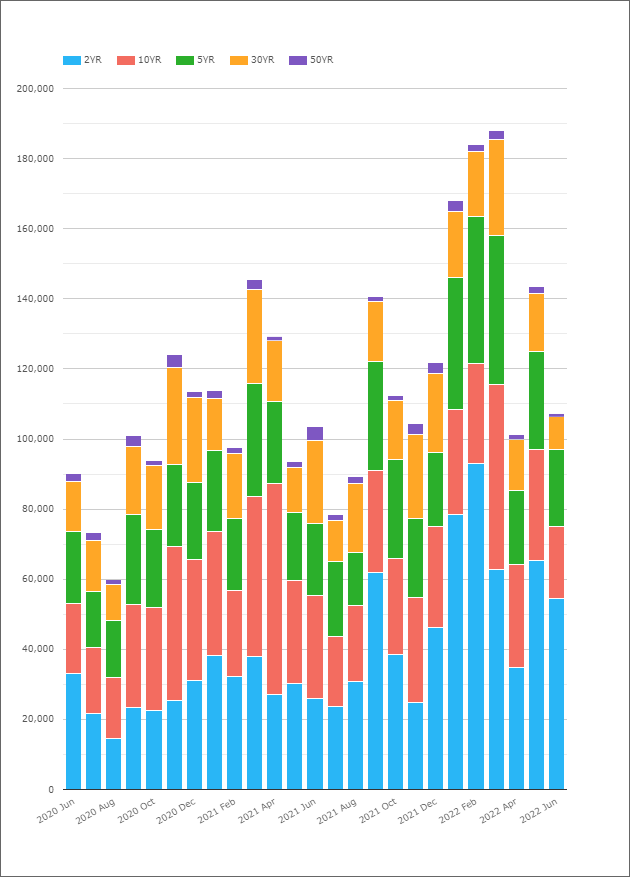

GBP Inflation Swap Clearing

Turning our attention to GBP markets;

Showing;

- Cleared volumes by tenor in GBP Inflation swaps. All volumes are at LCH SwapClear.

- Volumes have really grown in 2022 – by 34% compared to last year.

- March 2022 was an all time record month, with over $188bn equivalent traded.

- The three largest volume months all occurred in Q1 2022 in fact!

- And May 2022 was the fifth largest of all time.

- GBP Inflation trading is extremely active right now.

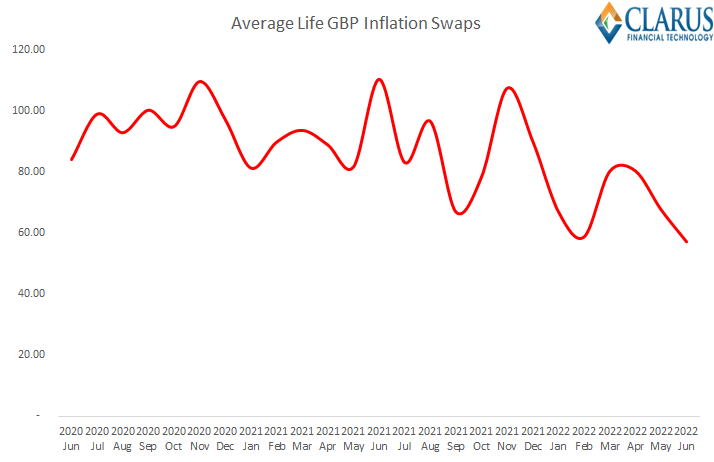

There is therefore one sign that inflation expectations are becoming entrenched in GBP markets – there is much more activity than we have ever seen before. Are the trades also getting longer?

Well, that chart tells a story!

- Weighted average life of cleared GBP Inflation Swaps.

- June 2021 saw the longest average activity, at 9.2 years.

- In 2022, that same average life has been more like 5.7 years.

- In fact, there is evidence in 2022 that the weighted average life of activity is getting much shorter.

- This might help explain why we see higher notional amounts trading. It is a similar amount of risk, but moved “up” the curve to shorter maturities.

- For example, May 2022 saw the 3rd highest volumes of 2Y and shorter tenors traded.

- One for our DV01 calculations to verify.

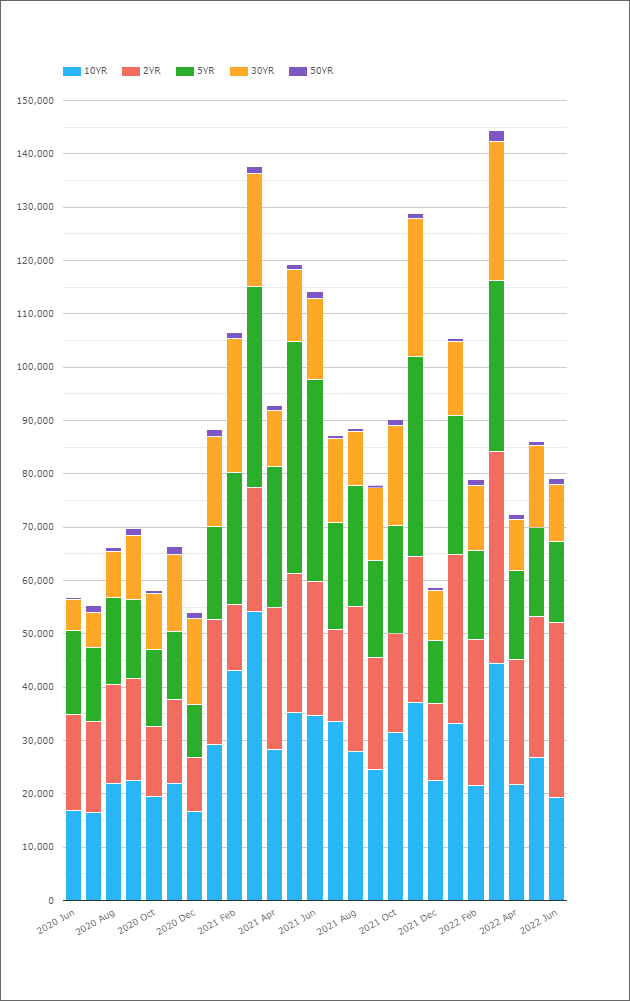

USD Inflation Swap Clearing

Finally, are inflation expectations becoming entrenched in US markets?

Showing;

- Some large volumes in inflation trading in 2022.

- March 2022 saw all time records in cleared USD inflation swaps, topping $140bn for the first time.

- The monthly average volume in 2022, however, is almost identical to the average during 2021, at around $95bn per month.

- Monthly volumes are pretty volatile.

- With 4 trading days still to go, June 2022 has already seen the second largest amount of notional traded in tenors of 2Y and less. This was only beaten by March 2022.

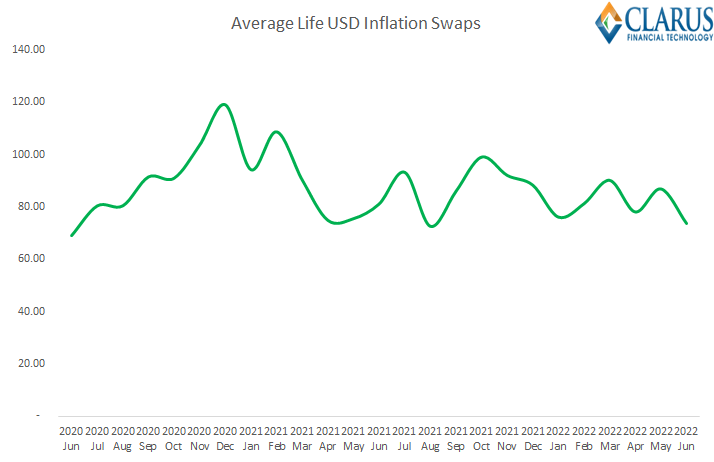

Given that last data point, it is perhaps no surprise to see the following chart for Weighted Average Life in USD Inflation Swaps:

- Weighted average life of cleared USD Inflation Swaps.

- December 2020 saw the longest average activity, at nearly 10 years.

- In 2022, that same average life has been more like 6.8 years, compared to 7.5 years in 2021.

- The chart suggests that trades have been somewhat shorter this year.

In Summary

- We look for signals that inflation expectations are becoming entrenched.

- We suggest that elevated trading volumes and longer average maturities point to entrenched inflation expectations.

- The data shows that inflation swap activity is 22% higher this year than last.

- This is particularly the case in GBP markets (+34%).

- However, there is no evidence that the average life of trades is increasing in these two markets.

- EUR inflation swaps did see a record amount of 10Y swaps trading in May 2022, but there is no clear sign that this is part of a general trend.