Monthly volumes of cleared inflation swaps topped $500 Billion for the first time in March 2021. That is basically double the monthly volumes that we were seeing as recently as a year ago.

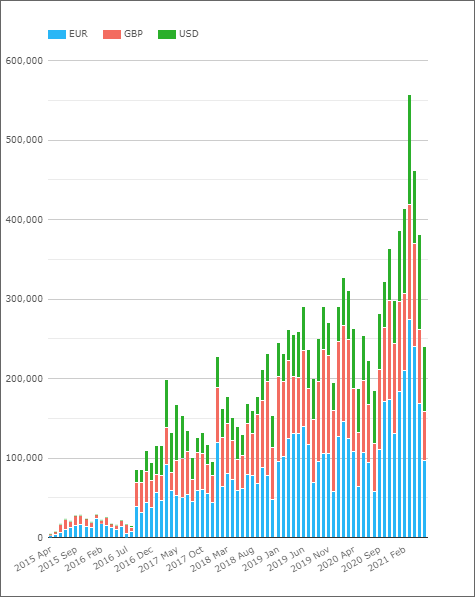

This blog will take a look at the volume data available to us. It serves as a great reminder of just how much history we have in our data products at Clarus. Cleared volumes in Inflation swaps for the past 6 years from CCPView:

Showing;

- Cleared volumes in EUR, GBP and USD inflation swaps per month since 2015. Volumes are shown in USD notional equivalents.

- February 2020 was the first month that global cleared volumes had surpassed $300bn.

- Since then, we have had 8 months over $300bn.

- This includes two months over $400bn.

- And the huge volumes in March 2021, which saw $556bn of inflation swaps cleared. That is a stand-out month by anyone’s standards.

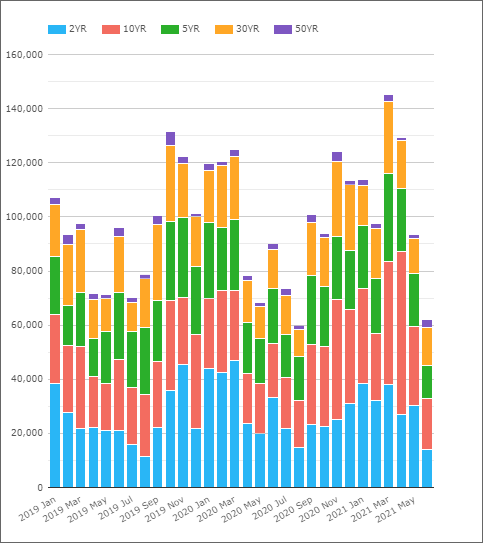

EUR Inflation Swap Clearing

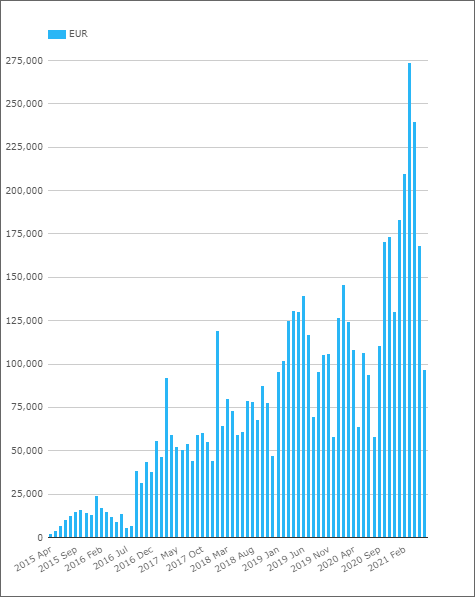

Looking at each currency in turn, I was surprised to learn that it is the EUR Inflation swaps market that is the largest market:

As the chart shows:

- The high volume months are characterised by spikes in EUR inflation volumes, such as March 2021.

- These months tend to see EUR accounting for over 50% of total cleared inflation swap volumes.

- Nearly $275bn equivalent traded in EUR inflation swaps during March 2021.

- The four record volume months were all at the beginning of 2021 from January until April. Something really stirred up EUR inflation trading.

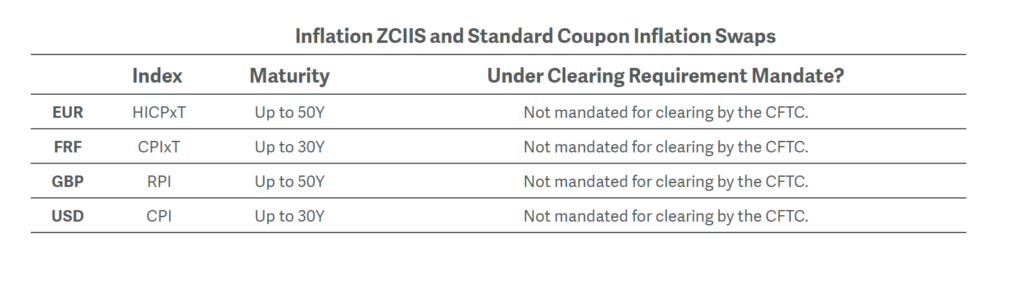

As the LCH website highlights, none of these products are subject to clearing mandates but there are two different EUR inflation indices that are cleared:

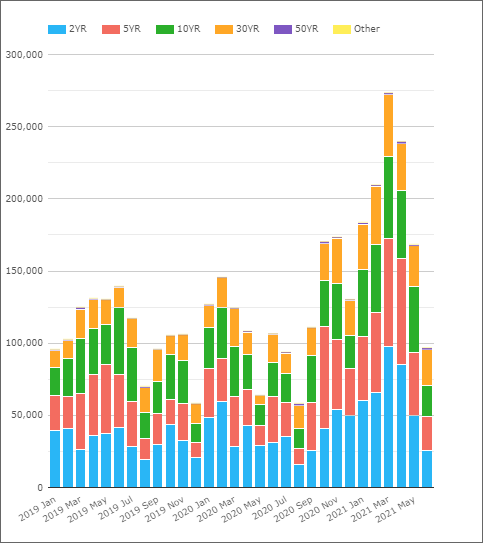

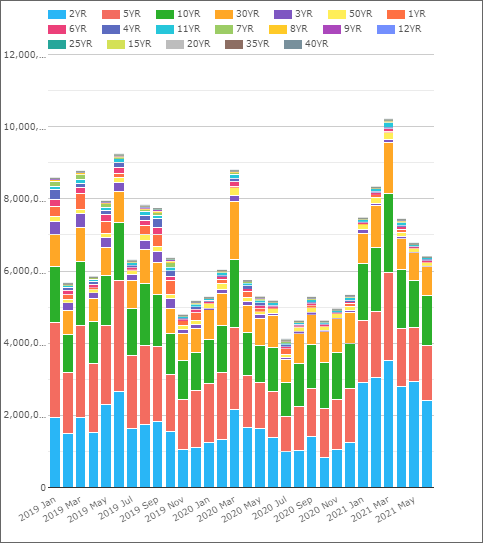

CCPView also includes a break-down of tenors traded.

The split of volumes by tenor is pretty stable over the past couple of years:

- 30% in 2 years.

- 25% in 5 years.

- 25% in 10 years.

- 15% in 30 years.

- Not much in 50 years.

There doesn’t seem to have been a particular maturity that saw a spike in volumes in March 2021. It was broad-based activity that caused the large volumes across all tenors.

And Brexit?

Amir’s blog on Inflation Swaps from way back in 2015 here reminded me that the interdealer market for EUR Inflation swaps probably saw some Brexit impacts. Indeed, we have seen an increase in EUR Inflation Swaps traded on SEF during 2021:

However, the increases in volumes traded on-SEF have not been anywhere near the experience we saw in vanilla EUR IRS. This likely speaks to the fact that EUR Inflation Swaps are not subjected to a Trading Obligation (“DTO”) and therefore do not have to execute on venue. It is also notable that:

- The increase in volumes has mainly been seen on a Dealer to Client SEF, Tradeweb. This is different to what we have seen in vanilla IRS, where it has been the interdealer SEFs seeing the increase in volumes.

- NEX has now started passing EUR inflation swaps across its SEF. I guess these are regular compression-type exercises?

- The largest on-SEF volumes were actually seen last month, not in March.

- SEF volumes overall are small and vary a lot! Of the $275bn that traded in March, just 3.7% traded on-SEF.

- Why are there no EUR Inflation swap volumes on the Bloomberg SEF? Weird.

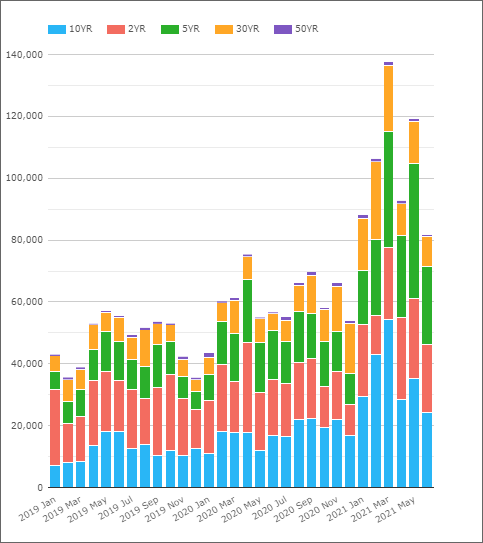

GBP Inflation Swap Clearing

Turning our attention to GBP markets;

Showing;

- Cleared volumes by tenor in GBP Inflation swaps. All volumes are at LCH SwapClear.

- Volumes have been more consistent in this market than in EUR.

- March 2021 was also a record month.

- Roughly speaking, GBP volumes are half of EUR volumes.

- The maturity split is slightly different to EUR, with less short-end volumes and more 50Y volumes.

- 2Y see about 25% of volumes, 5Y accounts for 25%, 10Y another 25%, whilst 30Y accounts for 20% and 50Y for 5% of volumes.

USD Inflation Swap Clearing

Finally, on our whistle-stop tour of Inflation swap volumes, we look at US markets:

Showing;

- An evolution of volumes more similar to EUR markets, with volumes showing incredible growth in Q1 2021.

- Note that we did not see a huge volume spike in inflation swaps in March 2020, where-as this was the over-riding feature of vanilla IRS markets in the middle of the market turmoil.

- However, as we noted at the time, the large sell-off in bond markets back in February and March 2021 really served to increase volumes in vanilla IRS trading, as shown by global cleared volumes below:

- Showing global cleared volumes of vanilla USD IRS for the past couple of years.

- Note that March 2021 was an all-time record month for IRS volumes, surpassing even March 2020. We noted this at the time in our blogs.

Is it therefore possible that inflation swap volumes simply spiked in line with overall Fixed Income activity in March 2021? Did a rising tide “lift all ships” in this case?

If so, it seems very similar to Swaptions activity to me. However, for swaptions we could clearly point the finger at convexity hedging as rates increased (a lot). What is the cause in Inflation swaps for volumes to increase as rates rise?

It is worth bearing in mind that as well as large increases in reported/realised inflation we saw large increases in 5y5y inflation expectations in both the US and Europe at the beginning of 2021 (admittedly from all time lows due to the pandemic). Is it this volatility in the underlying that has driven volumes?

Uncleared Markets

Of course, there remains a large and active market in uncleared inflation swaps as well. However, transparency is severely lacking in this area of the market, therefore the analysis we can perform is sadly limited.

In Summary

- We have seen all time record volumes in Cleared Inflation Swap volumes.

- These occurred specifically in March 2021 where EUR, GBP and USD Inflation Swap volumes all peaked.

- It is notable that we did not see the same spikes in Inflation Swap volumes back in March 2020 when inflation expectations cratered to all-time lows.

- However, as inflation expectations have increased sharply since the turn of the year, volumes have rocketed higher.

- Monthly cleared volumes in inflation swaps can now top $500bn in a single month.