The Basel III Leverage Ratio, often referred to as the Supplementary Leverage Ratio (SLR), is one of the important new metrics introduced as a response to the Financial Crisis of 2007-08 and one which continues to receive a lot of press coverage and discussion.

In this article I will provide an overview and some of the detail that is most relevant to cleared derivatives.

Background

In January 2014, the Basel Committee on Banking Supervision (BCBS) published, “Basel III leverage ratio framework and disclosure requirements”, (see bcbs270.pdf) and in April 2016 a Consultative document “Revisions to the Basel III leverage ratio framework”, (see d365.pdf).

These documents state that an underlying cause of the global financial crisis was the build-up of excessive on- and off-balance sheet leverage in banks which apparently still maintained strong risk-based capital ratios.

The introduction of a simple, transparent, non-risk-based leverage ratio is designed to act as a credible supplementary measure to the risk-based capital requirements.

Public disclosure requirements in a prescribed format started in Jan 2015 (quarterly), to allow for calibration and comparison and a smooth transition by banks prior to regulatory implementation in 2018/19.

Leverage Ratio

The definition in the BIS document is:

with a 3% minimum requirement, though subsequently some jurisdictions (e.g. US) have specified higher ratios of 5% or 6% for global systemically important banks.

The Capital measure is Tier 1 Capital, which is mostly Common Equity and some additional Tier 1 Capital e.g. Preferred Stock.

The Exposure measure is the sum of on-balance sheet exposures, derivatives exposures, securities finance transaction exposures and off-balance sheet items. (In later sections I will focus only/mostly on the derivatives exposures as most relevant to us).

Importantly unlike Capital Ratios which are of the form Capital divided by Risk Weighted Assets (RWAs), the Leverage Ratio intentionally does not distinguish between safer or riskier assets; meaning that for SLR a bank must hold the same minimum amount of capital against low risk assets (e.g. US Treasuries) as higher risk assets (e.g. Equities).

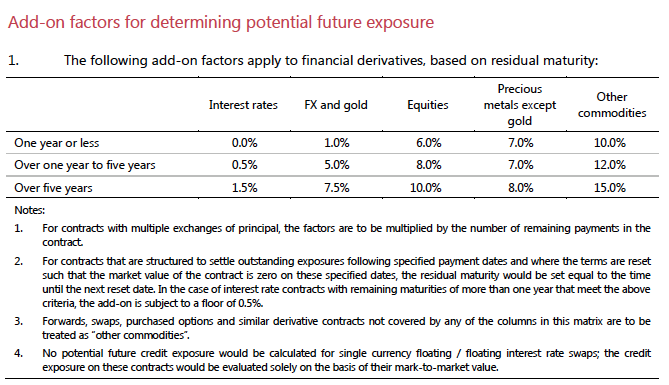

Derivatives Exposures

The determination of derivatives exposure in the January 2014 BIS paper was based largely on the Current Exposure Method (CEM), which does not differentiate between margined and un-margined trades.

The table of Add-on factors for PFE given in this paper, gives a sense of which products are hit particularly hard by SLR e.g. Cross Currency Swaps.

In April 2016 consultation paper BIS proposed to implement a modified version of the SA-CCR, which is a great improvement in methodology over CEM for margined trades as and when firms move to SA-CCR (2018/19).

The modification to SA-CCR mean that:

- the Replacement Cost (RC) component will be modified to restrict the recognition of collateral by allowing only eligible cash variation margin exchanged under specified conditions, which include same currency as the settlement currency of the derivative contract, daily margining, full amount of VM, single master agreement to cover the derivative and the VM.

- the PFE add-on component will be adjusted by setting the PFE multiplier to 1 (one), thereby not recognising any collateral posted by the counterparty (or any negative net market value of the derivative position). However, in line with the SA-CCR framework, the effect of margining would continue to be reflected in the potential shorter time horizon or margin period of risk (MPOR), ranging between 5 and 20 days, depending on whether the transaction is margined and centrally cleared as well as on the size of the netting set.

This last point has been the subject of much industry lobbying as it means that Clearing Members that offer Client Clearing and collect Initial Margin from clients cannot use that to offset the PFE add-on component, which does not make sense (at least to me).

For more on this and other comments, from the press, see Risk.Net, FT, Reuters, from industry bodies, see BBA, ISDA and for futures see ABN.

Use of Balance Sheet

Derivatives trading is subject to minimum regulatory capital requirements in that firms are required to maintain Capital Ratios and derivatives exposure contributes to Risk Weighted Assets (RWAs) for Credit Risk, Market Risk and Operational Risk.

Generally this has been the binding balance sheet constraint in large derivatives books.

However with the supplementary leverage ratio (SLR), there is now a new constraint.

Whether RWA or SLR is the binding constraint for a firm depends on their business mix and balance sheet.

In general a universal bank with relatively higher risk assets is more likely to be bound by the RWA requirements, while custody banks, trust banks or broker-dealers are more likely to be bound by SLR, as they have a relatively higher portion of low risk assets.

In a Sep 2013 paper by industry associations, GFMA et al (see here) more than half the banks surveyed believed that SLR was the binding constraint for them.

Either way pressures on balance sheets and ratios, means that banks are actively managing both RWA and SLR and in many cases explaining to clearing customers the need to charge for balance sheet and in some cases changing their customer mix (e.g. Deutsche Bank, see here).

SLR Disclosures

Banks have been disclosing their SLR figures in a prescribed format, so lets look at a few of these disclosures.

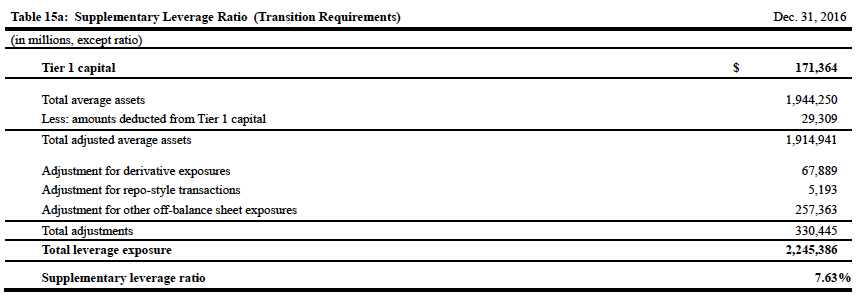

Starting with Wells Fargo & Company for Dec 31, 2016 (from Basel III Pillar 3 Disclosures).

Showing SLR of 7.63% and Tier 1 Capital of $171 billion.

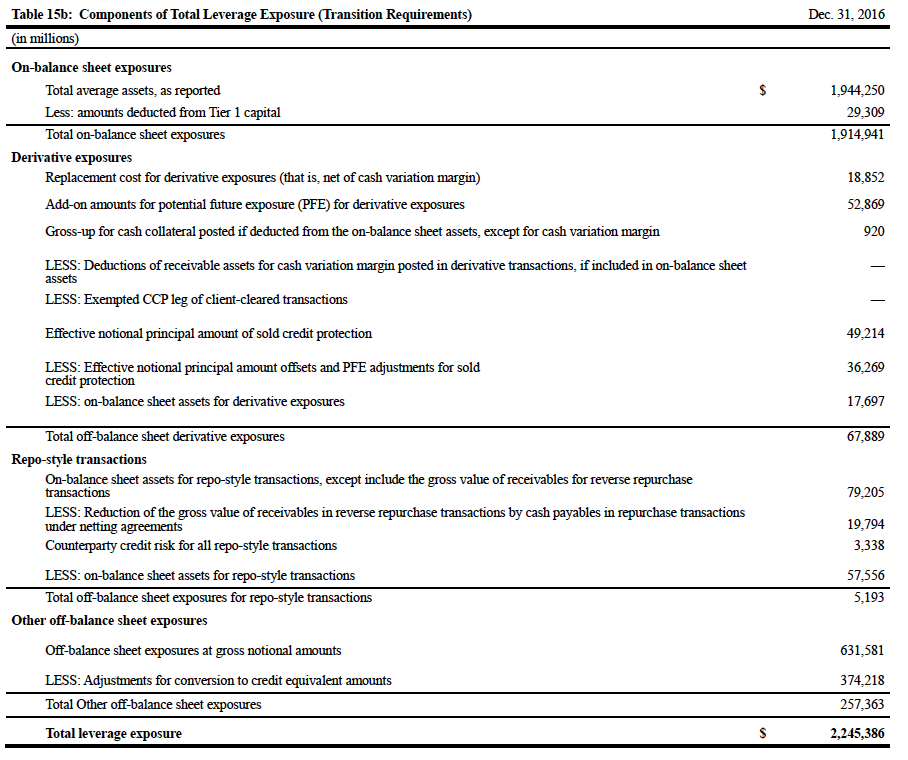

Next the component breakdown.

Showing:

- On-balance sheet exposures as $1.9 trillion

- Derivatives exposures as $68 billion

- with RC of $19 billion, PFE $53 billion

- and adjustments for Credit derivatives

- Securities finance/Repo exposures of $5 billion

- Other off-balance sheet exposures of $257 billion

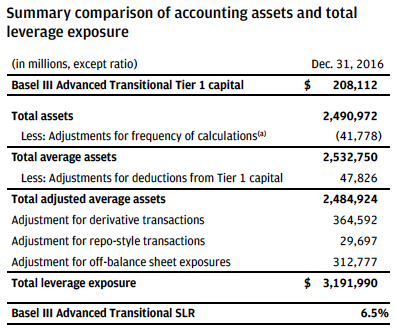

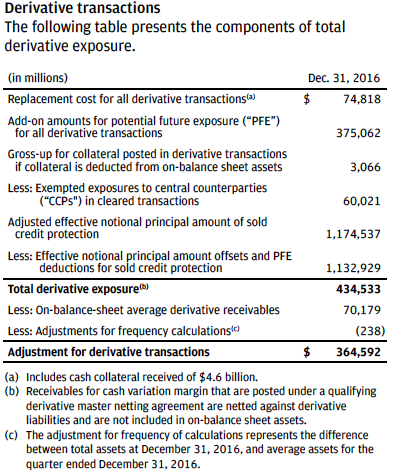

Next JP Morgan Chase & Co for Dec 31, 2016 (from Basel III Pillar 3 Disclosures).

Showing SLR of 6.5% and Tier 1 Capital of $208 billion.

Next the component breakdown table, just for derivatives.

Showing:

- Derivatives exposures as 364 billion

- RC of $75 billion

- PFE of $375 billion

- Less exempted exposures to CCPs of $60 billion

- Adjustments for Credit derivatives

Interesting numbers indeed.

There are a lot more firms to look at and quarter on quarter tends to observe.

I intend to do that in a future article.