A while back, we began noticing a lot of “back start” swaps on the SDR ticker in SDRView. Reconciling this with some particularly large days on SEF, we determined that many of these were “compression” runs. Amir wrote a blog about this back in July here.

Fast forward a couple months and I’ve become aware of various post-trade services that TrueEx is marketing to the client community, and it has made me realize there is potentially a lot more to SEF’s than just a place to go execute a swap.

WHAT THE DCO’s LET YOU DO

Before we look at what SEF’s are offering, it is wise to understand what the DCO’s themselves are offering, as some of the SEF services are really just tools to facilitate services offered by the DCOs.

- Compression. Cleared trades with matching fixed rates and payment dates can be compressed into a single line item.

- Coupon Blending. Loosens the requirements of basic compression to allow for trades with any fixed rates to be processed. The DCO will terminate all the trades and replace them with two trades:

- Fixed/Float swap that has a weighted notional blended rate

- Fixed/Float, zero coupon swap, with an adjusted notional to balance the projected floating flows.

- Standby Clearing. A service to clients to clear a single trade and later be allocated.

Coupon blending would seem to be particularly helpful for IMM (but not MAC) swaps, such that a firm can buy and sell a standard IMM swap 100’s of times over the course of days and weeks at a 100 different rates, and end up with just two line items.

SO WHAT CAN SEF’s DO

So we all know you can execute a trade on a SEF, be it via CLOB or RFQ. But let’s examine at least some of the items in the TrueEx marketing literature:

- PTC

- Bunched Orders

- Coupon Blending

- Trade Porting

- Average Pricing

PTC (Portfolio Termination & Compaction)

TrueEx and Tradeweb offer PTC, and Bloomberg has been vocal about offering this shortly. Idea being that in order for clients to take advantage of the DCO Compression services, the DCO requires NEW trades to be created and cleared to either fully or partially terminate the clients pre-existing trades. As such, clients upload a portfolio to the SEF, and the SEF facilitates the RFQ for offsetting trades.

Bunched Orders

If you rewind to the days before clearing, the typical asset management transaction was typically done as a single trade, and then later on that day, the client would send a spreadsheet to their bank with instructions on how to allocate that trade across the 40 or so separate accounts they were trading for. I recall Markitwire and VCON facilitated this post-trade workflow.

When the days of clearing came in, this had to be re-tooled to expedite the clearing process such that each trade hit their beneficial owner account immediately. What this meant was that trades had to be “pre-allocated” prior to execution so that each trade would be sent for clearing. Worth noting that the master trade seems to get reported to the SDR, but the individual allocated legs are cleared.

Enter now the concept of standby clearing which allows clients to execute the bunched order as a single trade again. For pre-deal credit checking, the client uses an FCM account that has been setup for (presumably) gross credit checking, this is the standby-FCM. The master trade gets cleared and held in this account at the DCO until instructions are received to assign it to the multiple accounts, which could also potentially span multiple FCM’s.

So where are those instructions managed? Well, this is where SEF’s potentially come in. In theory the client can communicate the allocation schedules to their FCM, who can then communicate them to the DCO for each trade. But if you are a client, you probably have multiple FCM’s and each probably ask you to put it into special formats.

I understand that TrueEx, Bloomberg, and Tradeweb each allow clients (and potentially their FCMs) to perform this allocation operation on their SEF, which in turn communicates with the DCO. The TrueEx offering appears to be agnostic to venue, CCP, voice/electronic, etc, so that for example, you could execute on Javelin, Bloomberg, Tradeweb, even ICAP, and allocate on the TrueEx PTS platform. This could be interesting if you believe the story that the IDB’s are behind in the “client-friendly” bells and whistles on their SEFs, and hence clients need a place to do post-trade operations after execution on one of these venues. Of course you’d also have to believe that a client is trading on an IDB SEF!

Coupon Blending

Coupon Blending should hopefully be clear from a DCO perspective. They (the DCO) are the counterparty, so they can do whatever they want to trades as long as the risk and flows are equivalent.

What caught my eye is TrueEx offer “trueBlend” as a one-sided process to reduce line items, along the lines of what the DCO offers. It’s not entirely clear to me how a utility other than a DCO can offer a one-sided coupon blending process, but it seems TrueEx facilitate the STP & reporting of these transactions back into the clients systems.

Trade Porting

Trade Porting also caught my eye. TrueEX market this as a utility to “move existing positions between clearing houses and between clearing firms.”

Back in 2009 when I first began working with clearing houses, we designed a solution for doing just this – taking a cleared leg of a trade and moving it to another clearing house. Logistics are possible, but the fundamental problem is always that the clearing house needs to maintain a zero risk position, so you can’t ever take away a single leg of a trade.

In order to move a trade to another clearing house (without executing more trades) requires de-clearing it. To do this and maintain a zero risk position at the CCP, you need to also de-clear an equal and opposite trade. While it is theoretically possible to go find the other side (original counterparty to your trade), clearing houses just aren’t keen to perform this service (of course!). Further, as clearing houses have begun to do single-sided compression such as coupon blending, there is no guarantee any longer that there is an equal and opposite trade for every trade they have on the books.

So the only way I see “moving between clearing houses” is through the execution of LCH/CME basis trades, which will compress the original trade at one of the DCO’s.

Average Pricing

While I don’t see this offered on the TrueEX datasheet, I do occasionally hear of firms wanting to do a series of trades and have them allocated at an average price. In a simple example, if they are receivers of 10mm @ 3.0% and 10mm @ 3.5%, their average rate is of course 3.25%. However if they need to allocate equally to 4 accounts at the average price, how do you do that?

Answer seems pretty simple – perform a type of coupon blending on the original package (of two trades) and create 4 equal trades in each account. Of course coupon blending creates 2 trades per account (hence 8 total) but this is just some of the gory detail that clients want addressed.

Maybe TrueEx is operationally solving this in TrueBlend.

ACTIVITY

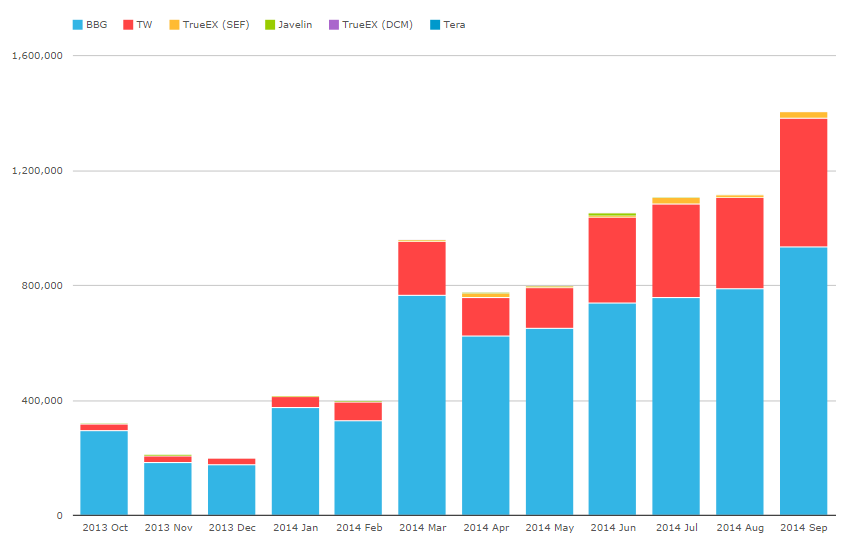

So what does this have to do with SEF Volumes? Well, I found it interesting that looking at SEFView, I see roughly $80 bn of activity for TrueEX year-to-date. Reconciling that with the TrueEX data sheet, I see that same $80 bn of activity on their SEF, but a whopping 3 trillion from PTS.

So there seems to be lots of appetite for these client-friendly bells and whistles that are happening away from the SEF itself.

The chart below is SEF volumes. If we were able to collect all PTS activity (which would be double-counting in many cases) the amounts would seemingly be much larger.

CONCLUSION

Once you get away from the interdealer trading activity, you realize clients require quite a bit of special treatment in the pre and post-execution arena. There are DCO services available for these clients, and it would seem that the SEF’s have begun to cater for these services, regardless of whether that trade was executed on their SEF or not.