We are seeing increasing volumes of Cleared Swap Compression trades and this article will take a detailed looked at the mechanics of such trades.

The Reason for Compression

Lets start with the rational for compression trades.

Every Cleared Swap trade shows up as a line item on a Clearing Statement and over time we have more and more of these line items, each one attracting a Clearing Fee. The majority of these Swaps start as MAT swaps (par coupons and on-the-run tenors) but as they age they become non-par coupons and broken date tenors. For some firms these trades may already have served their business purpose.

As termination is only available in the bi-lateral world, for Cleared Swaps the appropriate mechanism to get rid of these trades is to enter into equal and opposite trades. Equal meaning all the terms of the trade match (start date, end date, notional, fixed rate, floating rate, etc) and opposite meaning pay instead of receive or vice-versa.

The Clearing House when its sees these new equal and opposite trades, nets them with the originals, meaning that we are left with nothing or a reduced notional.

This is exactly analogous to what happens when we buy or sell a Futures contract.

So compression results in less line items and less clearing fees.

Compression vs Compaction

It should also be obvious that by entering into new offsetting trades, we are changing the risk and consequently the margin in the cleared account. This means that the transaction needs to be credit checked before proceeding.

Using CHARM we could do this easily and ensure that risk and margin would not increase massively.

Compaction refers to the fact that at the same time as compression, we enter into new Swaps that seek to preserve the risk of the trades. So we still end up with less line items but without materially changing the risk or margin. Or conceivably changing risk to a a desired goal. Again we could check this using CHARM.

The Mechanics

The business process is as follows:

- A customer identifies a list of cleared trades that they would like to compress/compact

- This list of trades is loaded onto a SEF, credit checked and sent to dealers

- Dealers quote to enter into opposite trades, in essence an NPV for the list

- The customer agrees to execute with a chosen dealer

- The whole list is transacted in one go

- With the NPV being paid or received by the customer

- The resulting executed trades are reported to an SDR and sent to a Clearing House

- The Clearing House extinguishes line items (in its overnight batch)

- Next day the customers clearing statement shows less line items

- Resulting in lower clearing fees

Note: CME and LCH are planning on relaxing the need to match the fixed rate exactly by introducing coupon blending approaches. One result of this is that the NPV will no longer be as large (so less cash changes hands) and another that more swap line items will net together.

Differences to TriOptima

For those of you familiar with TriOptima’s triReduce compression service, which has been running for many years in bi-lateral swaps trading, the differences should now be obvious. triReduce is a service where participants agree to terminate existing swaps with no change in market risk (or within a tolerance). The result of the multi-lateral compression cycle is binding and everyone then terminates their bi-lateral swaps. Note that these Terminations are also reported to SDRs.

Real Data

Lets now look at some real figures reported in the most recent two weeks by two SEFs.

Using SEFView, we can isolate just trueEx and Tradeweb and do so for IRD:Vanilla in USD.

Which shows $22.674 billion reported by trueEx over 7 business days in this 10 day period.

trueEX

We know that for trueEX the reported volumes are exclusively from their PTC platform.

If we were to drill-down on the 14 July 2014 figure of $2.589 billion, we would see that this is reported as a 2Y tenor transaction, but with no other details.

However we know that these trades would also have been reported to an SDR.

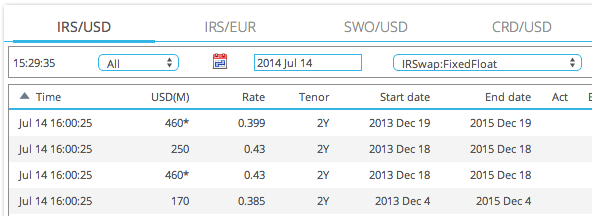

Using SDRView Pro, we can select the 14 July and instead of Spot, pick the sub-type “Old” (meaning trades with effective date prior to our chosen date of 14 July).

Sorting by time, we find the following four 2Y trades.

From which we can see that:

- These 4 trades were all executed at 16:00 LON or 11:00 NY.

- The original trades were 2Y swaps when executed in Dec 2013.

- The fixed rates these were executed at are 0.399, 0.43, 0.43 and 0.385.

- Two of the trades are capped at $460 million

- So the total of the 4 trades is $1.34 billion

- Instead of the $2.5 billion shown in SEFView

In addition if we were to drill-down on these trades, we would see that two of them had additional fees of $471,115 and $866,852.

These are the aforementioned NPVs, exchanged by the parties to enter into the offsetting swaps. Which we could check by re-valuing these trades on 14-July, on which date they would be 1Y and 5 months tenor.

Tradeweb

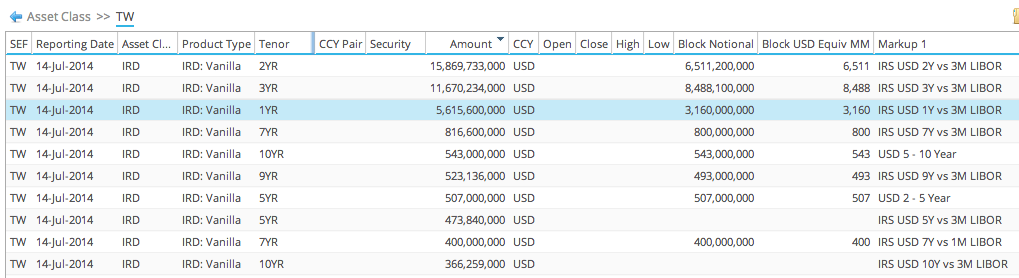

Tradeweb on 14 July 2014, reported $37 billion, a much higher figure than on any other day in the period.

Lets now drill-down on this figure.

From which we can see that:

- 2Y has $15.8 billion

- 3Y has $11.6 billion

- 1Y has $5.6 billion

- Each of which are much higher than other tenors

- Each of which are much higher than other days for these tenors

- The total of these three tenors is $33.2 billion

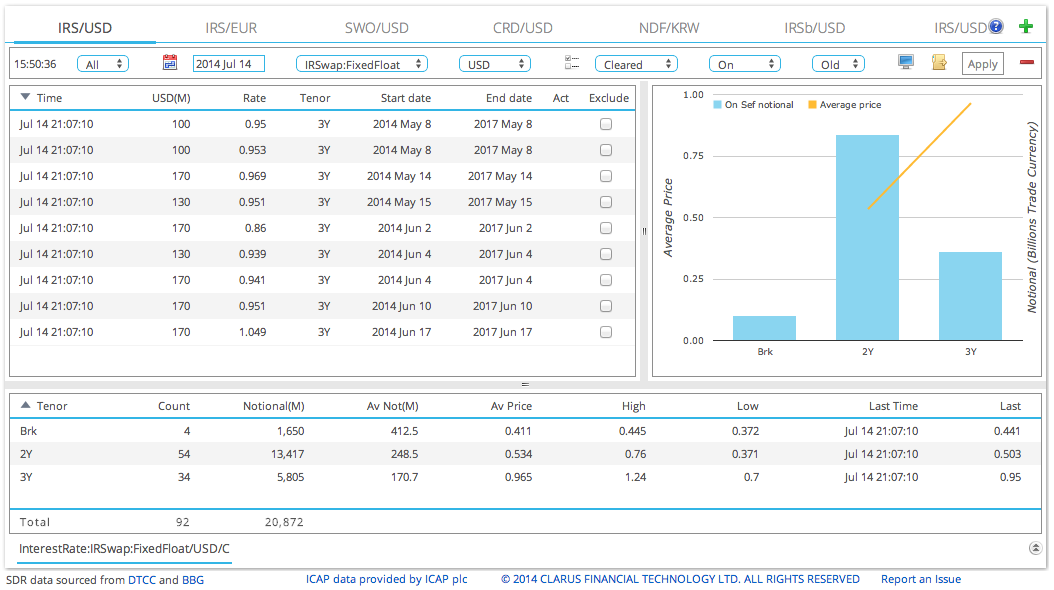

Can we find these trades in SDRView? Lets try.

Sure enough, we can see:

- 92 trades with $20.8 billion gross notional

- Remember that 4 of these are the trueEx deals (with $1.34 billion).

- So we have 88 trades with $19.53 billion

- All of these are executed at 21:07 LON or 4:07 NYC.

- So we can assume they were transacted as one list

- 21 of the trades are capped, so we know the gross notional is higher than $19.5b

In addition, if we drill-down we find that only one of the trades has an additional fee, which is $3,276,805.

We can assume that this is the NPV that changed hands for these 88 trades to be transacted to offset the existing aged 88 trades.

And the overall gross notional must have been close to $33 billion for these trades.

Probably a little less as the Tradeweb SEFView volumes probably include other 1Y, 2Y & 3Y trades.

In my recent blog, A Six Month Review of Swap Volumes, I noted the sharp risk of Tradeweb volumes in June.

We can now presume that some part of this was down to Compression and Compaction trades.

Summary

Compression and Compaction trade volumes are now significant.

These trades serve to reduce line items and clearing fees, by removing trades that are no longer needed.

The mechanics involves executing new trades with matching terms and opposite direction.

Which Clearing Houses then Net (extinguish) in an analogous manner to Futures.

SEFs are natural platforms for automating the data and process that needs to flow back and forth between parties.

trueEx launched its PTC service in Dec 2013 and has shown good volume each week (see SEFView).

Tradeweb launched its compression platform in Nov 2013 and executed significant volume in June and July; which accounts for part of its recent increase in IRD volumes relative to other SEFs.

SDRView can be used to see the compression activity, including the executed trade list and associated price (NPV).

New transparency for us all.

Provided we have the time and tools to become informed.