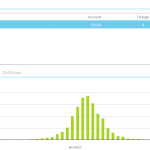

How much Initial Margin will Uncleared Derivatives require in the first month of trading?

Uncleared Margin Rules (UMR) come into effect as of 1st September So let’s play a fun little game. Take the SDR data for Uncleared Derivatives. Import this data into CHARM, our Initial Margin and Risk tool. Make a few broad assumptions about the trades and the Dealer market. We end up with an estimate of how much IM […]

Higher Swap Margins after Brexit

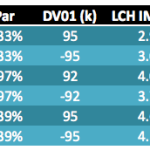

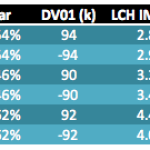

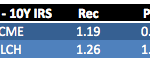

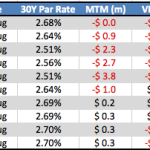

Last week I looked at Brexit – The Impact on Swap Margin and stated that we will start to see increases in Initial Margin particularly for GBP Swaps. Now that a week has passed lets look at the what the data shows. Cleared IRS 10Y Lets start by using CHARM to calculate the IM of 10Y par vanilla swaps […]

BREXIT – The Impact on Swap Margin

Given the large moves in Swap rates that we highlighted in our BREXIT Day One and Day Two blogs, I thought it would be interesting to look at the impact on Swap margins. Cleared IRS 10Y Lets start by using CHARM to calculate the IM of 10Y par vanilla swaps in EUR, GBP and USD. Showing that on 23 […]

Margin Valuation Adjustment

While it all began many years ago with Credit Valuation Adjustment (CVA), a number of new XVAs have risen to prominence in the last few years such as DVA, FVA, MVA, KVA. Chris wrote about Funding Valuation Adjustment (FVA) last week, so today I will look at Margin Valuation Adjustment (MVA). Background MVA arises when Initial […]

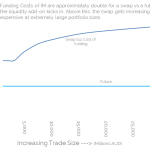

FVA for Cleared Swaps

We’ve recently added Margin Valuation Adjustment analysis into CHARM. As we’ve talked about in the past (here and here), MVA is a cost to the business because Initial Margin has to be funded for the holding period of a trade. This blog considers FVA – Funding Valuation Adjustment – caused by the Variation Margin of trades. All Swaps impart a […]

Compression in Swaps

We run a real compression exercise through CHARM… …showing the potential IM reduction from a compression run Depending on the exact portfolio, the ratio of NPV unlocked to the IM released can be highly variable…. …taking a recursive process to accurately assess your capital efficiency. This is exactly why pre-trade analysis of Compression using high quality, high performance engines such […]

AUD swap market: Concentration risks from the Clearing Mandate

We present a uniquely Clarus view of the AUD IRS markets Our analysis of the regulatory landscape, bond issuance data and swap market flows suggests that many Swap Dealers will end-up in Add-On territory for OTC swaps clearing at CCPs This means that swaps become incrementally ever more expensive to trade relative to futures From a liquidity point of view, […]

China’s Black Monday and Volatility of Swap Margin

We all know that the Shanghai Composite Index has seen massive volatility with the media dubbing August 24th as China’s Black Monday with the Index falling 8.5% and then a further 7.6% on the 25th. So I thought it would be interesting to look at how a USD Interest Rate Swap trade performed over this […]

Principal Component Analysis of the Swap Curve: An Introduction

Principal Component Analysis (PCA) is a well-known statistical technique from multivariate analysis used in managing and explaining interest rate risk. Before applying the technique it can be useful to first inspect the swap curve over a period time and make qualitative observations. By inspection of the swap curve paths above we can see that; 1. […]

CCP Default Management Process and the SwapClear Fire Drill

There has been a lot written in the press about the increased importance of Central Counterparties (CCPs) and the cash and capital resources available in the event of member defaults. A CCPs Default Management Process (DMP) documents the steps to be taken in the event of a member default. These are designed to utilise the defaulting members margin to […]