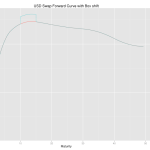

Swap Equivalents via Waves

In a recent paper, “Calculating Delta Risks and Hedges via Waves (2015)“, Hagan deals with an old practical problem–determining risk and hedges on an interest rate book. In older systems a delta hedge report is often implemented by perturbing quotes used to construct the yield curves, restripping the curves and then revaluing the book. As […]

Client Portfolios will Dominate CCP Risk

Using Client Open Interest figures we can project the share of CCP portfolio risk due to Clients once Clearing reaches a mature state. This will take several years as legacy non-cleared Rates portfolios (which dominate global notional outstanding) need to run off and be replaced by cleared trades under the US, EU and Asia client clearing mandates. However, […]

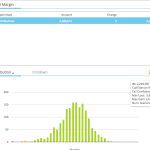

Can SPAN Margin for Futures be higher than HistSim Margin?

Following on from my article on Portfolio Cross-Margining of Swaps and Futures, I wanted to take a more detailed look into the Initial Margin of Interest Rate Futures. In this article I will compare SPAN with Historical Simulation and check whether SPAN margin is always lower than HistSim margin, which is what we would expect given […]

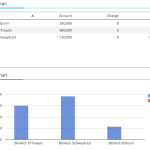

Portfolio Cross-Margining of Swaps and Futures

We often get asked about Cross-Margining of Swaps and Futures, as well as SPAN margin for Futures. In this article I will introduce the benefits of cross-margining, using a few simple examples and the CME Clearing model. As this is my first article on this topic, I will endeavour to keep it as simple as possible […]

HFT in the Swaps market – it’s a good thing!

I thought it was very interesting this week that Commissioner Giancarlo mentioned the potential emergence of HFT in the swaps trading landscape. From a quick read of his remarks, it sounds like he is not a great supporter of continuous CLOB trading as the only mode of swap execution. But what if enabling HFT in […]

Initial Margin and Swap Pricing

Welcome to 2015 everyone! I thought I’d start the year with some simple thoughts on Initial Margin, before later applying these to what may (or may not!) be charged when dealers quote on a compression run that we identified using the SDRView Pro API. Initial Margin Basics As Amir has covered in a number of […]

Margin Games 2014

2014 So, it’s that time of year when we look back at 2014, the year that was. We go through the (painful) year-end reviews, give the year a mark out of 10 if you must. Think about all of the tail events you’ve traded through during the year. Those once-in-10,000-lifetime events that seem to occur at least […]

JAVELIN’S 2-DAY VAR LETTER: WHAT DOES IT MEAN?

A short while ago I saw the letter written by Javelin to the CFTC regarding MAC swaps and margin. The press release can be found here. My brief synopsis: Swap futures are equivalent (in terms of risk) to cleared OTC MAC contracts Swap futures enjoy 2-day VaR margining (SPAN or SPAN like) OTC MAC contracts are […]

Price Making in Swaps and Sharpening your Axe

Market making in Swaps is a business in the midst of significant change. Regulatory drivers are increasing cost and complexity and while central clearing has helped, it has not yet simplified the business to one which is automated, high-volume and low cost. When making prices Swap dealers have “usually had an axe”, meaning a bias to […]

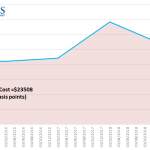

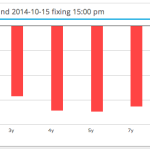

Stress Testing of Initial Margin and Procyclicality post Oct 15th

There has been much comment on the market moves in the US Treasury market on October 15, 2014. Our article Swaps and the Flash Crash described what we saw in Interest Rate Swaps. So I thought it would be interesting to look at what this period of market stress and higher volatility means for Cleared Swap Margin requirements. And […]