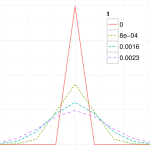

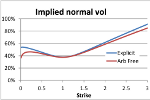

Arbitrage-Free SABR: Finite Difference Techniques

In January a new approach to the SABR model was published in Wilmott magazine, by Hagan et al., the original authors of the well-known SABR model. They review some of the weaknesses of the model, and concentrate on the problem of negative probabilities induced by the original approximation formula, especially at low strikes. To solve […]

Push, Ping and Charm

Last week we announced our CHARM product with a press release titled, Swap Margin Check in 10 milliseconds. In this article I will provide the detail behind our thinking. CCP Mandatory Clearing of Swaps in the US, means that CCPs have to perform a Clearing Acceptance Check, which requires first checking that the executed trade submitted to […]

Valuation of Massive OTC Portfolios: From Milli-Seconds to Micro-seconds

In the not to distant past I can recall seeing several risk systems valuing vanilla interest swaps with individual trade valuations taking around a few milliseconds. Whilst quants might rightly be alarmed that it would take so long, when one adds in overheads which can easily occur in the integration of a pricing library with […]

Value at Risk, what you should know, overview and detail

Last week I presented Value at Risk to a meeting of the CFA Institute. The brief was to provide an introduction to Value at Risk, why it is used in capital markets, how is it calculated, strengths and weaknesses. As such it needed to provide an introduction, some detail and an analysis, all in 1 hour […]

LCH Swapclear Margin, the need for change and the impact

LCH SwapClear have just implemented a change in their Initial Margin methodology and this article will discuss three elements that constitute the change: Historical look-back period, increased from 5Y to 10Y Relative scenarios changed to absolute scenarios Worst Loss to Expected Shortfall Ten Years This is the most obvious change, because as we approach the […]

Arbitrage free SABR and near negative rates

This week in London the Thalesians hosted a presentation by Pat Hagan titled ‘Arbitrage free SABR‘. Knowing the popularity of Pat’s presentations, I had planned to arrive early to ensure I had a good seat, unfortunately I mis-calculated how long it took to get from the City to Canary Wharf, and so I arrived on […]

Central Counterparty Clearing Workshop

The Dodd-Frank Act in the US and the EMIR Directive in Europe have mandated the requirement for Interest Rate Swaps to be cleared at Clearing Houses. One of the most significant differences in market practices from this change is the requirement to post collateral to meet the Initial Margin requirement. “Initial Margin for Cleared Swaps” […]

CCP Initial Margin for Interest Rate Swaps

The Dodd-Frank Act in the US and the EMIR Directive in Europe have mandated the requirement for Interest Rate Swaps to be cleared at Clearing Houses. One of the most significant differences in market practices from this change is the requirement to post collateral to meet the Initial Margin requirement. At the recent 13th Annual […]