Guest Blog Series

Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

Super Mario to the rescue? No, not this Mario. Draghi was again even more dovish than expected at the central-banker’s annual shindig in Jackson Hole. Veering from the script, it looks like he’s ready to push the Bundesbank toward QE and ignore their deeply-ingrained fear of hyperinflation. What will the Eonia market have to say? It’s prediction time.

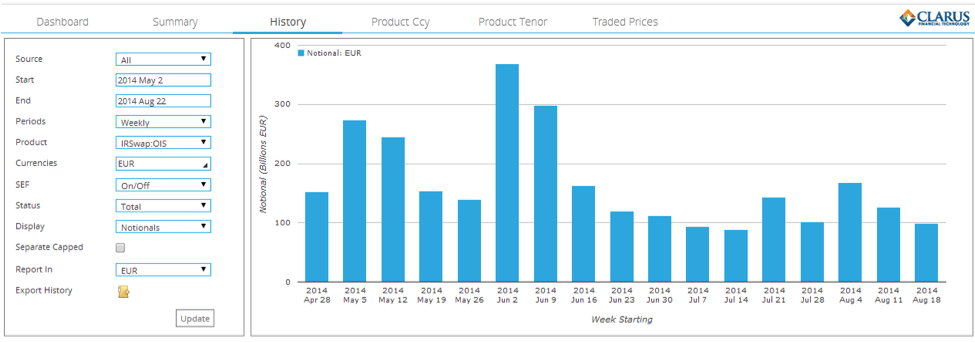

First off, it’s important to note that the Eonia-markets have been a follower not a leader. Draghi was Dovish at the May press conference; cue a flurry of trading. Draghi actually did something at the June meeting; cue a much larger flurry of trading – see below from SDRView Researcher:

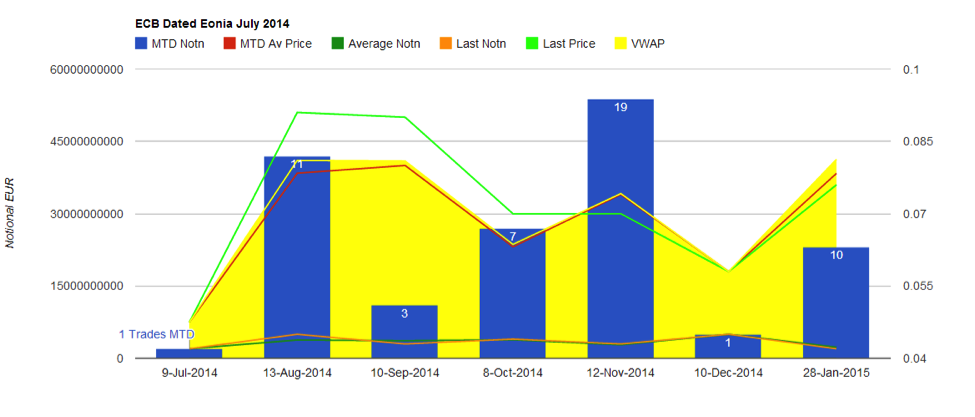

As we can also see, the July meeting was a non-event and (thankfully) no-one had to cancel an August holiday as that meeting was also non-eventful. Drilling down into the data via the SDRView API, let’s compare July’s activity in ECB-dated swaps to what we see in August so far:

It’s notable in July that the VWAP and average prices were considerably below the last traded prices for the August, September and October meetings. November was more stable despite it being the focal point for trading and it is notable how few trades (3) we saw for the September meeting. Compare this to what we have seen in August so far:

It’s notable in July that the VWAP and average prices were considerably below the last traded prices for the August, September and October meetings. November was more stable despite it being the focal point for trading and it is notable how few trades (3) we saw for the September meeting. Compare this to what we have seen in August so far:

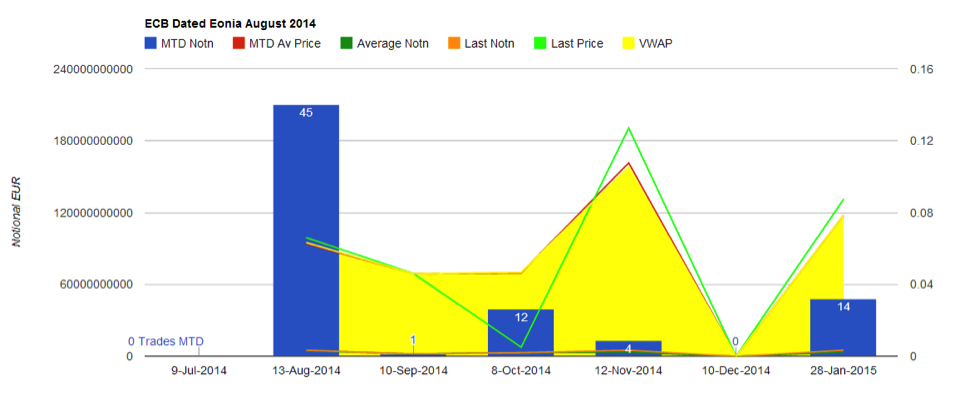

Yup, September is still being largely ignored by markets. October and January are seeing similar amounts of activity in terms of trade count, although activity in November has dropped-off a cliff. I’m writing this on Monday 25th – a UK Bank Holiday, so there’s no quieter day to break-out the soothsayer’s tools and make some predictions. However, it also means we have a whole week of August left for the market to look again. What should we expect?

Well, we cannot ignore the sheer number and size of trades that took place in the August meeting, which passed without event. With the ECB on such a dovish leaning, we have to expect a sharp increase in September activity over the coming days.

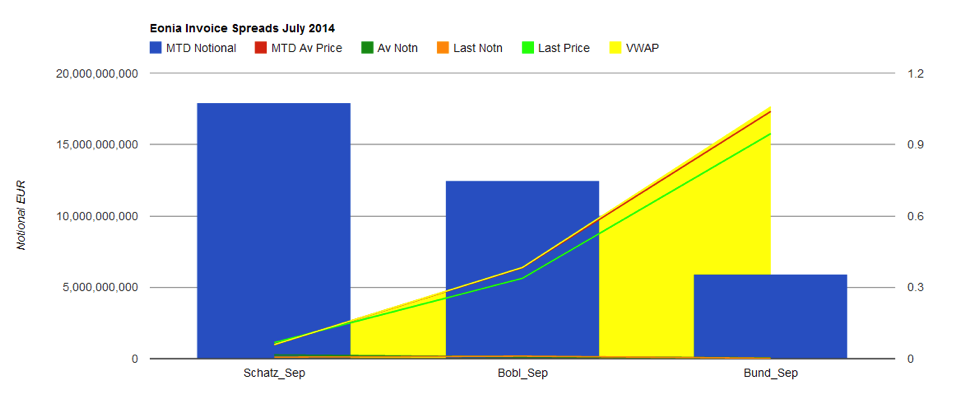

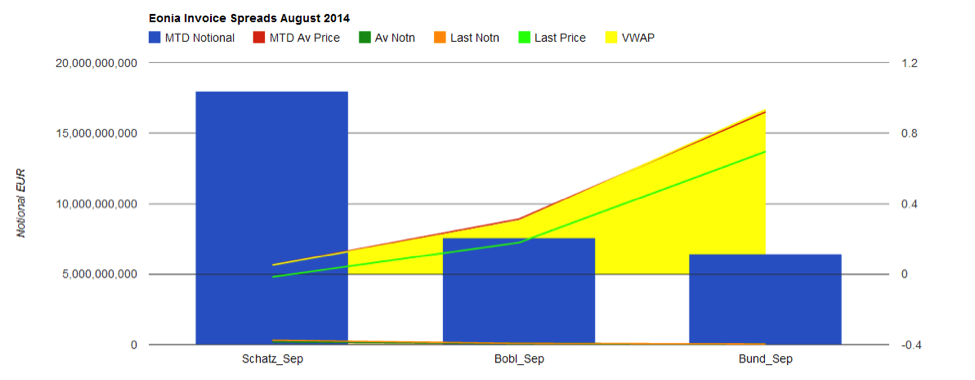

Or do we? We can actually explain why the September meeting is so thinly traded by looking at another Eonia structure. It looks like dealers are exposed to this meeting already, through one of their favourite esoteric structures – invoice spreads. Here’s the data for Eonia Invoice Spreads for July:

In a nutshell, we see Schatz broadly stable, whilst the curve flattened during the month, with Bunds and Bobls ending below the VWAP. So far in August and we can see a telling sign:

Yup – Schatz levels are in negative territory and prices are moving lower across the curve. With the Schatz Eurex delivery date the same as the start of the next ECB maintenance period – 10th September – market players can obtain exposure to the September meeting dates without explicitly trading the exact dates. Indeed, with only 31 ECB-dated trades outside of the front meeting date in August, the most liquid animal looks to be the Schatz invoice spread with 62 trades MTD.

With Euribors seeing a mini melt-up in response to Draghi’s speech, it looks like the September meeting is firmly in play.

I would actually prefer more of a flattening play for the ECB dates, allowing for the possibility that the ECB further tweak the TLTRO terms, finally activate their ABS programme – and even look at cutting rates again.

Therefore, ahead of the September meeting expect to see continued healthy volumes in the Schatz spread, with people likely choosing to pay meeting dates in 2014 vs any receiving flows.