SEF, Oct 2, What happened to EUR IRS trading?

Following on from my article SEF, Oct2, What does the SDR Data show? I wanted to take a further look at what else we can observe in SDRView using the DTCC real-time price dissemination feed source. Whats happened to IR Swaps in EUR, GBP & JPY? Daily Volumes in these three major currencies seem to have dropped […]

SEF, Oct 2, What does the SDR data show?

As yesterday was the first day for Swap Execution Facilities (SEF) trading, I decided to look at what the data in a Swap Data Repository (SDR) can tell us about what happened on Day 1. The DTCC real-time public dissemination feed has a field name “Execution Venue”, which prior to Oct 2 always had the value […]

Real-time reporting of Swap transactions

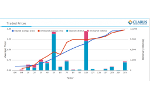

Today we put out a press release announcing the real-time reporting of Swap transactions in our SDR View application and I wanted to provide some further insight into the value and importance of this. First lets start with some recent history, always a good start for financial markets. The DTCC DDR real-time dissemination dashboard has […]

SDR View, Capped Notional Changes

Those of you that read my blog post SDR, Block Trade Rule, 30 July Update will know that from 30th July, we moved from the interim period to the initial period. One of the main changes introduced was that capped notionals were increased and that blog has the before and after tables for US IRS Swaps. […]

SDR, Block Trade Rule, 30 July Update

Those of you that read my previous post on the Block Trade Rule will know that on July 30th we moved from the Interim period to the Initial period. This means two significant changes, firstly that the public dissemination of all trades is no longer delayed by 30 minutes, only block trades are delayed and secondly […]

Swap Data Repository, Block Trade Rule, the Bad News

Under the Dodd-Frank Act, the CFTC issued Part 43 of its regulations to implement the real-time reporting mandate. This has a requirement for “real-time public reporting”, which is defined as “to report data relating to a swap transaction, including price and volume, as soon as technologically practicable after the time at which the swap transaction […]

Competition | June 10 Prediction | The Results

Today ClarusFT (and OTC Space) announce the result of our competition to predict the impact of the Dodd-Frank Act mandatory clearing deadline of June 10th. The question we posed was the following: What do you predict will be the gross notional remaining of Uncleared USD IR Swaps FixedFloat in the week of 10th – 14th June 2013, as reported to […]

Win a Nexus 7, Kindle Fire or Apple iPad mini

The Dodd-Frank Act has a mandatory clearing deadline of June 10th for Category 2 entities (hedge funds, non-swap dealer banks) We are asking the following question: What do you predict will be the gross notional remaining of Uncleared USD IR Swaps FixedFloat in the week of 10th – 14th June 2013, as reported to the USD […]

Cleared Swap prices versus Bi-lateral Swap prices

Last month, I posted a blog titled “Swaps, Actual Traded Prices and Size”. Today I would like to make a correction in one of the interesting insights I noted in that blog. Namely the point that the “The price differences between UnCleared and Cleared Swaps can be observed and is sizeable” and I went on […]

Is a Chart worth a hundred words or more?

We have all heard the adage “a picture is worth a thousand words”, well today I am going to postulate that “a chart is worth a hundred words or more” and also “a chart is a hundred times quicker in conveying key information”. A few weeks ago, we released our SDR View, which while great […]