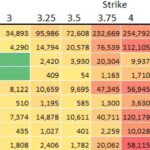

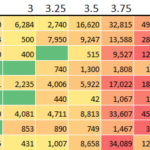

Swaption volumes by strike – Q1 2025

This post looks at USD swaptions activity in Q1 as part of our regular quarterly coverage, the last of which was Swaption Volumes by Strike Q4 2024. Swaptions basics If you are uninitiated in swaptions, here are some basics: Now, on to the post. Swap market context Q1 2025 saw the following daily price moves […]

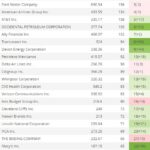

Most active names in Credit Derivatives – April 2025

After about a year since our last blog on this topic, it is high time for another look at the most active names in CDS, using data reported to US SEC Securities Based Data Repositories (SBSDRs). CDS on sovereigns Using SBSDRView, we can find the most active sovereign CDS trades in April 2025, starting with USD activity. Table 1 – […]

2024 SEF volumes and share in SOFR swaps

SOFR Swaps at D2D venues were usually spreadover, butterfly, curve switch or CCP switch packages. On D2C venues, spot-starting SOFR swaps were dominated by outright trades. As well as spot-starters, forward, IMM and MAC SOFR swaps also trade in significant numbers on D2C venues (unlike D2D venues). Continue reading for the charts, tables, and details. Background This post iterates, for […]

2024 US SDR-Reported IR Compression

Key takeaways: Data background For 8+ years, SDRView data has included the package type field to allow compression to be broken out from outright and other package types. In late 2022 we used the CFTC reporting upgrade to immediately add platform id which allows platforms’ compression market share to be analyzed. Platform id values consist […]

Transparency – Where do we go from here?

USD OIS Trading The chart below shows the entire global USD OIS cleared swaps market in 2024: The chart shows the amount of DV01 traded in benchmark maturity buckets – ranging from 2Y to 50Y – in USD OIS versus both SOFR and Fed Funds. The data is from CCPView. This data is reported directly […]

Swaption Volumes by Strike Q4 2024

Continuing the work on Swaptions, I delve into the options market activity in Q4. The quarter was characterised by trading activity related to the US election, and from a data perspective we cannot avoid giving a notable hat tip to the change in block sizes. Q4 2024 saw the following daily moves in ten year SOFR […]

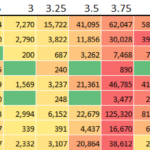

Swaption Volumes by Strike Q3 2024

This blog covers USD Options markets in Q3 – so please note that is before the election result! This is the latest in a series of blogs covering Swaptions: Q3 2024 was a characterised by huge volumes in underlying Swaps, with notable activity in August. There was also a lot of activity tied to changes […]

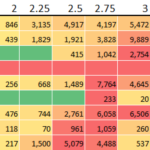

Volumes in EUR Swaptions

June 2024 saw the largest number of EUR Swaptions reported to SDRs in the past three years: Showing; My interest in EUR Swaptions was sparked by a recent Risk.net article; I’m not sure our data shows much support for the idea that it was straddles specifically that led to a spike in volumes. Further complicating […]

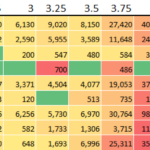

Swaption Volumes by Strike Q2 2024

This blog follows on from the interesting activity we have seen across Options markets so far this year. Take a look if you have missed anything: I have written previous Swaption reviews after large, directional moves in Rates. Q2 2024 was a little bit different, although it would still be characterised as a “volatile” quarter. […]

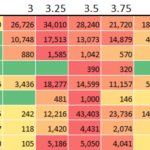

Swaption Volumes by Strike Q1 2024

Time to update and revisit one of our most interesting 2023 blogs – Swaptions: Swaptions showcase a different use case for SDR data, and highlight why data augmentation is necessary. Straddles Are Back! My previous look at 2023 trade counts highlighted: As soon as we noticed this, we set our sights on identifying Straddles again […]