Most Active Names in Credit Derivatives – April 2024

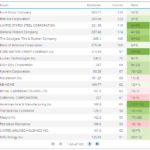

More than six months have passed since I last looked at the most active names in CDS and TRS, so high time to take a look at recent data from US SEC Securities Based Data Repositorys (SBSDRs). CDS on Sovereigns Using SBSDRView, we can find the most active sovereigns for CDS trades in April 2024. The above list was a […]

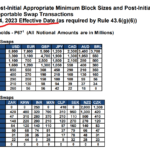

Dec 4th has been and gone. Where are our new block sizes please?

Back in June 2023, I covered the new block sizes that were due to come into effect on 4th December 2023. In case you missed them, please take a look before reading today’s blog: However – in what appears to be new news – the CFTC issued a No Action letter late in October to […]

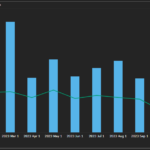

Time Series of Swap Prices and Volumes

Analysing existing datasets in new and novel ways, often throws up interesting insights and questions which help with our understanding of the real world and in turn help us to make better decisions. Today I wanted to showcase a new feature in SDRView, that demonstrates this, the Ticker Summary View. SDRView has transaction level data […]

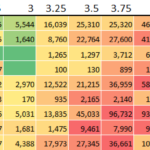

Swaption Volumes by Strike Q3 2023

Sometimes this blog would benefit from another Chris Barnes or Amir Khwaja! It has taken me until the tail-end of 2023 to revisit one of the most popular topics on the Clarus blog – Swaptions: I do not know which of the ~85 blogs I should not have written since I last wrote about Swaptions, […]

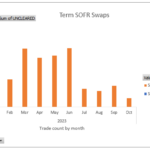

Term SOFR and BSBY Volumes – October 2023

I last looked at Term SOFR and BSBY Volumes in May2023, so today I will look at the YTD 2023 data trends for these indices, and as before seperate Term SOFR (published by CME) from Average SOFR (NY Fed). A one-sentence summary is that “Term SOFR Swap volumes are down, though still far higher than Average […]

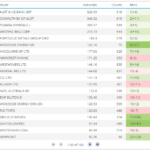

Most Active Names in Credit and Equity Derivatives – August 2023

I last looked at the most active trading names in CDS and TRS in May 2023, so today I will look at August 2023 data from US SEC Securities Based Data Repositorys (SBSDRs). CDS on Sovereigns Using SBSDRView, we can find the most active sovereigns for CDS trades in August 2023. The above list was a […]

SOFR Swaps Volumes and Share – July 2023

Let’s update my blog on IDB Market Share in SOFR Swaps with the most recent data and expand the coverage to also include D2C venues. Types of SOFR Swaps SOFR Swaps in the IDB (inter-dealer broker, D2D) market trade primarily as Spreadovers to US Treasuries. This is by far the most frequent trade type in […]

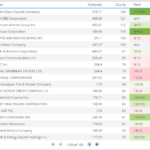

Most Active Names in Credit and Equity Derivatives – May 2023

Last month I looked at the most active trading names in CDS and TRS in April 2023, so today I will update that for May 2023. This data is from U.S. SEC Securities Based Swap Data Repositorys (SBSDRs). CDS on Sovereigns Using SBSDRView, we can find the most active sovereigns for CDS trades in May 2023. […]

Most Active Names in Credit and Equity Derivatives – April 2023

I last looked at the most active trading names in CDS and TRS in January 2023, so today I will update that for April 2023 data. This data is from U.S. SEC Securities Based Swap Data Repositorys (SBSDRs). CDS on Sovereigns Using SBSDRView, we can find the most active sovereigns for Credit Derivatives trades in April […]

IDB Market Share in SOFR Swaps

Types of SOFR Swaps SOFR Swaps in the IDB (inter-dealer broker) market trade primarily as Spreadovers to US Treasuries. This is by far the most frequent trade type for IDBs, with the highest volume in notional or dv01 terms and the most important in setting prices of SOFR Swaps. Next are Curve/Switch trades, which are […]