4Q 2019 CPMI-IOSCO Quantitative Disclosures for CCPs have just been published and while we are still focused on the Covid-19 pandemic and resulting market volatility, I thought it would be interesting to see what the data shows as of a Dec 31, 2019, before we had any idea what was coming.

So a little different to my usual quarterly blogs on this topic, see CCP Quantitative Disclosures 3Q 2019.

Summary:

- Pre-funded member contributions to the Default Fund are up year-on-year

- Across IRS, ETD, CDS, Bonds, Equity Options

- We see large increases at CME, Eurex, DTCC, ICE, LCH, OCC

Background

Under the CPMI-IOSCO Public Quantitative Disclosures, CCPs publish over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing and more.

CCPView has over 4 years of these quarterly disclosures for thirty-six Clearing Houses, each with multiple Clearing Services, covering the period from 30 Sep 2015 to 31 Dec 2019. This data provides both insights into trends over time at one CCP and comparisons between CCPs.

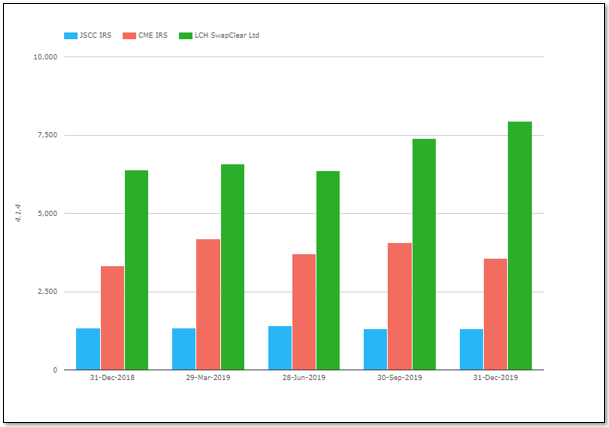

Default Resources

Where better to start than a look at some of the Default Resources that Clearing Houses held as of Dec 31, 2019 going into the Covid-19 Crises, to meet any losses in excess of a defaulting member margins.

- LCH SwapClear significantly increasing to $7.9 billion from $6.4 billion a year earlier

- CME IRS also up to $3.6 billion from $3.3 billion

- JSCC IRS similar from a year earlier at $1.3 billion

- CME significantly increasing to $4.9 billion from $4.4 billion a year earlier

- Eurex also up a similar amount from $3.6 billion to $4.1 billion

- ICE Europe F&O again up a similar amount from $2.8 billion to $3.2 billion

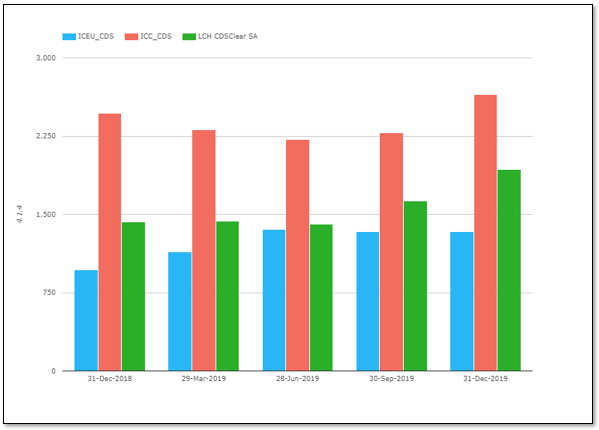

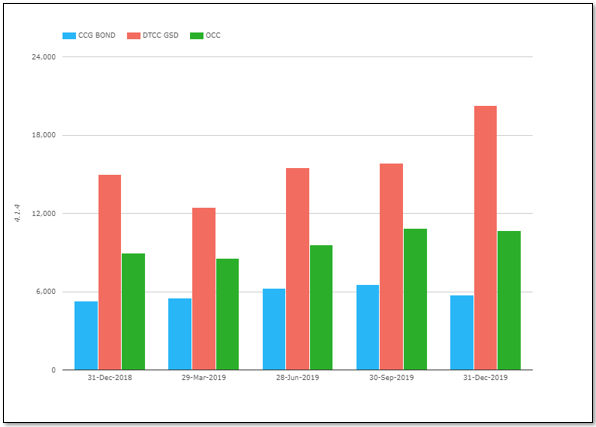

- A similar picture of increased prefunded contributions

- DTCC Government Securities Division, a massive increase to $20.3 billion from $15 billion a year earlier

- Options Clearing Corporation up from $9 billion to $10.6 billion

- CCG Bonds up from $5.3 billion to $5.7 billion

So across the board, IRS, Futures, CDS, Bonds, Equity Derivatives , we see the same trend; higher pre-funded member contributions to the default fund.

Timely, to say the least; the calibration of default resources based on credit stress tests, cover 2 losses, market volatility and increased participation in clearing has led CCPs to increase pre-funded member contributions.

A good place to be at the start of a financial crisis and so far (touch wood), except for Ronin Capital defaulting at CME, which was covered by the defaulting members resources, I have not heard about any defaults.

Given the massive margin calls that must have been raised in February and March, that is a testament to the soundness of CCP risk management.

More Disclosures

CCPView has disclosures from thirty six Clearing Houses, each with many Clearing Services, so there is a lot more data to look at covering Equities, Bond, Futures, Options and OTC Derivatives.

With over 200 quantitative data fields and quarterly figures from September 2015 to December 2019, that is a lot of data to analyse.

If you are interested in this data please contact us for a CCPView subscription.

If your firm is not already a subscriber, it would be great to have you as a customer.