- Clarus Microservices make it easy to get Swaps data

- Swap volumes can be retrieved from SDRs using simple Python

- This data can be displayed in Tables and Charts

- Our Sandbox allows you to try quickly in your Browser

Introduction

Under the Dodd-Frank Act, all swaps, whether cleared or uncleared, that are executed by US persons, need to be reported to a Swap Data Repository (SDR).

The SDR data is available via the Clarus Microservices API. It can be easily retrieved using simple Python programming language.

In this blog, I will demonstrate a few of the SDR functions available in the Clarus API. The functions take BBG tickers and return values such as notional and dv01, which can then be presented in charts and tables.

Volume and DV01 of Outright Trades

To start, I specify the BBG tickers for outright trades on six major tenors and then use the function sdr.volume to get notional and dv01 for each.

bbg_tickers = 'USSW2, USSW3, USSW5, USSW7, USSW10, USSW30' notional = clarus.sdr.volume(ticker=bbg_tickers, volumeType='notional') dv01 = clarus.sdr.volume(ticker=bbg_tickers, volumeType='dv01')

The output from the above two API calls is shown below:

Ticker Period Start Period End Volume Type Volume

USSW10 2018-08-03 2018-08-03 NOTIONAL 3231600000

USSW2 2018-08-03 2018-08-03 NOTIONAL 2768000000

USSW3 2018-08-03 2018-08-03 NOTIONAL 633000000

USSW30 2018-08-03 2018-08-03 NOTIONAL 973000000

USSW5 2018-08-03 2018-08-03 NOTIONAL 3104000000

USSW7 2018-08-03 2018-08-03 NOTIONAL 891000000

Ticker Period Start Period End Volume Type Volume

USSW10 2018-08-03 2018-08-03 DV01 2758311

USSW2 2018-08-03 2018-08-03 DV01 474617

USSW3 2018-08-03 2018-08-03 DV01 168557

USSW30 2018-08-03 2018-08-03 DV01 2013724

USSW5 2018-08-03 2018-08-03 DV01 1388505

USSW7 2018-08-03 2018-08-03 DV01 551946

In just a few lines of basic Python code I was able to get Notional and DV01 volumes for today , August 3, 2018 for these major tenors.

To collate the data in a table, I will use a popular data manipulation library in Python called Pandas.

From the above output data,Tickers, Notional, and DV01 are loaded into a new Pandas dataframe.

import pandas as pd

df = pd.DataFrame({'Ticker': notional['Ticker'], 'Notional': notional['Volume'], 'DV01': dv01['Volume']})

Next, I want to append more data to the above dataframe, which would include the Tenor, the Average DV01 for the prior 30 days, and its difference from the daily DV01.

df['Tenor'] = [int(i[4:]) for i in df['Ticker']] df['Avg DV01'] = [clarus.sdr.volumeadv(ticker=i, volumeType='dv01').get_value(0,'ADV') for i in df['Ticker']] df['%Deviation'] = df['DV01'].astype(float)/df['Avg DV01'].astype(float)*100 df = df[['Ticker', 'Tenor', 'Notional', 'DV01', 'Avg DV01', '%Deviation']].sort_values(by='Tenor', ascending=True)

In the above block of code, I first strip the Tenors from the Ticker symbols.

Next I call the clarus sdr.volumeadv API function to get the Average DV01 volumes for the prior 30 days for each Ticker independently.

I then calculate the difference between the daily DV01 with the Average DV01 for the last 30 days to get the %Deviation.

Lastly, I set the columns in order and the Tenors in ascending order to get the dataframe below:

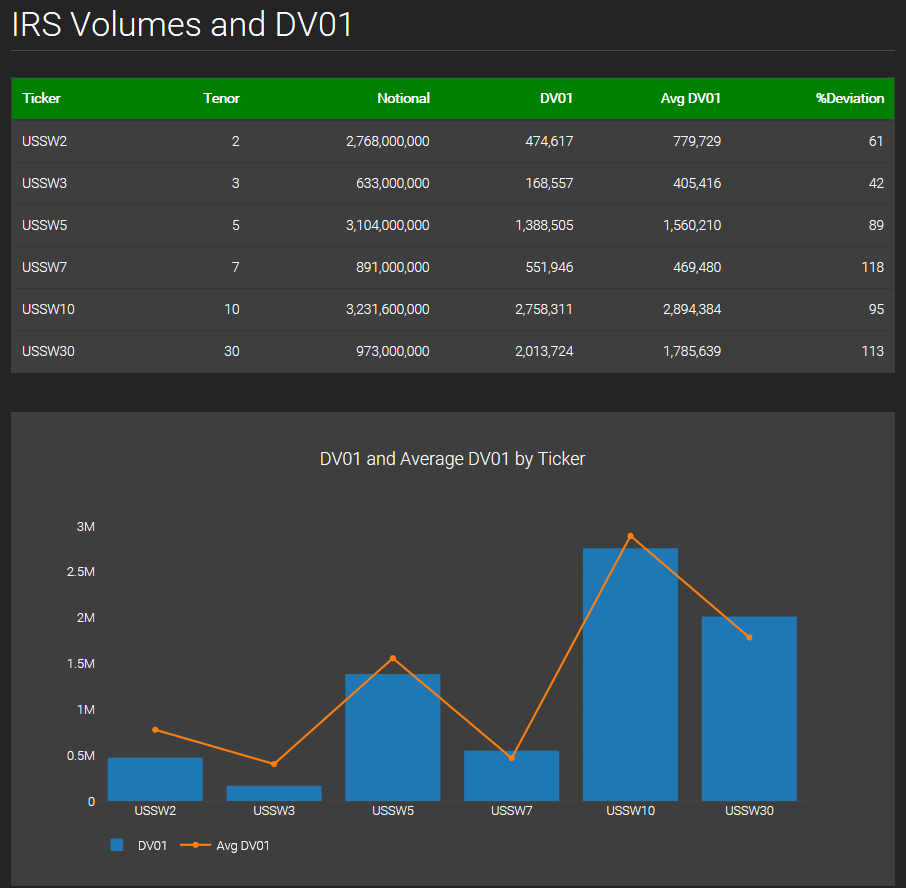

Ticker Tenor Notional DV01 Avg DV01 %Deviation

1 USSW2 2 2768000000 474617 779729.23 60.869464

2 USSW3 3 633000000 168557 405415.54 41.576354

4 USSW5 5 3104000000 1388505 1560210.18 88.994740

5 USSW7 7 891000000 551946 469480.20 117.565341

0 USSW10 10 3231600000 2758311 2894384.05 95.298722

3 USSW30 30 973000000 2013724 1785639.48 112.773268Creating a Dashboard

Next I will show you how to convert the above Dataframe into Tables and charts in a Dashboard in just a few lines of python code using the clarusui python library.

table = ui.Table(df, cssClass='table-inverse', headerColour='green') bar_chart = ui.BarChart(df, colFilter='DV01') line_chart = ui.LineChart(df, colFilter='Avg DV01') combo_chart = ui.ComboChart(bar_chart, line_chart, yaxis='Tenor', xaxis='DV01 Volume', title='DV01 and Average DV01 by Tenor') dashboard = ui.Dashboard(table, combo_chart, style=ui.DarkStyle(), header='IRS Volumes and DV01') print(dashboard)

All I do is pass in the dataframe (df) to the Table, Bar chart and Line chart.

To best display the relationship between the daily DV01 and Average DV01, I pass the Bar and Line chart to a Combo chart.

I then input the Table and Combo chart to my dark themed dashboard to get the below:

Hovering on the Bars and points in the Line chart displays the exact values at that point.

Once the dataframe was created, with a few lines of python code, all I had to do was pass it into the table and charts to get the above engaging Dashboard.

Try it Yourself

It is really easy for you to try the above examples yourself.

We provide Clarus python packages to make it convenient to call the Clarus API.

First you need to register for a free trial account here.

(Only for potential customers, no vendors please).

When you have been authorised, login and try out the examples above.

The Clarus API Reference Page allows you to try out the examples within a Browser Sandbox environment , before installing on your computer.

What could be easier?