Fannie Mae recently issued its first ever securities linked to SOFR (see here for details). The issuance was $6 billion in size, settled on 30 July with 6m, 12m and 18m tranches. So I wanted to update our recent SOFR Swaps Are Trading blog and see if this bond issue has led to any more activity in SOFR Swaps.

Recap of Week 1

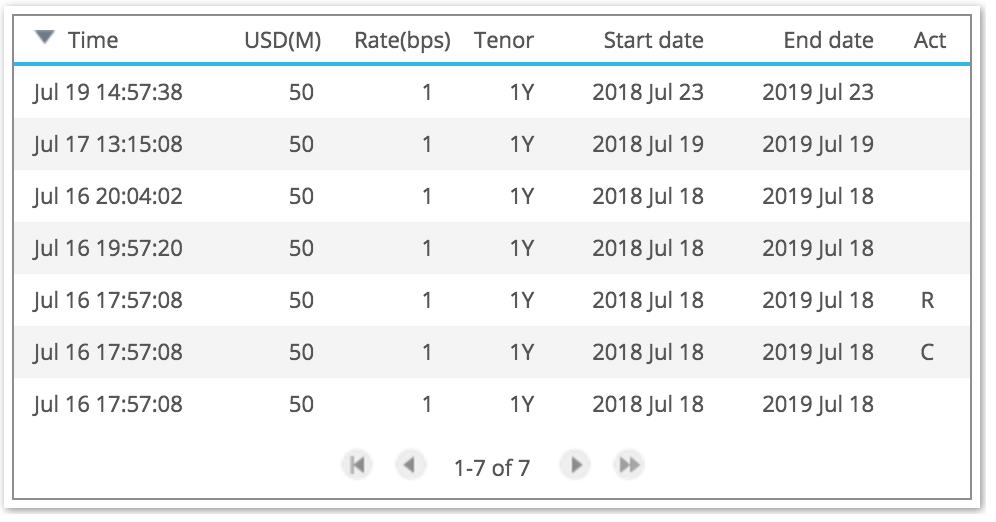

First a summary of the trades we reported in the week of 16th July:

Two of these seven rows are Cancel and Replace transactions, so we have five trades, each at $50 million, 1Y tenor and SOFR minus 1bps vs FedFunds, a cumulative total of $250 million.

All of these were executed On SEF and using SEFView, we can see that were done on TP-ICAP.

All were Cleared, which we think was at LCH SwapClear.

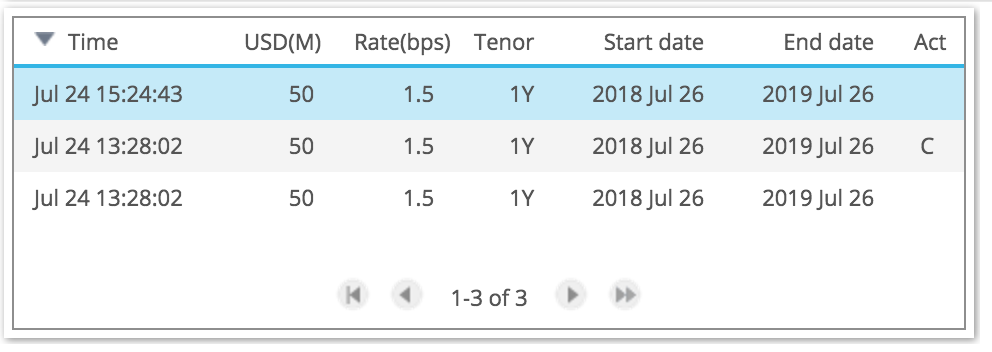

Week 2 – July 23, 2018

Lets move onto the second week.

This time we see three transactions, but the second cancels the first and then a new trade at 15:24 (London time or 10:24 New York), again $50 million and 1Y tenor, but this time at 1.5bps (not 1bps).

So not much of note there.

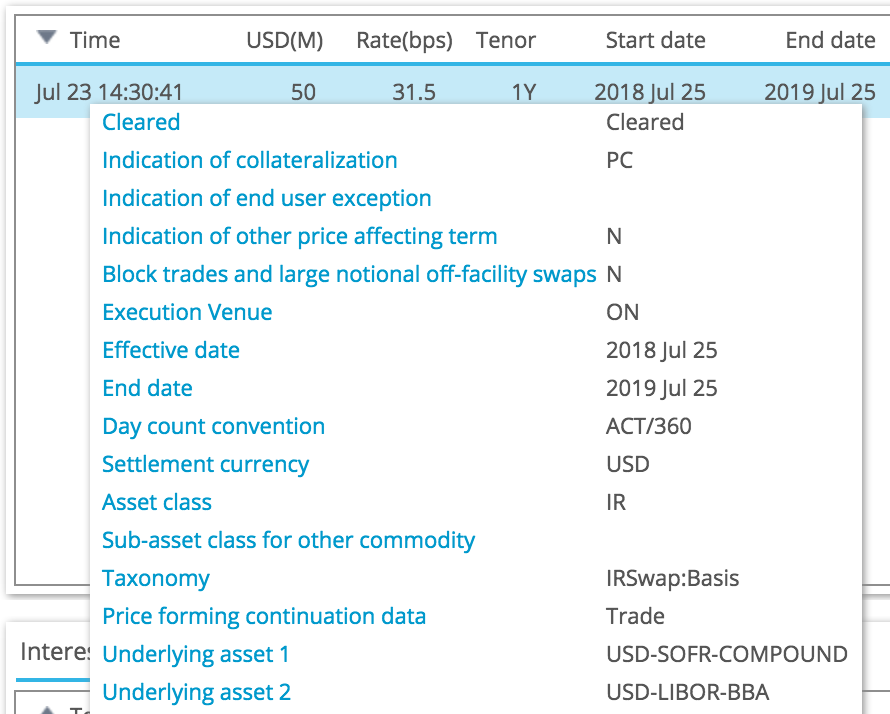

However there is another trade of note.

The first SOFR vs Libor Swap!

- $50 million notional

- 1 year tenor

- Spot starting

- SOFR daily compounded

- LIBOR 3M

- A rate of SOFR plus 31.5 bps

- Cleared, again we assume LCH

- On SEF, again on TP-ICAP (confirmed in SEFView)

This is good we definitely need to see basis spread trading between SOFR and Libor. How else are firms going to understand their risks as they start the transition away from Libor?

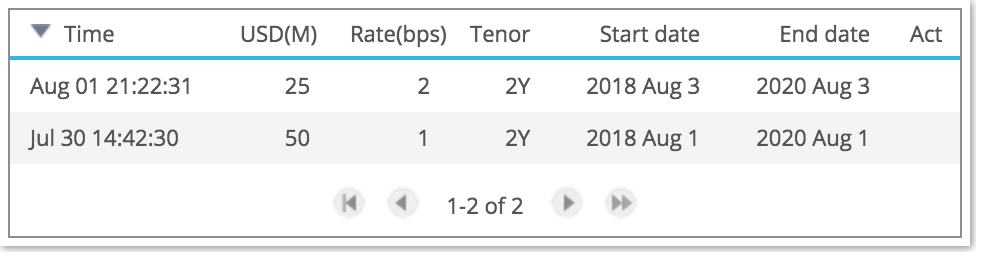

Week 3 – July 30, 2018

Onto week 3 and perhaps we will see some pickup related to the the Fannie Mae securities?

Unfortunately no pick-up in volume.

However we do see 2 trades and this time with 2Y tenor, as opposed to 1Y, the first at SOFR -1 bps, the second two days later at -2bps, but half the notional.

And there were no SOFR vs Libor Swaps.

Well that is a downer!

Anyway, early days and summer doldrums is a good time to test market infrastructure is ready.

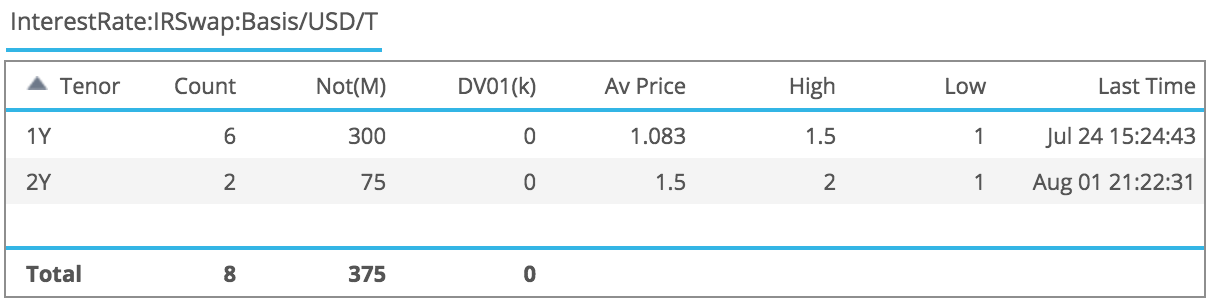

Recap of Weeks 1-3

A quick summary table of the Swap trades we have seen so far.

Eight trades in total with $375 million gross notional, six in 1Y and two in 2Y.

And the single trade, SOFR vs Libor we highlighted above in $50 million.

We are some way from an active market developing, let alone flow trading.

However with more issuance and a focus on the move from Libor to RFRs, we should see volumes picking up.

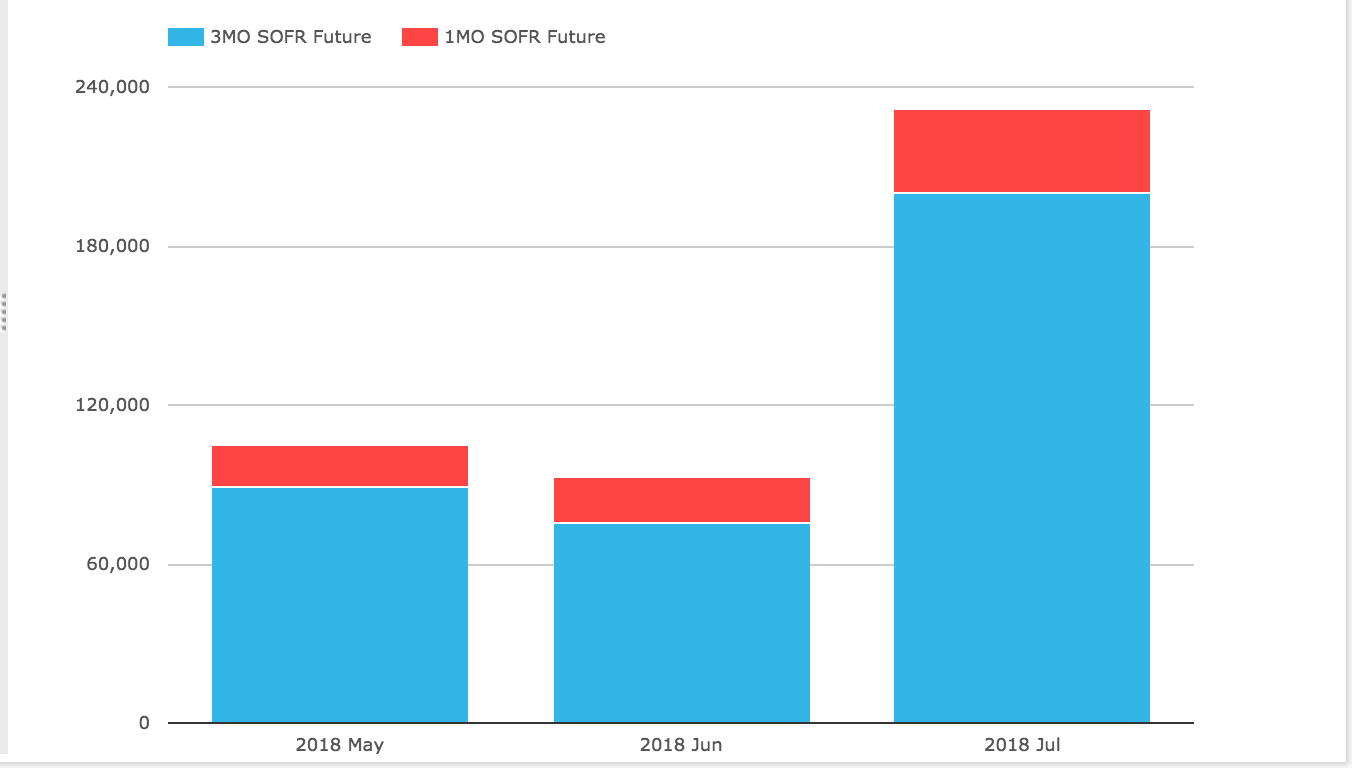

CME SOFR Futures

We only need to look at CME’s successful launch of its SOFR contracts, to see what is possible.

From SEFView, we see the start in May and volumes rising significantly in July, with the 3 month SOFR contract hitting $200 billion in notional equivalent in the month, lets call it an ADV of $10 billion.

Granted there is still a long way to go to get anywhere near the CME FedFunds future, let alone the mighty CME Eurodollar, but the early signs are promising and we know there is significant regulatory pressure to move away from Libor to SOFR.

The next few months will be interesting indeed.

Keep Updated

For SOFR Swaps, we have a neat “Alerts” feature that sends all SOFR trades straight to your email inbox. It’s the ideal way to stay on top of this new market:

Try it out for yourself via SDRView Pro (register for a free trial).

Try it out for yourself via SDRView Pro (register for a free trial).

Or stay informed by reading our blog (subscribe link below).

Why not simply keep a running chart of notional SOFR OI v FedFunds OI?

Good idea. A bit early to do this for Swaps given the low volume of SOFR.

For CME Futures, we have that chart in our CCPView product and will use in the next blog on SOFR volumes.