- Over $95bn in Fed Funds swaps have traded at negative rates.

- The lowest recorded rate so far was close to minus 7 basis points.

- Swaps all the way out to 3 year maturities have traded in negative territory.

- When does the market expect negative rates and how large will the cut be?

A GIFT!

On Tuesday 12th May 2020, Trump tweeted:

Looking at our data from US SDRs, the market was rather ahead of Trump here. Certain OIS swaps have been trading in negative territory since Thursday 7th May.

This bout of trading and advocacy for negative rates has recently led the Fed to rebuff the idea of negative rates:

Let’s see what the market thinks.

How Much Has Traded?

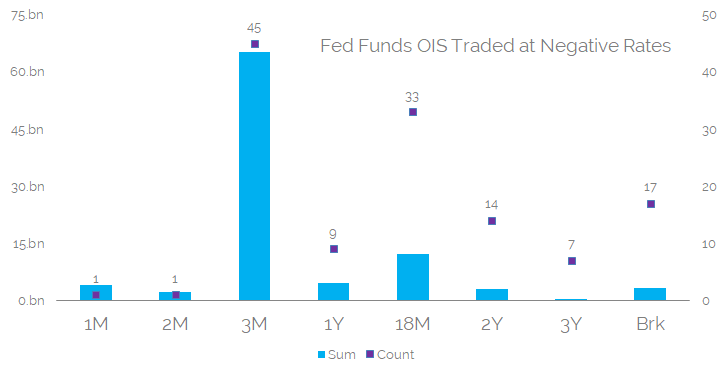

Looking at Fed Funds swaps traded since April, we’ve seen the following notional amounts trade in negative territory per tenor:

Showing;

- $95bn of notional in Fed Funds OIS has now traded at negative rates.

- This was across 127 trades in total.

- The shortest tenor was 1 month.

- The longest tenor was 3 years.

- The most active tenor was 3 months, as per most Fed Funds swaps.

The most telling thing for me is that due to the really flat curve, negative rates have extended out along the curve rapidly. 3 year swaps traded in negative territory! I guess this is a reflection of the European experience – once rates turn negative, they tend to stay there for a while.

When Are Rates Forecast to Go Negative?

Whilst we’ve seen 3 year swaps trade at sub-zero rates, it is not as if the whole curve before that point is in negative territory.

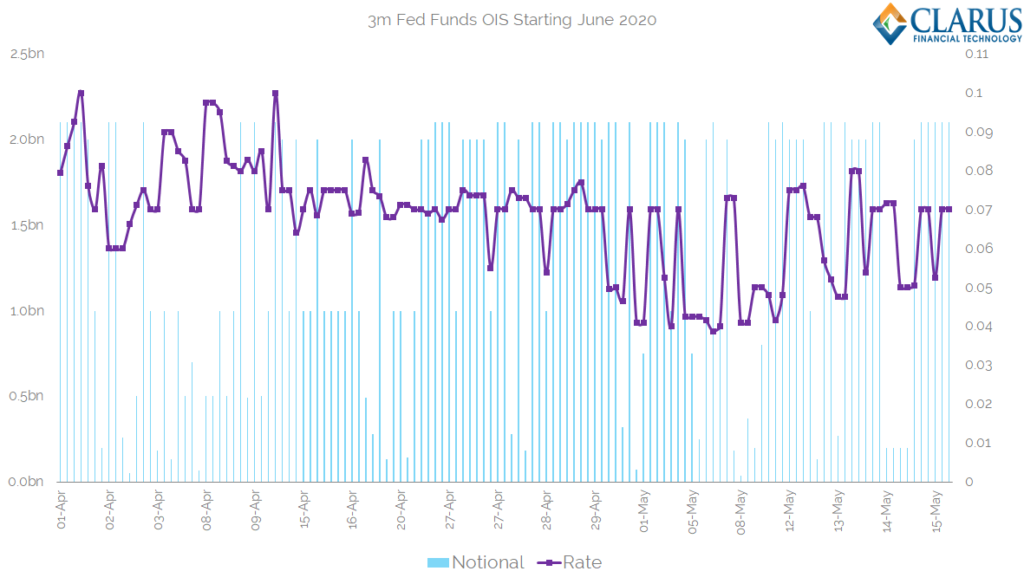

The most active Fed Funds forward, the June IMM dates (a 3 month swap starting 17th June 2020, ending 16th September 2020) has not traded at negative rates. This has only gone as low as positive 4 basis points:

Since the 7th May, when forwards further along the curve headed negative, the June 2020 contract has traded 33 times in positive territory, totaling at least $47bn (many trades at the short-end are capped at the block threshold).

Given that Fed Funds is already fixing at positive 5 basis points (right at the bottom of the range), the market isn’t expecting any cuts from the Fed until at least September.

Looking at the schedule of meetings, that means there are potentially three meetings in play during 2020. September, November and December.

When does the market think negative rates may come to fruition?

March 2021

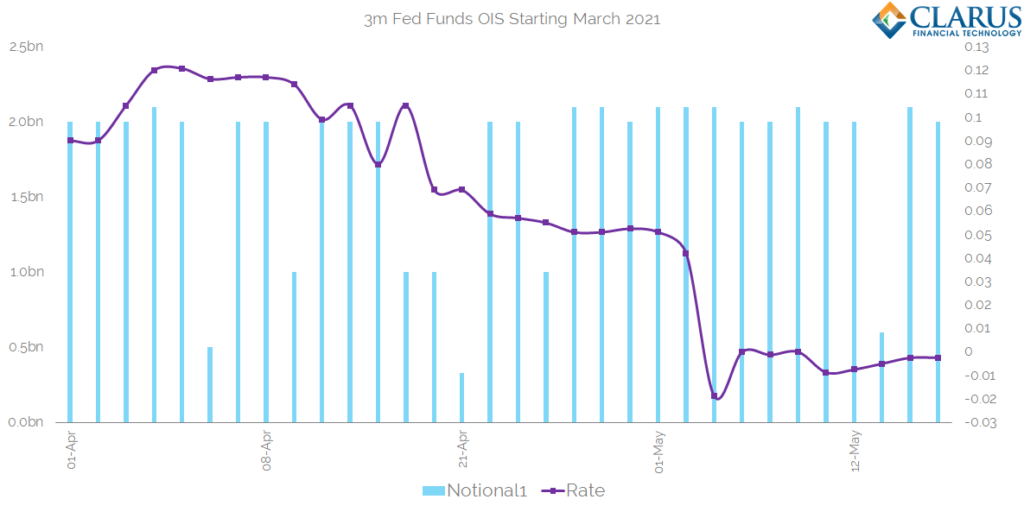

Looking at historic pricing, the first OIS swap that traded in negative territory was the 3 month March 2021 IMM contract, starting 17th March, expiring 16th June 2021:

Showing;

- Mar21 traded at -1.875 basis points on 7th May at 16:27 CET.

- It has since remained largely in negative territory, trading only twice at the heady heights of zero since then.

- That first negative print was the low of the contract so far, with most prints occurring between -0.75 and -0.25 basis points.

- A total of $17bn (at least, most are above block) notional has traded in the Mar21 contract at rates of zero or below.

So are we nailed on for a March 2021 cut?

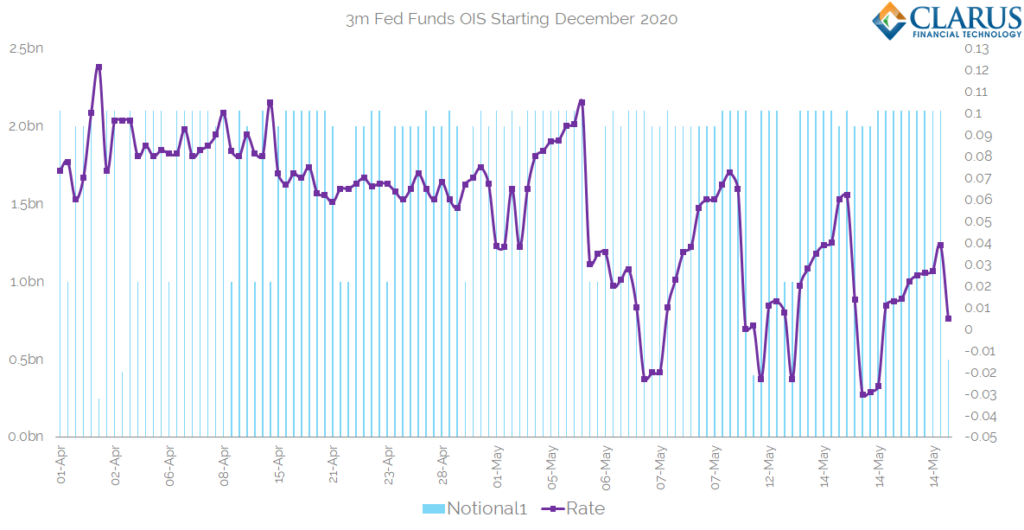

December 2020

Not so fast there. The December 2020 contract has also traded in negative territory:

Showing;

- Dec20 was later to the negative party than it’s Mar21 cousin. It first traded below zero about one hour after the March contract on May 7th.

- Since then, a lot more trading activity, and a lot more volatility, has been seen on the Dec20 contract.

- Prices quickly rebounded above 7 basis points, before again see-sawing negative.

- The low was minus three basis points.

- The (capped) notional amount that has traded at zero or below is comparable to Mar21 – $17.4bn.

- But the number and total amount of trading since May 7th has been much larger in Dec20. Over $75bn has traded since May 7th – most of it at positive rates.

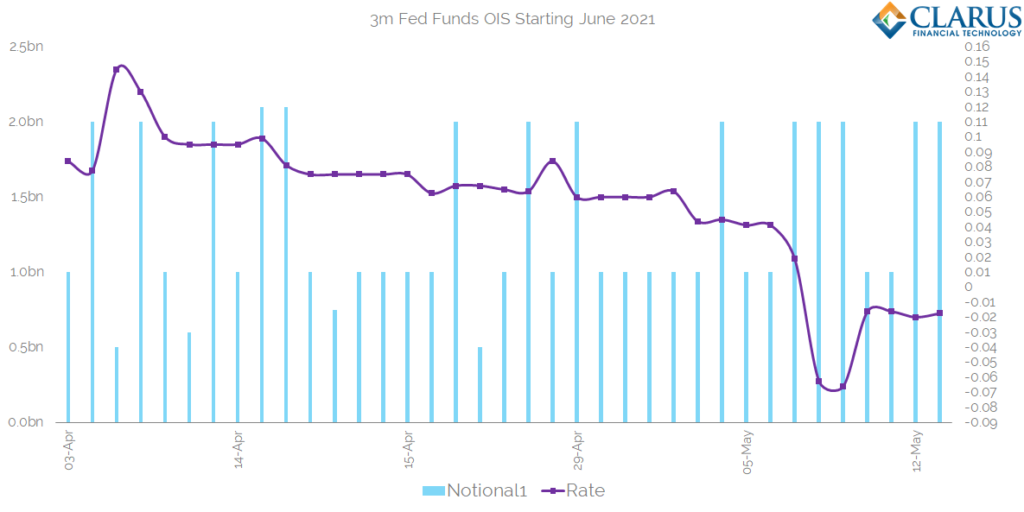

June 2021

Marking the low-point in Fed Funds 3 month swaps, we saw a minus 6.625 basis point print in the June 2021 contract on 8th May:

It looks like liquidity wasn’t at its best for this contract. It traded below minus 6 basis points twice, and then didn’t trade again until after the weekend, when it bounced all the way back to minus 1.625 basis points.

Current Market – FOMC Watch

Based on current market pricing for FOMC-dated OIS, we see the following probability of cuts per meeting:

Showing;

- The overriding consensus is that a 25 basis point cut isn’t coming any time soon.

- The fourth Fed meeting, scheduled for November 4-5 2020, only carries a small chance of a cut in rates.

Motivations for Trading Negative Rates

Having looked at the trading activity, the executed rates have been only marginally negative. We are not seeing any trading that fully prices in a 25 basis point cut into negative rates. We’ve looked along the curve and it doesn’t turn deeply negative at any point. It looks to be very flat in the short-end.

Conclusions?

- The market may think the first foray into negative rates for the Fed would be a 5 or 10 basis point cut from here, to a target rate of 0 to minus 10 bp.

- Contracts may only have gone negative due to stop loss activity.

- Hedging of tail risks related to negative rates in other products may have led to severe enough receiving pressure at the short-end to push rates negative (without any speculative pressure for negative rates as an actual outcome).

This FT report may confirm the third point above.

Recall that this first happened in Euro markets back in 2012/2013 when it became apparent that EUR rates could very easily turn negative. The ECB did cut rates into negative territory in June 2014, but the EONIA overnight fixing didn’t turn negative until later on, first in August and then consistently in September 2014.

Much of the related EUR hedging was due to CSAs carrying zero floors. Is the same true in the USD market? Were zero-struck floors in USD allowed to expire once the Fed started a sustained hiking cycle in 2017?

Final Thoughts

The shape of the curve doesn’t suggest that the market expects or is pricing in deep cuts into negative territory. However, it is not just individual contracts or forwards that have headed negative.

A total of $7.6bn in notional has traded in longer-term Fed Funds OIS, from 1Y out to 2Y, all at negative rates. 15th May saw the lowest of these contracts trading, at -3.25bp for 1Y.

3Y Fed Funds swaps also traded at negative levels as recently as 14th May. This long-term activity is more consistent with CSA hedging of zero floors.

Either way, any experiment with negative rates is unlikely to be over quickly.

Hi , It would be great to get your take on how Negative rates will affect Credit Risk. Matt