Today, we look at three recent start-ups or new products introduced by derivatives exchanges and clearinghouses (CCPs).

Key takeaways:

- FMX started executing SOFR futures at LCH in September 2024, executing $750 billion notional in Q3 2025.

- SGX began executing and clearing JPY TONA money market futures in July 2024, executing $86.4 billion in Q3 2025.

- LCH SwapClear introduced MYR NDIRS in April 2025, clearing $128 billion in Q3 2025.

All the charts, data, and statistics in this blog were sourced from CCPView.

FMX rates futures

FMX is a fixed income e-trading platform focused on US Treasury bonds, FX, and repo owned by BGC. Recently, FMX launched the FMX Futures Exchange with strategic investments from seven large investment banks and three non-bank trading firms.

FMX Futures executes USD rates futures cleared at LCH, and has so far launched:

- In September 2024, three-month SOFR futures with nine quarterly expiry dates

- In May 2025, two- and five-year T-Note futures with three quarterly expiry dates each.

FMX’s website emphasizes margin relief and lower-risk basis trading.

- Margin relief comes from cross-margining against cleared swaps at LCH. The most obvious opportunity would be the natural offsets between short-end SOFR OIS with maturity dates close to the nine SOFR futures expiry dates.

- Lower risk basis trading comes from collocated FMX cash platform and futures exchange matching engines. This delivers low latency and therefore lower “legging risk” – the risk of only one side of the T-Note future and cash UST trade package executing.

The volumes to date are cited below.

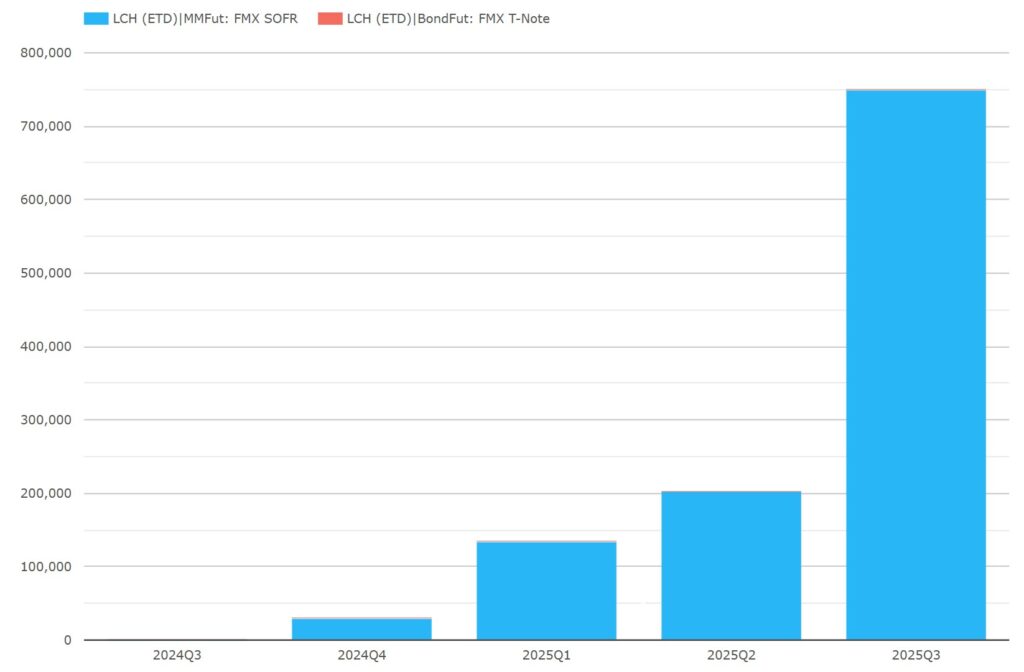

Chart 1: LCH USD rates ETD volumes by product type (notional USD millions). Source: CCPView.

Chart 1 shows the progress of FMX / LCH USD rates exchange-traded derivatives (ETD) volumes in 2024 and 2025.

- In 2024, SOFR futures started trading in September, and saw $28.9 billion notional cleared in Q3.

- In 2025, SOFR futures accelerated reaching totals of $133 billion in Q1, $203 billion in Q2, and $750 billion in Q3.

- In 2025, T-Note futures (invisible at this notional scale) started trading in May and reached $80 million in Q3.

Putting aside bond and FedFunds futures and options on futures, we now look solely at SOFR futures market shares by selecting relevant product subtypes. Rather than snipping and pasting from CCPView directly, I downloaded the percentages to adjust the numerical precision for visibility.

Table 1: USD SOFR futures CCP share (percentage of notional). Source: CCPView.

Table 1 shows that CME has dominated SOFR futures volumes.

- After dominating Eurodollar (USD LIBOR) futures, CME has had competition from ICE Europe for SOFR futures liquidity – staying above 70 percent each year from launch in 2018 until 2021. After LIBOR cessation, CME reasserted its dominance – reaching a SOFR futures share of above 99.99 percent by the end of 2024 (highlighted in blue).

- FMX and LCH first executed and cleared SOFR futures in September 2024, reaching a SOFR futures share of 0.11 percent for the first three quarters of 2025 (highlighted in green), and taking over 0.3 percent in September 2025.

FMX Futures Exchange has made a promising start.

SGX TONA futures

SGX has launched and reached a material market share of JPY TONA money market futures. As noted in our recent JPY rates update, SGX reached 22 percent of Q2 TONA volumes.

We put this in a bit more context by letting quarterly volumes tell the longer-range story.

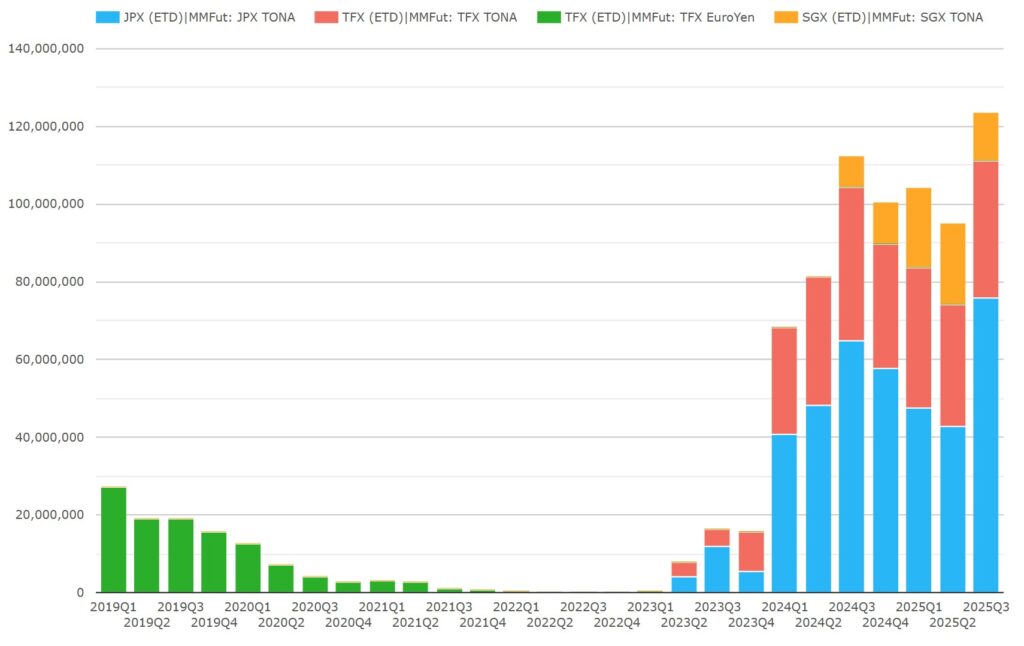

Chart 2a: JPY TONA futures volumes (notional JPY million). Source: CCPView.

Charts 2a shows that:

- TMX Euroyen futures (which only began trading in Q1 2018) had fallen out of use by most participants by the end of 2020 – a year before JPY LIBOR cessation at the end of 2021.

- After not having TONA futures at all, the competing products from both TMX and JPX launched a year after LIBOR cessation in Q1 2023. They then jumped to ¥68.2 trillion across both exchanges in Q1 2024.

- SGX launched its TONA futures in Q3 2024, reaching ¥20.9 trillion ($143 billion) in Q2 2025, its largest quarter to date, and ¥12.6 trillion ($86.4 billion) in Q3 2025.

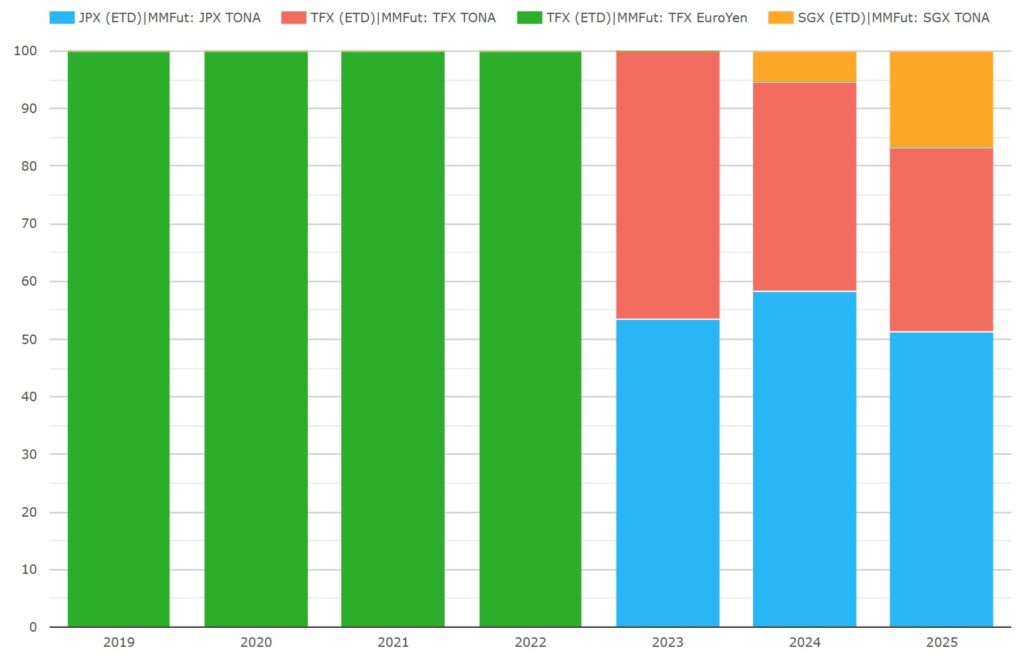

We now look at market share by year. Note: 2025 is only for the first three quarters.

Chart 2b: TONA futures CCP share (notional percentage). Source: CCPView.

Charts 2b shows that:

- Initially, JPX and TFX split the market evenly in 2023.

- SGX achieved a 5.3 percent share in 2024, despite only launching in July.

- In 2025 to the end of September, SGX had a 16.8 percent share at the expense of reductions in the shares of JPY and TFX.

- In 2025 to the end of September, SGX’s share was largest in April with a 32 percent share, mostly at the expense of TFX, whose share was 32 percent.

In the TONA futures market, SGX has made market share inroads of a size and at a speed rarely seen in any ETD market.

SwapClear MYR swaps

As noted in our recent quarterly cleared rates swaps blog for Q2 and Q3, LCH SwapClear recently introduced clearing of Malaysian Ringgit (MYR) swaps. As MYR is a non-deliverable currency, these are in fact non-deliverable interest rate swaps (NDIRS), meaning they settle in USD rather than MYR. This is the first time MYR swaps have cleared, as no other CCP previously cleared them.

Volumes were meaningful from the first month – April 2025 – allowing a single chart to show them visibly in the context of all NDIRS.

Chart 3a: Cleared non-deliverable IRS new trade volumes (notional USD million). Source: CCPView.

Chart 3a shows that:

- MYR NDIRS (in dark blue) first cleared in April 2025, with volumes of $14.2 billion.

- MYR NDIRS cleared $62.5 billion in September 2025, and $128 billion in Q3 2025.

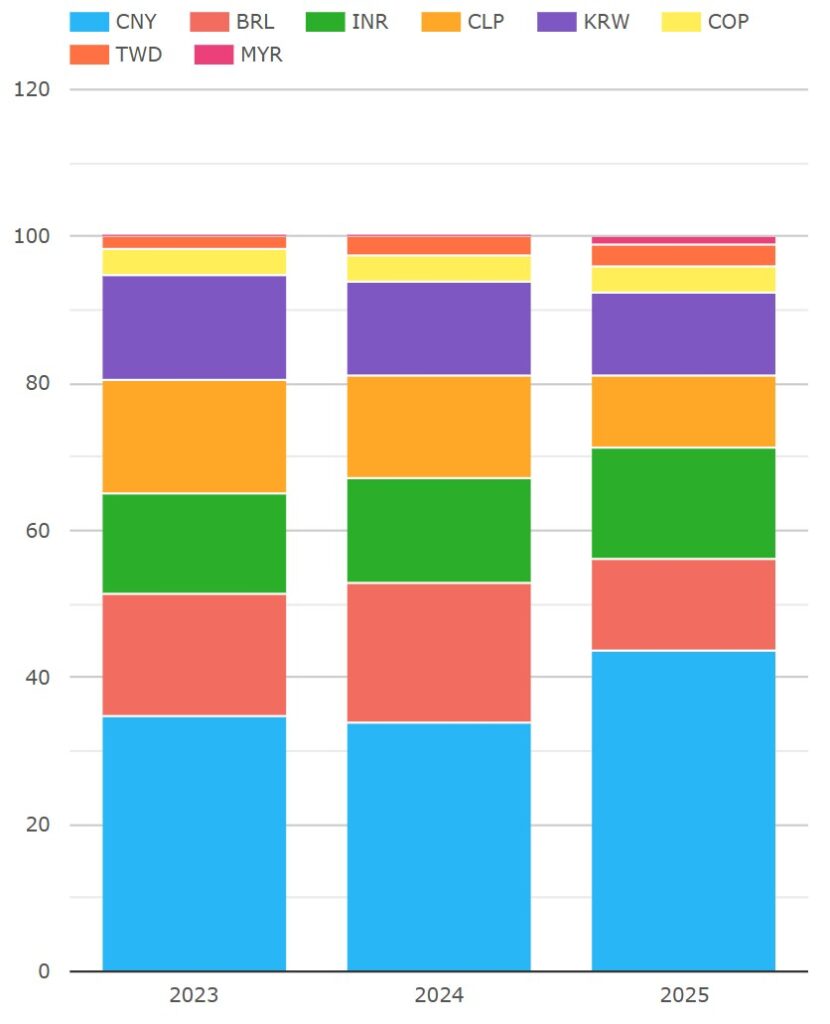

Now, we look at NDIRS currency market share by year, including 2025 up to the end of September.

Chart 3b: Cleared NDIRS share1 by currency. Source: CCPView.

Chart 3c: Cleared NDIRS CCP share (percentage of NDIRS $ trade notional). Source: CCPView.

In 2025 to the end of September, charts 3b and 3c show that:

- MYR (in magenta) had a 1.0 percent share, despite their April start.

- MYR contributed to LCH SwapClear maintaining a leading market share at 40.6 percent, flat YoY, offsetting a 1 percent loss for other currencies combined.

- Shanghai increased its share YoY by 9.6 percent, driven by the relative increase in CNY volumes.

- CME’s share decreased by 10.1 percent YoY, driven by the relative decrease in BRL, CLP, and COP volumes.

Full-year 2025 market shares will tell us more, but SwapClear MYR NDIRS have already had a meaningful impact on NDIRS market shares.

That’s it

Skip back to the top to reread the key takeaways if you like.

In future, we will track progress on the innovations above in our quarterly volumes blogs, and post on other innovations as they crop up.

You can run charts and download statistics on a lot more asset classes and product types in CCPView. Click the link to see a summary of what is available.

Contact us if you are interested in a subscription.