I wanted to follow up on two of our 2022 blogs to estimate the impact on overall volumes in GBP, JPY and CHF markets of LIBOR cessation (which was only 7 months ago, believe it or not!).

All of the data in this blog is taken from CCPView, and looks at the impact of LIBOR cessation on trading volumes in Interest Rate Derivatives alone.

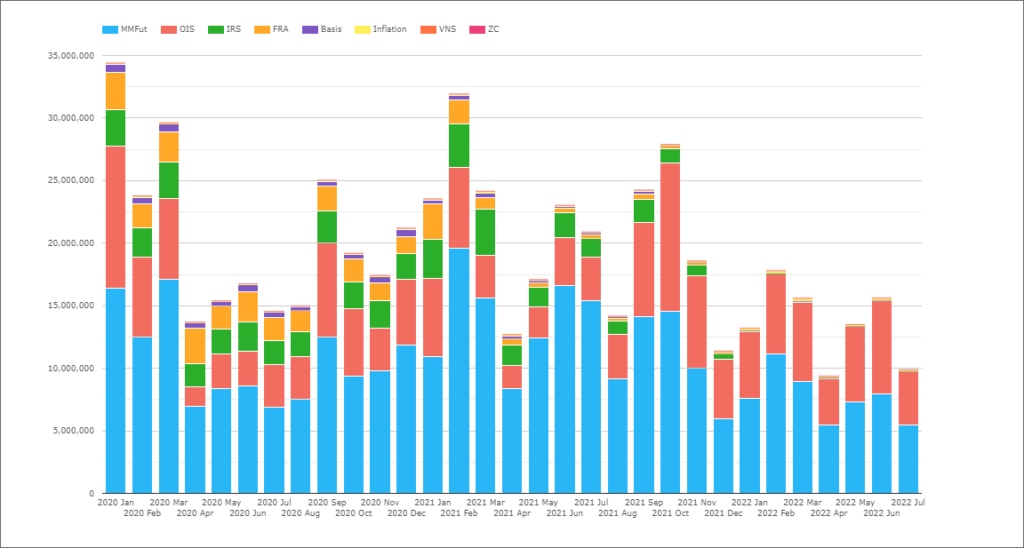

Overall Volumes

Taking a look at total volumes in Rates products in these 3 currencies shows that overall volumes are now lower in the post-LIBOR world:

Showing;

- Monthly volumes of all Rates products in GBP, JPY and CHF since January 2020. Volumes are shown in notional equivalents (millions of USD).

- This covers Short Term Interest Rate futures (STIR Futures contracts), IRS, FRAs, OIS, Basis Swaps, Inflation, Zero Coupon swaps….quite a list!

- As we have previously noted, IRS have disappeared from our data, and are now replaced with OIS.

- There are no FRAs.

- The only basis swaps still trading in GBP, JPY and CHF are in JPY TIBOR. These are trading both vs other tenors of TIBOR (3s6s basis) and versus the RFR (TONAR).

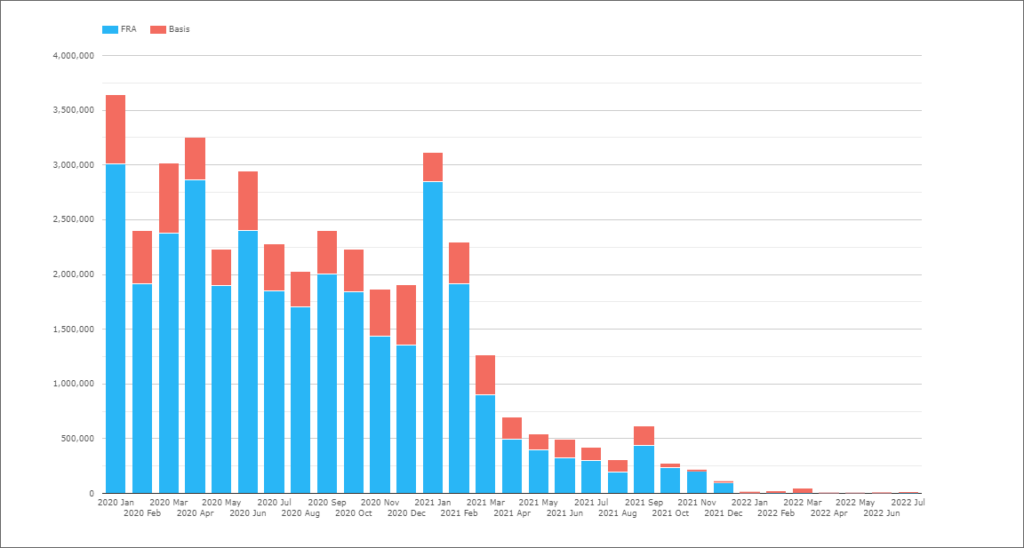

Disappearing Products

To quantify the reduction in volumes, let’s first look at the absolute loss that results from the following products no longer trading:

- FRAs

- Basis Swaps

Showing;

- Notional volumes of all FRAs and Basis swaps traded in GBP, JPY and CHF.

- In 2020, average monthly volumes in these products were over $2.5Trn.

- This was made up of ~$2Trn in FRAs, which are mainly short-term products, and ~$0.5Trn in Basis Swaps (longer term).

- In 2021, after the ISDA spreads had already been locked in and the CCPs conversion plans to RFR + spreads were well understood, these volumes reduced drastically.

- Average monthly volumes of FRAs in 2021 were just $0.7Trn, a reduction of 66%.

- Basis swap activity reduced by an almost identical proportion, a 64% reduction to $168bn per month.

This amount likely understates the reduction in OTC volumes because:

- JPY FRAs do not trade. They have always traded as Single Period Swaps, therefore show up as IRS volumes in CCP reports.

- With central banks in play this year, it could have been a stellar period for volumes in short-dated products, and in particular for FRA matching services. I am sure they’ve done well in USD anyway, but what might have been in GBP and CHF….

Anyway, let’s carry forward our $2.5Trn in lost volumes so far and take it as a starting point.

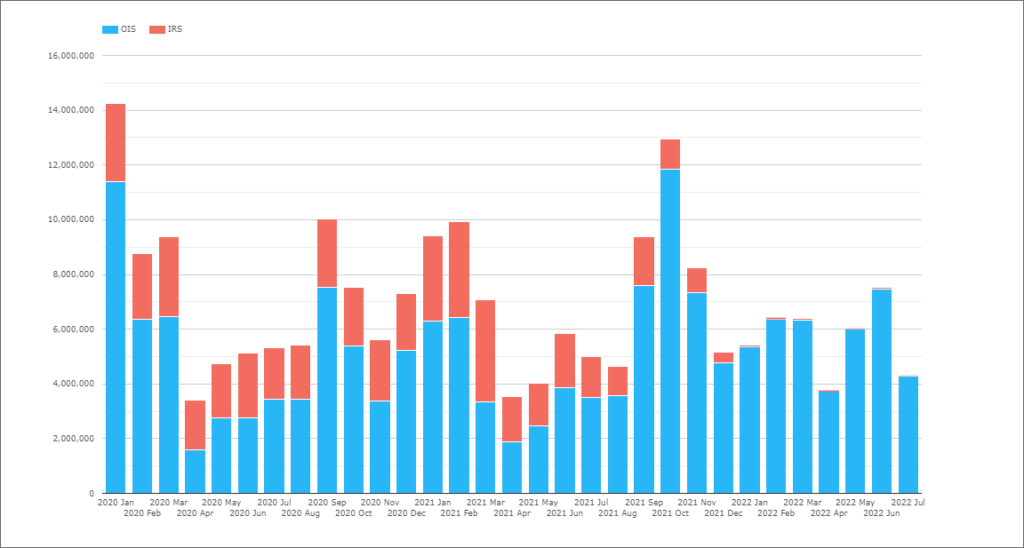

Reduced OTC Activity

We have obviously seen a great increase in OIS activity as RFRs are now the standard product to trade. However, have OIS products fully stepped into the shoes of previously traded IRS markets? Let’s look at the data:

This chart doesn’t look so bad! Let’s look at the data;

- Notional volumes of all IRS and OIS swaps traded in GBP, JPY and CHF.

- In 2020, average monthly volumes in these products were over $7.2Trn, much larger than in Basis Swaps and FRAs.

- RFR transition began in earnest in 2021 for these currencies.

- In 2021, average monthly volumes in these products was almost identical at $7.1Trn.

- Now, in 2022, post LIBOR cessation, OIS volumes have grown somewhat compared to OIS volumes last year, but have not completely replaced IRS volumes.

- In 2022, average monthly volumes are now at $5.7Trn.

We therefore see a total reduction of ~$1.5Trn in monthly volumes since 2020.

Adding that to the previous $2.5Trn reduction leaves us with a nice round $4Trn reduction in monthly volumes so far. And this is just in OTC products.

Let’s now turn to futures.

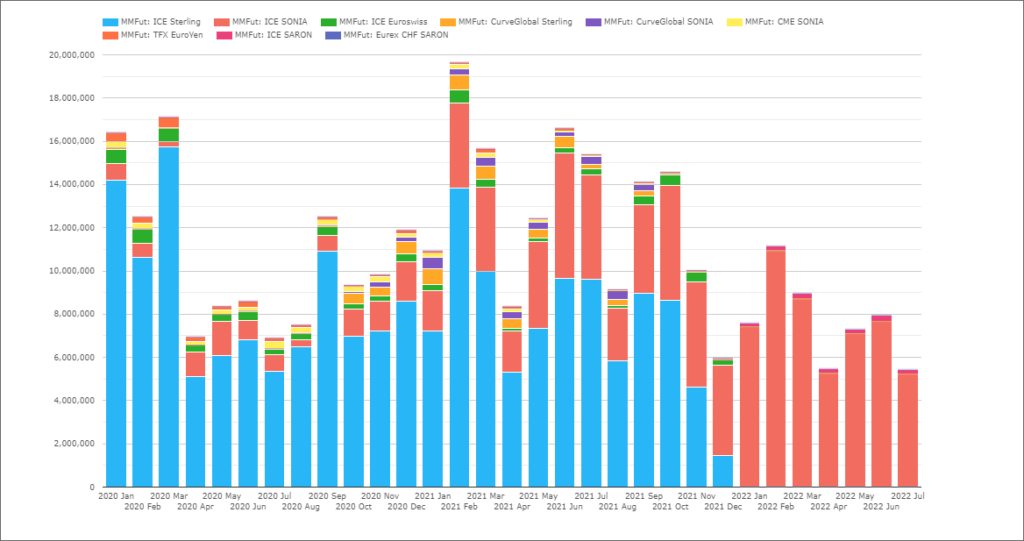

STIRs

Money market futures have likewise moved from LIBOR to RFR-based contracts. How have volumes help up?

Showing;

- Notional volumes of all STIR contracts traded across GBP, JPY and CHF futures products. As we know, GBP was a competitive landscape, so there were a lot of competing contracts out there!

- In 2020, average monthly volumes in these products were over $10.6Trn, much larger again than IRS and OIS OTC volumes.

- In 2021, these volumes increased significantly, to over $12.7Trn.

- Now in 2022, volumes have reduced to $7.7Trn.

Even with Central Banks so active in this space, LIBOR cessation has significantly reduced volumes. Let’s call this one a 34% reduction (the average of 2020 and 2021 given that volumes increased significantly), meaning another $4Trn reduction in activity.

Our running total now stands at $8Trn reduction in activity from LIBOR cessation.

And yet…

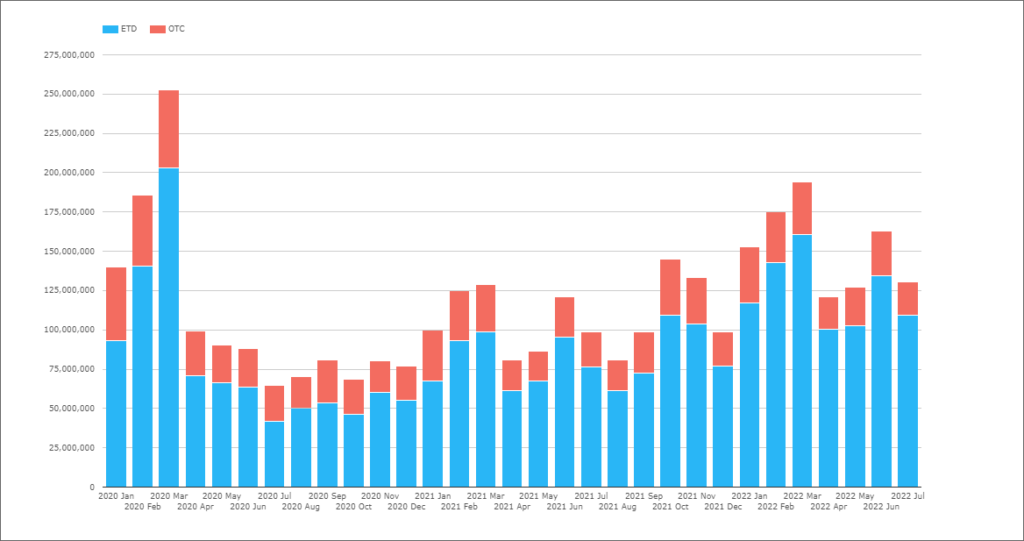

And yet…one LIBOR currency has laboured on! One LIBOR currency still remains…and it really is the daddy of them all. If we run the same data, but including USD:

Showing;

- Monthly volumes of all Rates products in GBP, JPY, CHF and USD since January 2020. Volumes are shown in notional equivalents (millions of USD).

- This covers Short Term Interest Rate futures (STIR Futures contracts), IRS, FRAs, OIS, Basis Swaps, Inflation, Zero Coupon swaps….but this time split into simply “OTC” and “ETD (futures)” asset classes.

- Including USD really changes the story, although the impacts are quite different between OTC (“swaps”) and ETD (“futures”).

- In OTC, average monthly volumes in 2020 were $28Trn. In 2021, this reduced by ~8% to $25.6Trn.

- In 2022, these average monthly volumes in OTC have increased to above $28Trn.

- OTC volumes are therefore ~5% higher, resulting in an additional $1.34Trn in monthly volumes.

- Obviously, this is all driven by increased USD volumes, given we know that other currencies reduced by ~$4Trn over the same time-period.

However, it could be argued that these OTC volumes are really just a rounding error compared to the explosion in Futures trading activity we’ve seen, as a result of increased SOFR adoption in USD futures markets.

- Monthly volumes of STIRS in 2020 were $73Trn.

- In 2021, this increased to $83Trn.

- In 2022, this now stands at $124Trn!

You can forget all about a measly $8Trn in reduction from GBP, CHF and JPY activity when USD are adding $45Trn a month in activity…

In Summary

- There has been an $8Trn reduction in monthly notional activity in interest rate derivatives as a result of the cessation of GBP, JPY and CHF LIBORs.

- This reduction in activity has been evenly split between OTC and ETD products.

- However, this reduction in activity has been dwarfed by the explosion in USD trading activity.

- Particularly in ETDs (futures), USD Rates trading activity is flourishing.

- How much of this volume will be sustainable after June 2023, the final cessation date of USD LIBOR?

- Follow our data to find out. Contact us for a CCPView subscription.