ESMA just published the results of its EU-Wide CCP Stress Test, the aim being to assess the resilience and safety of the European CCP sector and to identify possible vulnerabilities. Given that CCPs are conservative organisations, it is no surprise to learn that “EU CCPs can overall be assessed as resilient to the stress scenarios used to model extreme but plausible market developments”. I think that is a pass.

The published results show very interesting data, which I will highlight below. (Full results can be found here).

Background

ESMA conducted the tests for 17 European CCPs by asking each CCP to submit data for three dates in 2014; October, November, December.

A bottom-up approach of asking CCPs to supply the results and the risk factor shocks from their own daily Stress tests was combined with a top-down approach of building a common list of minimum price shocks for risk factors using both historical data and input from the European Systemic Risk Board (ESRB).

Where a CCP’s risk factor shocks did not meet ESMA’s minimum price shocks, CCPs were asked to provide updated results or justification for the level of price shock applied within a specific scenario.

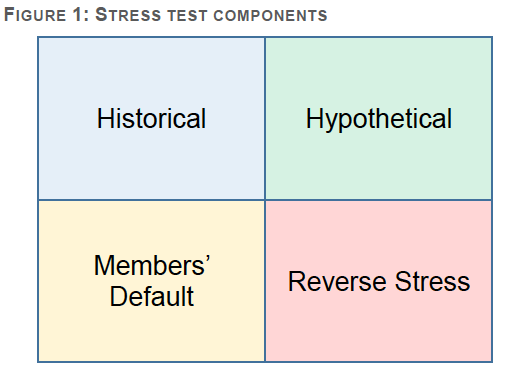

The Stress tests components are shown in the following picture from the published results.

Member Default scenarios specify that for each CCP the two members with the highest exposure were assumed to default; meaning that an individual CCP could face more than two defaults (up to a theoretical limit of 34, as 17 * 2, but in reality less).

Three scenarios, MD-A, MD-B, MD-C specify the default of two clearing members with the highest exposure, two corporate groups with the highest exposure and two corporate groups with the highest default probability weighted exposure.

As well as applying Member Default Scenarios, CCPs were asked to apply a number of Historical and Hypothetical risk factor shocks to the positions held.

And in addition Reverse Stress tests were created to determine the number of entities that would need to default to exhaust pre-funded and committed default resources.

Lets look at some of the results from the document.

Aggregate Default Funds

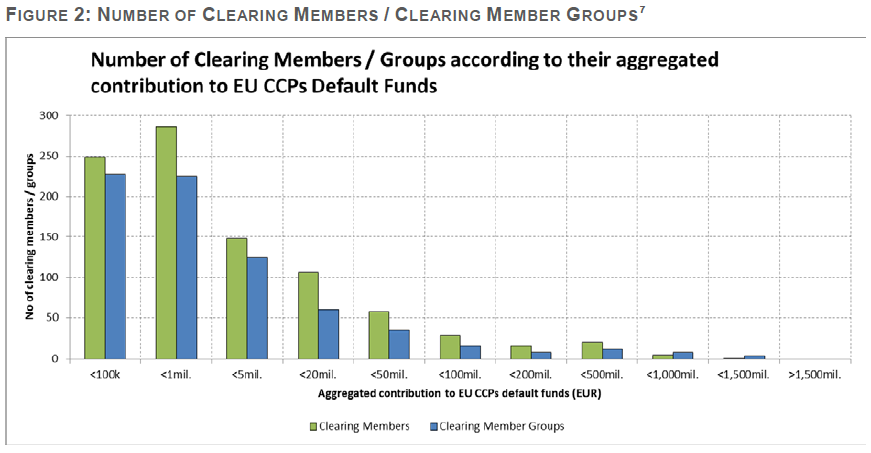

Starting with some charts to set the scene.

Showing:

- More than 900 entities as members of one or more CCPs

- (85% of these were only members at one CCP, while 11 entities were members at 10 or more CCPs)

- 60% of members have an aggregate contribution of < €1m and 95% < €100m

- 4 groups have a total contribution of more than €1billion each, the largest being €1.2b

- The 5% of members with > €100m, provide 70% of the mutualised resources across all CCPs

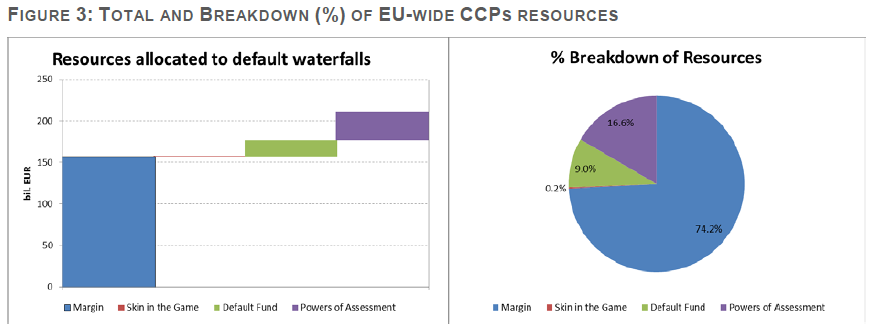

Showing:

- Margin at €150 billion represents the largest component (74%) of total aggregate resources

- Powers of Assessment (or Committed Resources) is next at 16.6%

- Default Fund (or Pre-funded Member Contributions) are 9%

- CCP’s resources are 0.2%

Interconnectedness and Concentration

Showing:

- CCPs, with the size of the yellow circles proportional to the size of the Default Fund (LCH UK is the largest)

- The Top 10 Clearing Member Groups (blue circles), which provide @ 50% of EU-wide Member Contributions

- The thickness of the line between a CCP and a Clearing Member Group is proportional to the sum of the contributions of all members belonging to this group to the default fund(s) of the CCP.

And as per the ESMA write-up “It can be seen that the top-10 groups are connected to all larger CCPs, but also to some of the smaller CCPs. These groups always have one or more entities that are members in the largest CCPs being also amongst the top default fund contributors. Even for this reduced scope, it can be expected that a default of one of the top groups would trigger a simultaneous default of one or more entities in most of the European CCPs with potentially systemic implications. Therefore, the default of the top-2 EU-wide groups is one of the member default scenarios considered in the stress exercise”.

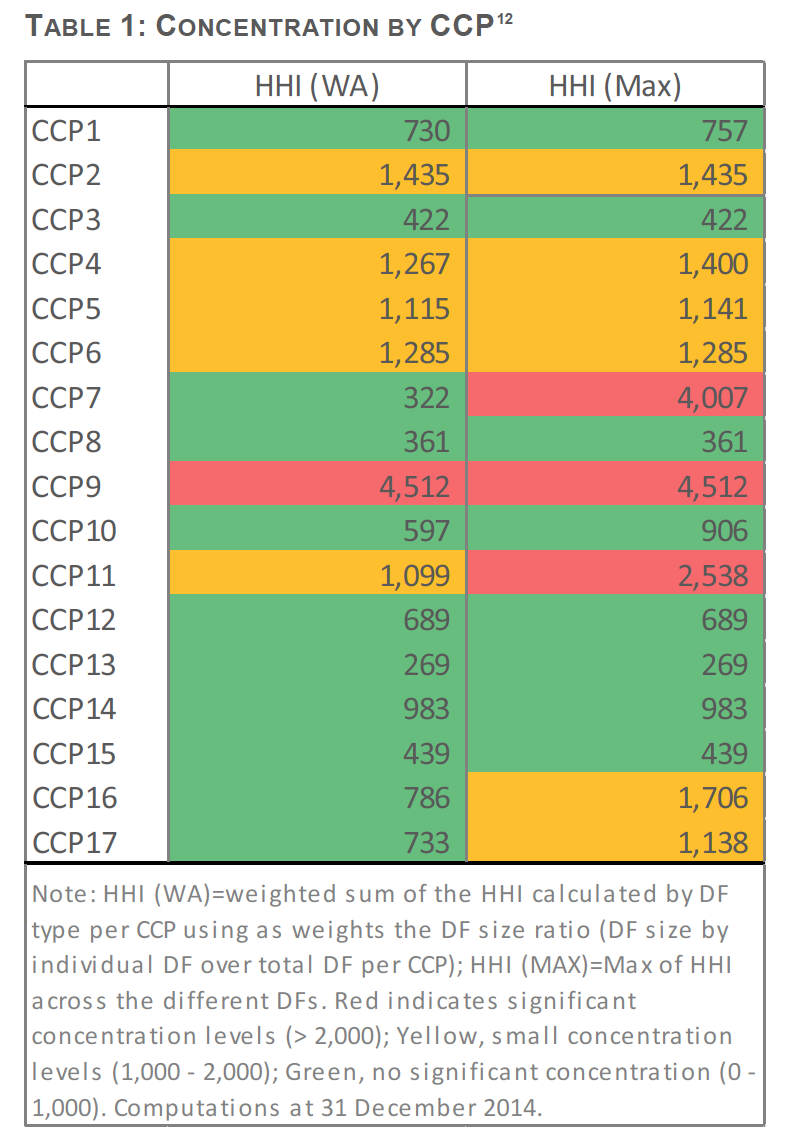

Next concentration of members by CCP.

With the ESMA explanation, “In the (HHIWA) case there is only one CCP showing high levels of concentration (red) because of the small number of clearing members. The overall exposure is from a systemic perspective limited and the small number of members is not expected to give rise to systemic risk. Five CCPs result to be moderately concentrated (yellow). For all five CCPs, however, the concentration level is only slightly above the lower threshold.”

Some interesting charts indeed, now onto the stress test results themselves.

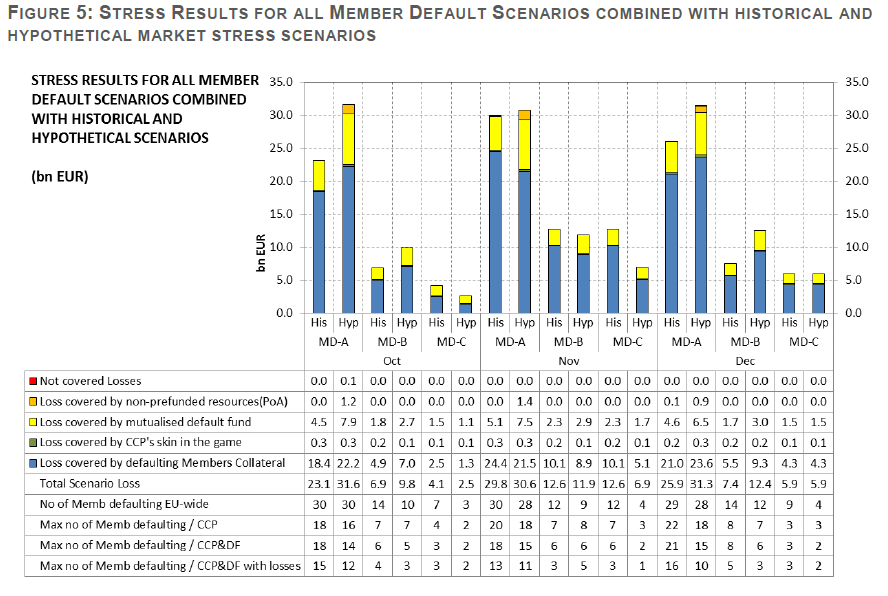

Sufficiency of Financial Resources

The absence of red shows that there are no losses not covered by financial resources, while the small amount of orange shows that non-prefunded resources are only used in small amounts. Meaning that losses are covered by pre-funded default fund contributions and the defaulting members margin.

It is interesting to examine the largest scenario; MD-A Hypothetical for October, this shows:

- Members Defaulting EU-Wide is 30

- Max number of members defaulting per CCP DF is 14

- Total Scenario Loss of €31.6 billion

- Loss covered by the defaulting members collateral is €22.2b

- Loss covered by CCP is €0.3b

- Loss covered by pre-funded Default fund is €7.9b

- Loss covered by non-prefunded resources is €1.2b

- Not covered losses is €0.1b

You get the picture. Thirty members defaulting EU-Wide is a severe stress test indeed.

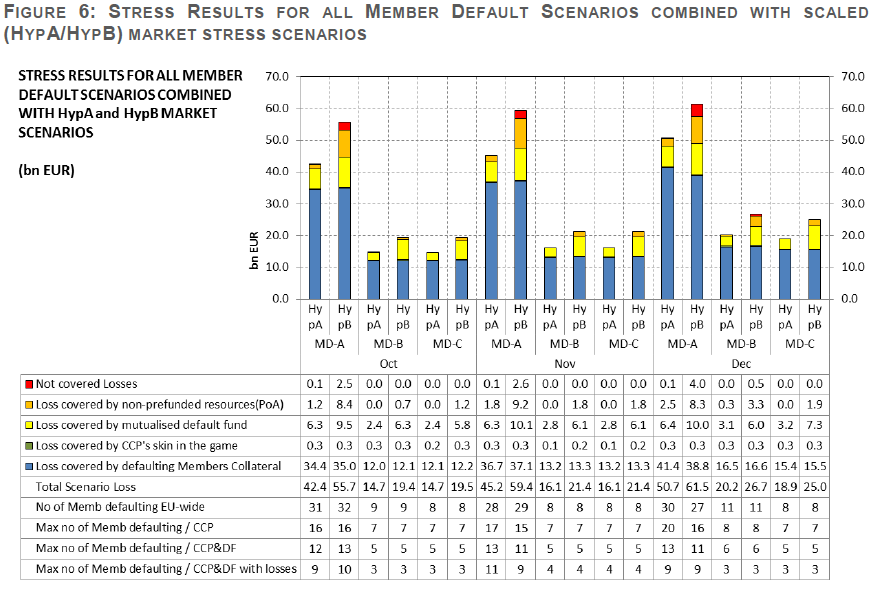

The results for the Hypothetical market shocks are even more severe.

This time the greatest not covered loss is MD-A HypB in December with €4 billion out of a Total Scenario Loss of €61.5 billion.

More charts and explanation for sufficiency of financial resources are to be found in the 67 page ESMA results document, so for those of you interested, you can get that that here.

Moving swiftly on and skipping the Clearing Member Knock-On Effects section.

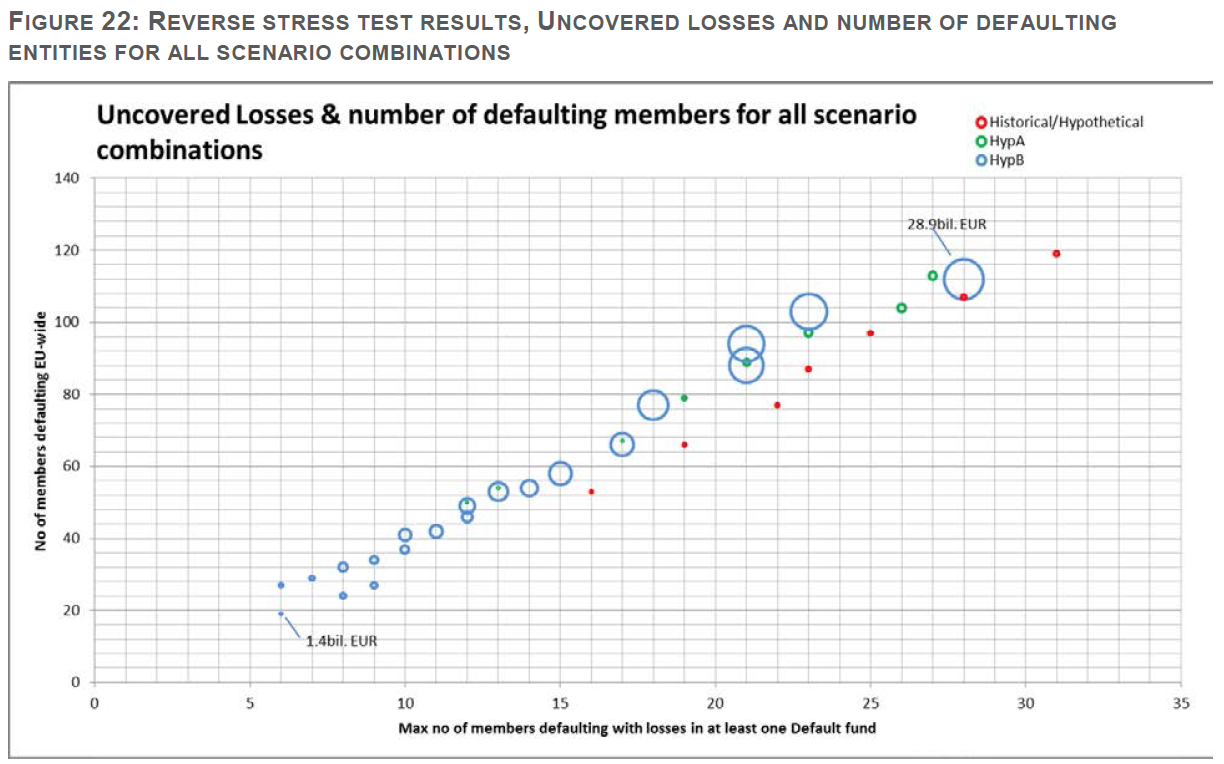

Reverse Stress Tests

These seek to test sufficiency of resources by considering an increasing number of defaulting entities in order to assess whether there is a plausible combination of member default and market stress scenarios that could lead to a systemically significant shortfall in the available resources.

The amount of significant uncovered losses (i.e. losses exceeding the not-prefunded resources by more than 1bn EUR) are summarised in Figure 22.

The results show that an implausibly large number of member firms would have to default e.g. 100 entities, to lead to uncovered losses of €28.9b. When the analysis is focused on a theoretical, highly extreme but less improbable assumption of less than 15 members defaulting at the EU-wide level and less than 5 members hitting a default fund with losses, the maximum shortfall of prefunded resources is less than 6bn EUR, while no uncovered losses exceeding 1bn EUR are identified.

From the ESMA doc, “no scenarios have been identified that are expected to be plausible and have at the same time a destabilising systemic impact on an EU-wide level.” Very good.

That’s it for the results.

More Recent Data

As the ESMA study was published 15 months after the results were gathered, it would be prudent to run this exercise again, particularly as EMIR Mandatory Clearing dates in 2016 are passed. (I don’t know whether there are plans to make this an annual exercise like the ECB Bank Stress Tests).

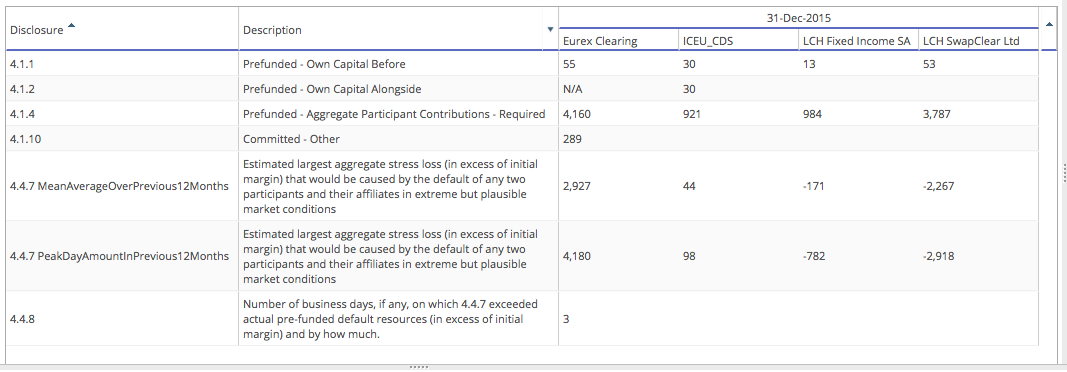

We can get a quick indication of the growth in CCPs by using CCPView to look at the CPMI-IOSCO Quantitative Disclosure data.

Showing as of 31 Dec 2015:

- Eurex Clearing with a Total IM of $47billion

- ICE Clear Europe Credit with an IM of $6.6b (excludes ICE Europe FnO)

- LCH Cash and Derivatives SA with an IM of $3.8b

- LCH Fixed Income SA with an IM of $19.4b

- LCH RepoClear Ltd with an IM of $10.3b

- LCH SwapClear Ltd with an IM of $72b

- A total of $160billion or €140billion

- Already close to the €150 billion figure ESMA used for all 17 CCPs as of Dec 2014

Adding in the other Clearing Services of ICE, LCH SA, LCH UK, not to mention CCG and the remaining 12, would definitely exceed €150b by some margin.

CCPView also has interesting Stress test figures disclosed by CCPs.

Showing that Default Fund Prefunded Resources are sufficient to cover the default of any two members in extreme but plausible market conditions.

For obvious reasons the CPMI-IOSCO data is not disclosed at member level, so we will need to wait on ESMA to run it’s next study with updated data from CCPs to get a detailed update on the resilience of European CCPs.

One of the ESMA recommendations is that CCPs incorporate in their creditworthiness assessment of their Clearing members, the potential exposures these may face due to their membership in other CCPs. Not sure how a CCP could do that, without requesting data from a member or regulator, which may not be forthcoming. Perhaps only ESMA could do that effectively.

I will end by encouraging you to read the ESMA press release or the full report.

That’s all for today.