The lawsuit from the British government in 2011 on euro zone CCP residency is coming to a ruling in the EU court Wednesday March 4th (according to this risk article – subs. required and this otcspace article). The idea is that CCPs clearing a 5% slice of euro-denominated products in a given category have to be incorporated in the euro zone.

Though the figures show a disproportionate amount of euro clearing outside the euro zone, my view in summary is that currency is a red-herring and nothing good can come from the rule standing.

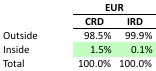

How much EUR clearing is in the euro zone? Very little

OTC figures from CCPView show that next to no euro-denominated OTC derivatives clear in euro zone incorporated CCPs today.

And there’s more: there are other not-yet-active OTC CCPs aspiring to clear euro-denominated product (e.g. CME Europe, Nasdaq OMX).

If the ruling is not limited to OTC and applies to futures and repo there are some other leading CCPs in London with a problem (e.g. ICE EURIBOR futures, LCH NLX EURIBOR futures, LCH Repoclear).

What if it went through?

Supposing so (presumably after further rounds of lawsuits or lobbying) maybe London-based CCPs would set up shop in Dublin or Paris. A lot of expense would be incurred with very little benefit. Existing euro zone CCPs might get a boost e.g. Eurex. It’s hard to construe this as equitable or just in the end.

Worse still perhaps the euro might decline in use outside the euro zone because of the restrictions on hedging. I had thought the intent was for the euro to become a rival benchmark for the dollar?

Who has the most to lose? LCH, ICE and CME

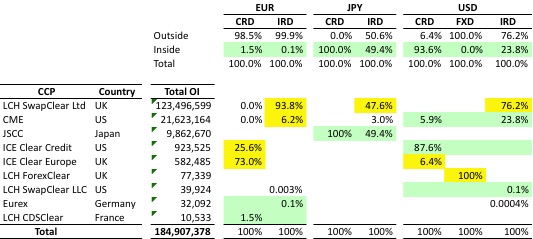

The chart below shows the OTC CCPs by country of incorporation and their shares of OTC cleared open interest in Credit, FX and Rates. I’ve highlighted in yellow the CCPs outside the euro zone with above 5% of the open interest in each asset class.

Just for fun I did the same for USD and JPY to clarify that EUR is not the only currency with this effect.

OTC CCP G3 Currency Open Interest by CCP (Source: CCPView)

Note: assumes product categories are asset classes and notional open interest share is a good proxy for open credit exposure.

Impact outside the EU?

The press is focusing on the UK / Sweden vs. euro zone issue. However, about 6% of euro IRS open interest is in CME and 26% of euro CDS open interest are in US incorporated CCPs.

I doubt the EU court has jurisdiction over non-EU CCPs but if not then enforcing the rule would mean US CCPs would have an advantage over EU CCPs from UK, Sweden etc. (Ironically this would mean that if the UK exited the EU there’d no longer be a problem!)

On the other hand if the ruling does apply in some way to non-EU countries then the non-EU countries would likely make it a problem in discussions given there is no similar rule for their currencies. For both USD and JPY there are major amounts of clearing in offshore CCPs (see above chart). Cue further conflict between EU and the US.

Regulate by geography not currency

The more fundamental point is that currency of denomination is just a way of analyzing exposures but not a way of carving up regulatory jurisdiction. A silly example makes the point: if an EU company buys oil futures denominated in USD on a European exchange would it make any sense for the CCP to have to be in the US?

The regulatory structure in preparation for a crisis works by location. CCPs are regulated by national regulators of their country of incorporation but in line with ESMA regulations in the case of the EU countries outside the euro zone. This includes dealing with financial crises.

Given regulatory coverage is in place and there is no precedent or similar rule for other benchmark currencies, it seems reasonable for the UK and US CCPs incorporated in London (as well as NASDAQ OMX in Stockholm) to cry foul.

Of course part of the underlying rationale here is EU politics. Deep-seated intra-EU resentments linger both against countries who did not join the euro at inception or against London in particular for remaining the financial center of Europe since. In the end it is for this reason that euro zone CCPs are small beer right now.

Takeaway

Shifting CCPs to Dublin or Paris might be expensive but is doable whether fair or not. Weakening the euro’s use as a currency of transaction beyond the euro zone may be much worse.

Regulation is fundamentally about geography not currency. Only a UK success in this matter can avoid a huge distraction from the work to make the EU financial system safer.

This article is authored by Jon Skinner.

UPDATE on 4 March 2015

The EU General Court sided with the UK, see Court Upholds British Challenge to ECB policy on Clearing Houses

I just spotted that the ECJ ruled in favor of the UK according to this article in Global Capital: http://www.globalcapital.com/article/qkphfst227xg/euros-can-be-cleared-outside-eurozone-rules-ecj

This seems the only sensible outcome.

J