It’s time to update our analysis of FCMs. The data from our last report showed a few things:

- The number of FCM’s reaching a 14-year low

- Any growth in pledged collateral being in “Cleared Swaps”

- A concentration of margins within the top firms, including 96% of swaps being cleared by the top 10 firms.

Let’s see what, if anything, has changed.

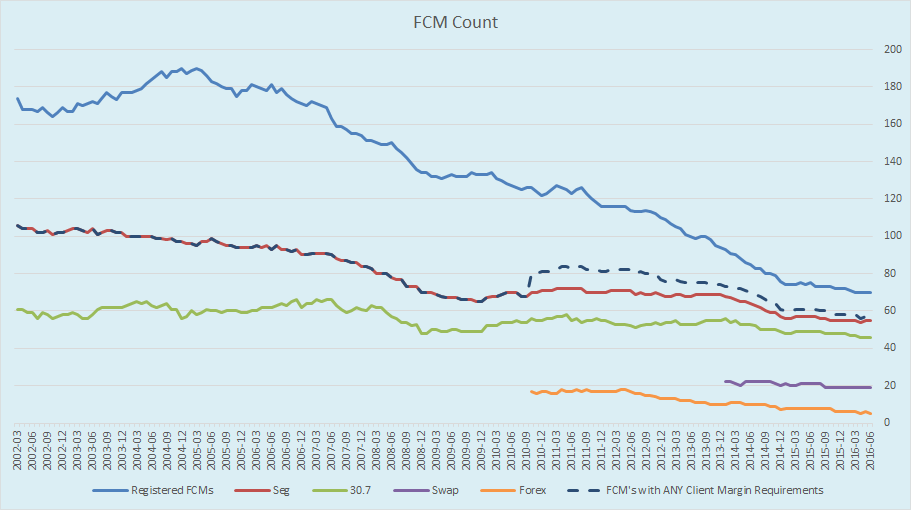

FCM Count

Starting with a simple count of the registered FCMs every month since reporting began in 2002. This number now stands at just 70, off from it’s peak of 190 in 2004 (top blue line).

The other lines on the chart illustrate how many FCMs have client margins required by clearing houses:

- FCMs with any client margins whatsoever is just 57. So this implies there are 13 inactive FCM’s ?

- 55 FCMs have activity in Futures & Options (Seg)

- 46 FCMs have activity in Foreign Futures & Options (30.7)

- 19 FCMs have activity in Swaps. So if you want to begin clear swaps, you can probably meet them all on a day trip.

- 5 FCMs have activity in Forex.

I should note that all 19 swap FCMs also clear futures. That seems obvious to me, but I am aware of some firms that struggle to find an FCM to clear swaps. Is there a reason there are no boutique swap-only FCMs? I presume the answer is “they would not be profitable”!

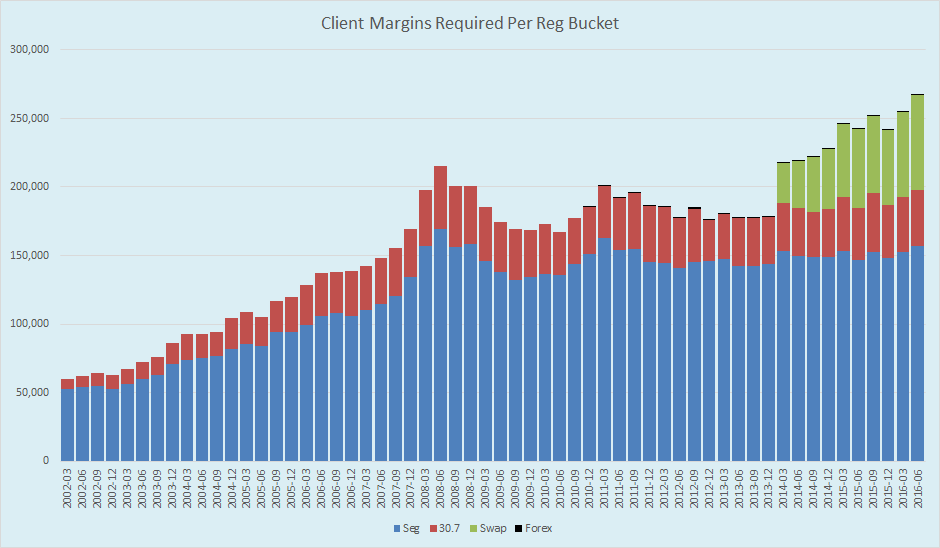

How Much Margin

Next lets update our chart of required margins, broken out by asset class. The total amount of margin pledged to support these cleared derivatives stands at 267 billion dollars:

This chart now starts out in March 2002. Few things I find interesting:

- Impressive industry growth from 2002 through 2008

- Futures and Options margins (both Seg and 30.7) are flat to down since 2008 to today. And I don’t think its because SPAN margin has gotten any cheaper!

- FCM Swap reporting began in 2014, and continues to account for the growth in derivatives leverage

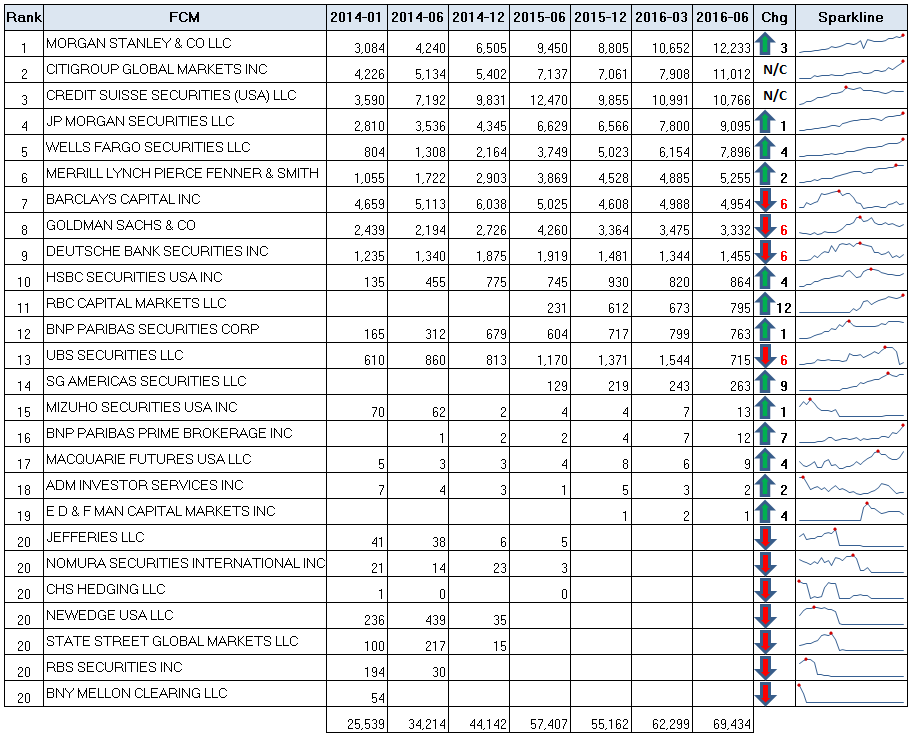

League Tables

Of course we want to see who the winners and losers are. (And maybe who just doesn’t want to play). Hence I give you the FCM league table. Starting with Cleared Swaps:

Some things to note:

- The changes (“Chg” column) shows changes from Jan 2014

- Morgan Stanley takes over the #1 spot from Credit Suisse, from our previous report in March 2016

- While we can see there are 19 firms that have activity, really only 9 firms have margins over $1bn.

- Only 14 firms with over $100 million. Heck I can think of some individual swaps that require $100 million in collateral!

- The Sparkline shows a mini monthly chart of required margins. The red dots in the Sparkline tell you when the FCM hit their peak. 4 of the top 5 are at their peaks, so still growing.

- All European firms are off of their peaks

- High concentrations remain within swap clearing:

- Top 3 FCMs account for 49% of the business

- Top 5 FCMs account for 73%

- Top 10 FCMs account for 96%

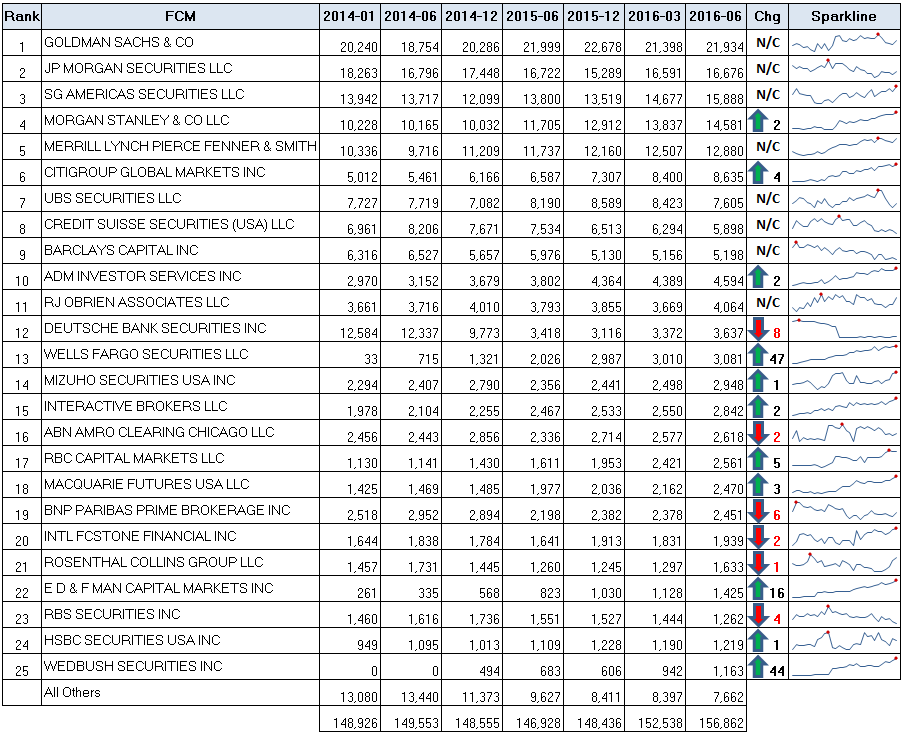

Futures and Options

We’ve updated our analysis to now bring you a league table for Futures & Options (Seg) as well:

A few points here:

- I cut the list at $1bn, which nicely stopped at the top 25

- The Futures rankings seem much more stable than swaps

- There are a few notables that have leapt up the list in the past 30 months:

- Wells Fargo up 47 spots !?

- Wedbush up 44

- ED&F Man up 16

- The top 2 FCMs are off of their historic highs

- The concentration within futures clearing not quite as high as in swaps:

- Top 3 FCMs account for 35% of the business

- Top 5 FCMs account for 52%

- Top 10 FCMs account for 73%

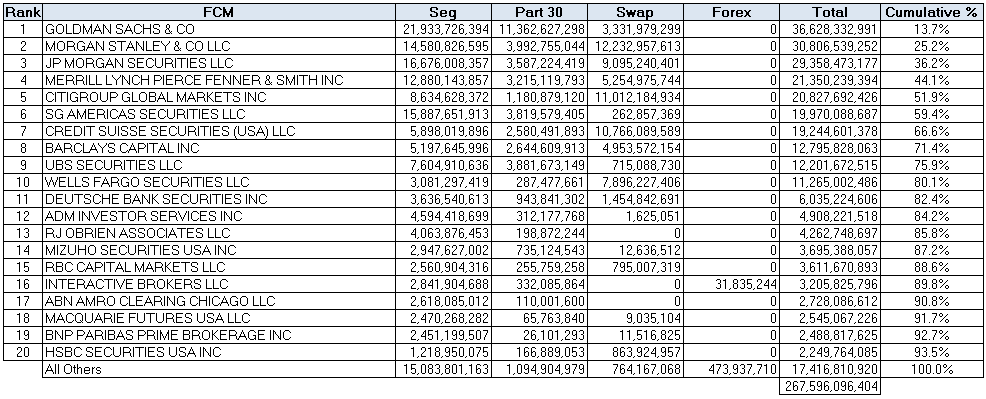

All Four

And finally, if we put it all together, and combine all 4 regulatory buckets, can get a league table as of June 2016:

I would note:

- Goldman Sachs clear #1

- Goldman’s with a tremendous amount of 30.7 margins. Just as a reminder, these are generally speaking the US-domiciled accounts for customers with futures & options traded on foreign exchanges.

- Forex is insignificant

- 80% of derivatives margin within top 10

Summary

The general theme continues from our March report:

- The growth in clearing is in swaps

- European banks stand out as retreating, or not growing as much as US firms

- The business is concentrated within the top 5 or so firms

I am reminded of an article by Joe Rennison of the Financial Times, which basically says:

- Many global investment banks have little capacity left on their balance sheets to clear derivatives for their clients. There is reference to being at 80% capacity.

- New margin requirements for bilateral swaps will further limit that capacity

- Europe will begin clearing soon

- The clearing mandate in the US applies to just 85 commercial banks, given some exemptions.

- The clearing mandate in Europe applies to over 5,000 institutions

So 80% full with only 85 commercial banks having to clear. And we just need to jam another 5,000 in there. There are a few flaws with the argument, but the overall tone seems to be fair: you don’t want to be anywhere near the bottom of that list of 5,000 and looking for a clearing broker.

We’ll be back in a few months to update our analysis.

great job sorting through the data. it’s quite alarming to see the decrease in the number of firms that offer clearing services. re the clearing mandate – a lot more than 85 commercial banks are required to clear. check with the lawyers for the details, but my understanding is that the mandate covers hedge funds, asset managers, and most other types of financial institutions above a certain level of size and trading activity. So the clearing capacity issue is even worse than you might think.

Thanks Will. Yes I think you are right, 85 did seem low, in fact that is one of the “flaws” I refer to. It does surprise me that even in the US, there are some firms that struggle to get an FCM for swaps, so I have to believe there will be a problem in Europe.

hi Tod

Interesting to put this together with the IM mandate and the clearing mandate. My view is essentially today that the clearing and reg IM model is wrong in three regards: 1. the clearing mandate was unnecessary and the bilateral IM mandate should havae been introduced sooner instead. 2. As a result too many trades are cleared by force using up clearing members capacity to clear for clients 3. Client clearing mandate only just started in Europe which will make this worse. 4. The bilateral IM mandate will create further pressure to clear and capacity will be used up. 5. There is a perfectly good solution (though a bit out of the box) which is to change the client clearing model to pure agency – see link below. 6. if this were adopted I bet you would see Goldman push into client clearing on that basis like it has for other less capital intensive products than OTC…

Best

Jon

http://www.theotcspace.com/2015/04/02/pure-agency-reducing-client-clearing-bank-capital-burdens