Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in February 2016.

First the highlights:

- On SEF USD IRS in February 2016 volume was > $1.3 trillion

- For price forming trades, DV01 was 11% higher than the prior month

- Butterfly and Curve trades were up

- USD SEF Compression volumes was exceptional at >$220 billion

- USD Swap Rates continued downwards with a 15bps flattening

- SEF Market Share shows gains for Tradeweb, driven by Compression

- And gains for Tradition, driven by higher CME-LCH Switch volumes

- CME-LCH Basis Spreads tightened significantly (by 1.5bps for 30Y)

- Global Cleared Volumes in G4 Ccys was much higher

- Driven by LCH SwapClear increasing 22% from the prior month

- LCH SwapClear successfully launched AUD OIS with Feb volumes higher than AUD IRS

Onto the charts, data and details.

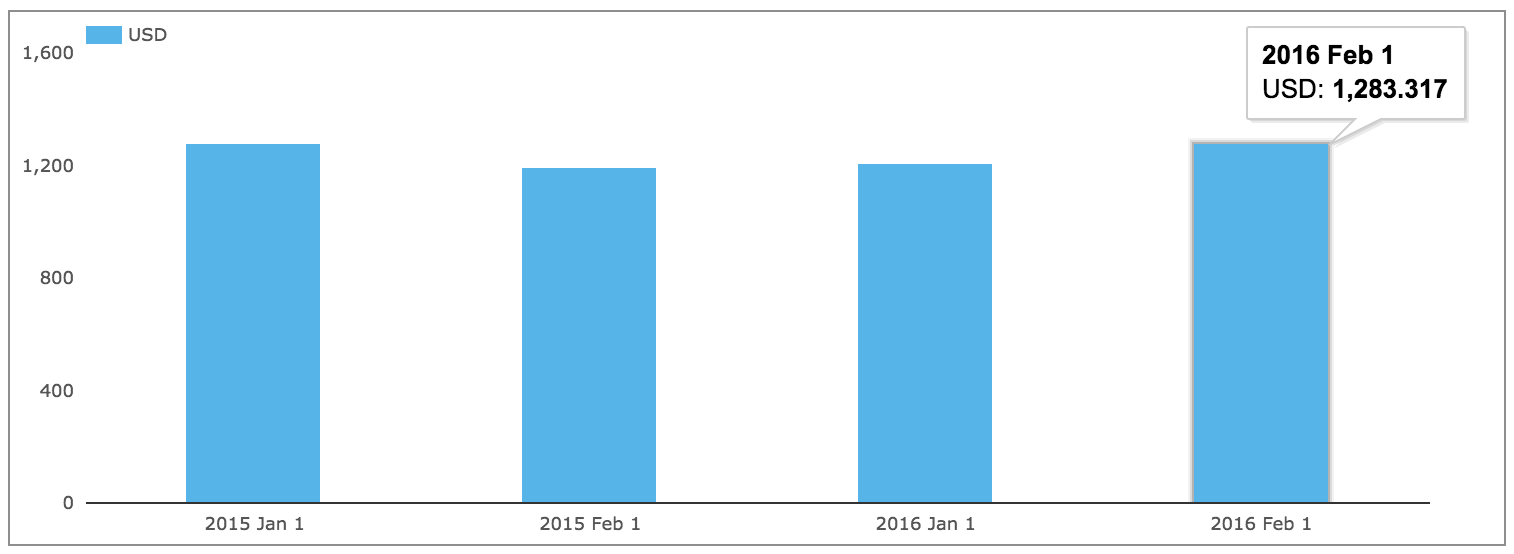

USD IRS ON SEF

Using SDRView lets start by looking at gross-notional volume of On SEF USD IRS Fixed vs Float and only trades that are price forming, so Outrights, SpreadOvers, Curve and Butterflys.

Showing:

- February 2016 gross notional is >$1.28 trillion

- (recall capped trade rules mean this is understated as the full size of block trades is not disclosed)

- A little higher than January 2016 (by 6%)

- Compared to February 2015, gross notional is up 7% (2016 being a leap year must have an impact)

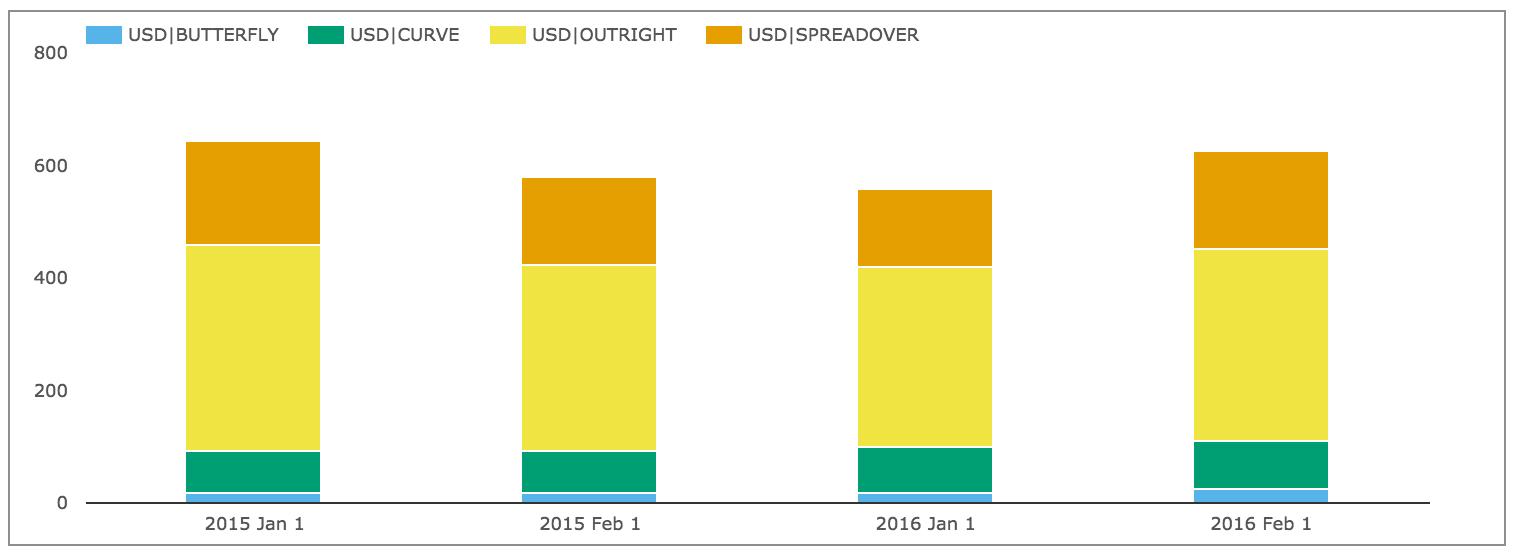

And splitting by package type and showing DV01 (adjusted for curves and flys).

Showing:

- In DV01 terms February 2016 was 11% higher than January 2016

- Overall >$630 million of DV01 was traded in the month

- (recall capped trade rules mean this is understated)

- Butterfly and Curve DV01 was higher in February 2016 than any of the other months shown

- Outright and Spreadover were higher than each mont except for January 2015

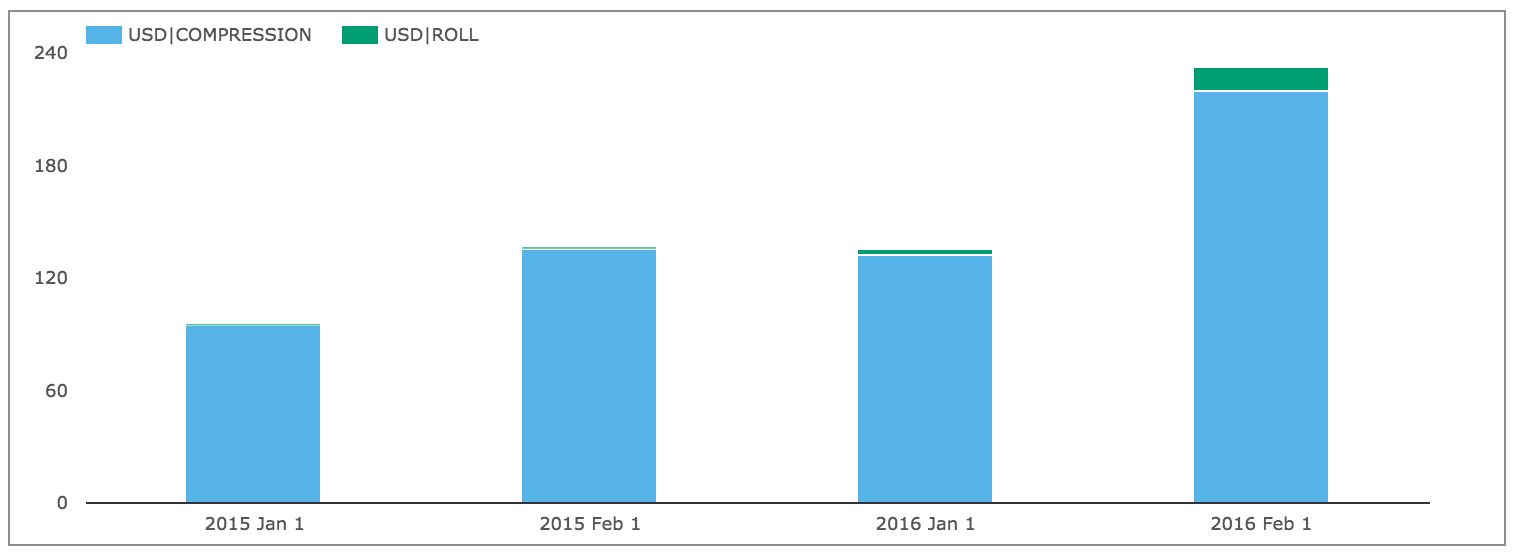

And gross notional of non-price forming trades; Compression and Rolls.

Showing:

- Exceptionally high Compression activity of >$220 billion

- Far higher than January 2016 and the corresponding months in 2015

- Surprisingly high Rolls for a non-IMM Month

- Many of these are 10Y Swaps, so probably due to the new CME Ultra 10Y UST Future

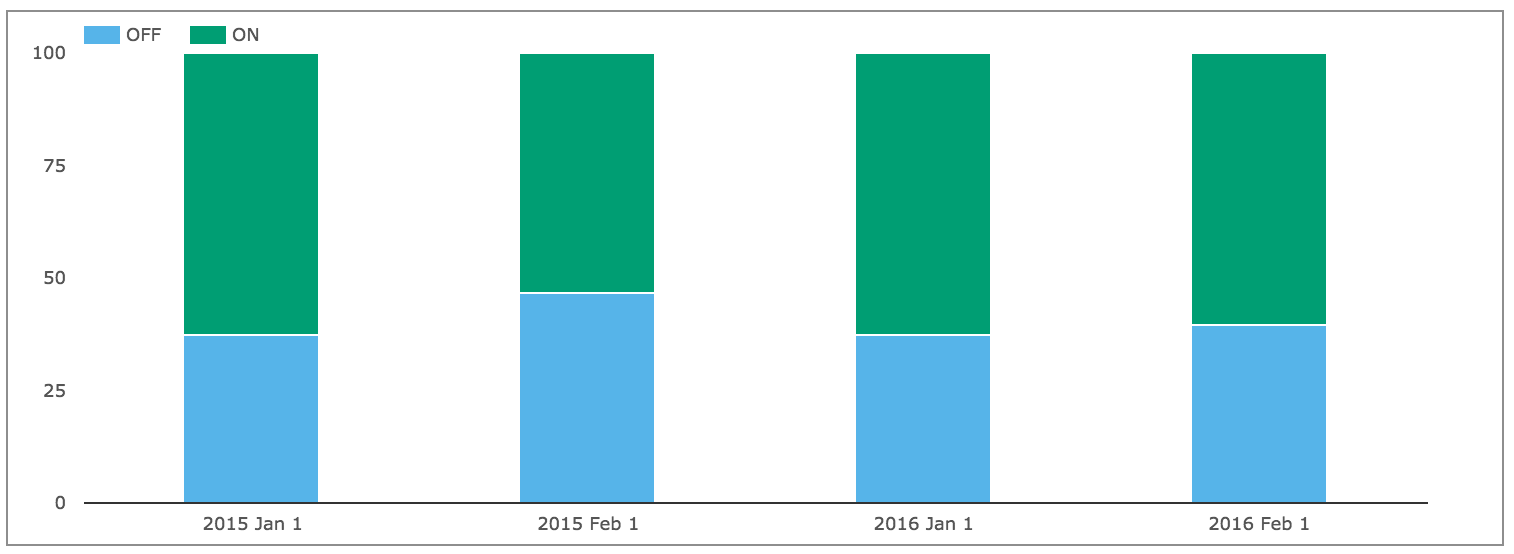

USD IRS OFF SEF

Comparing On SEF vs Off SEF for price forming trades.

Showing that On SEF vs Off SEF remains at 60% to 40% while February 2016 has a lower Off SEF percentage than February 2015 (40% vs 47%).

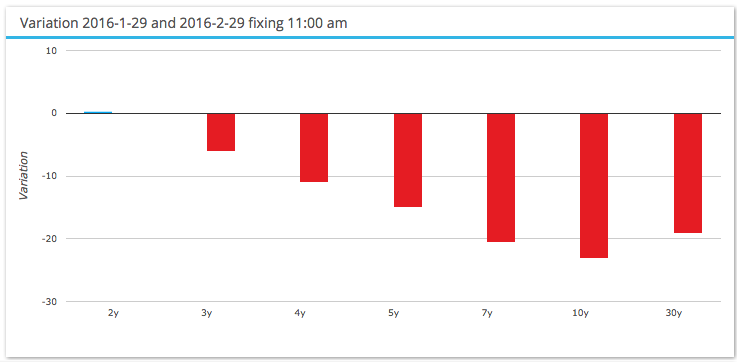

USD IRS Prices

Lets now take a look at what happened to USD Swap prices in the month.

Showing that:

- Rates continued the downward move we saw in January

- Not as large, but certainly more than an average month

- A flattening with short rates un-changed, medium down 15bps and long rates down 20bps

- Which will have resulted in significant Variation margin calls over the month

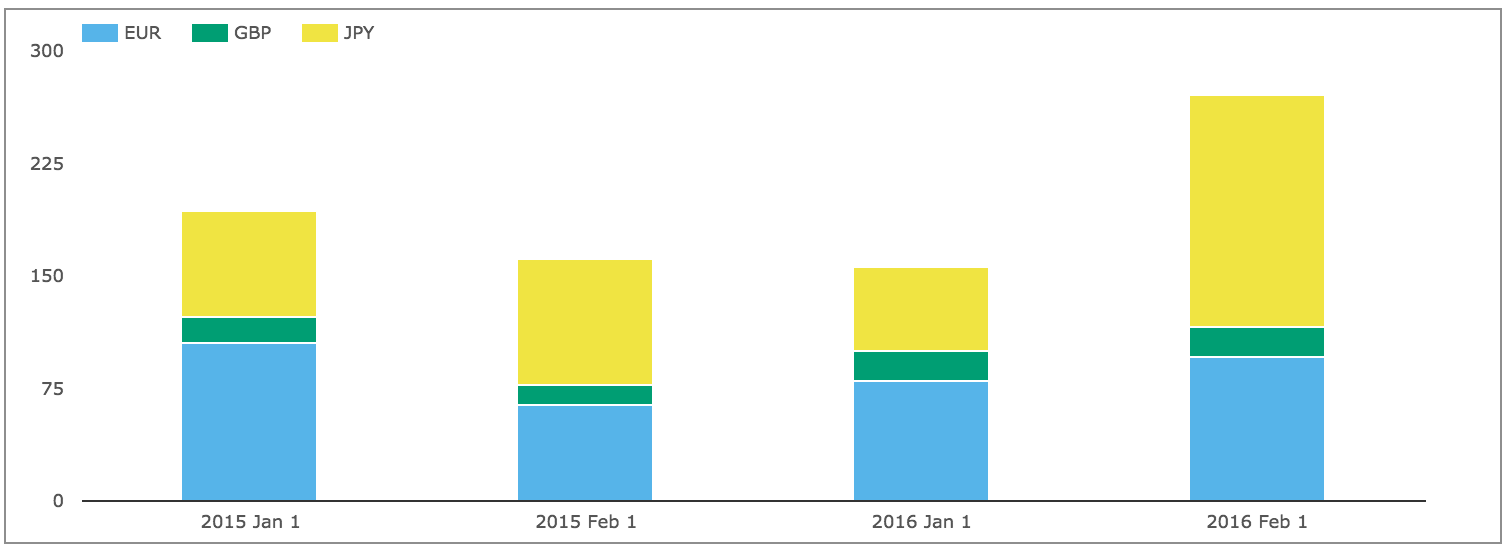

EUR, GBP, JPY Swaps

Lets also take a look at On SEF volumes of IRS in the other three major currencies.

Showing that for price forming trades JPY volumes were much higher in February 2016 than the other months; something to do with Swap rates going (more) negative last month? While the overall gross notional in these three currencies of >$156b in January is just 13% of the USD volume.

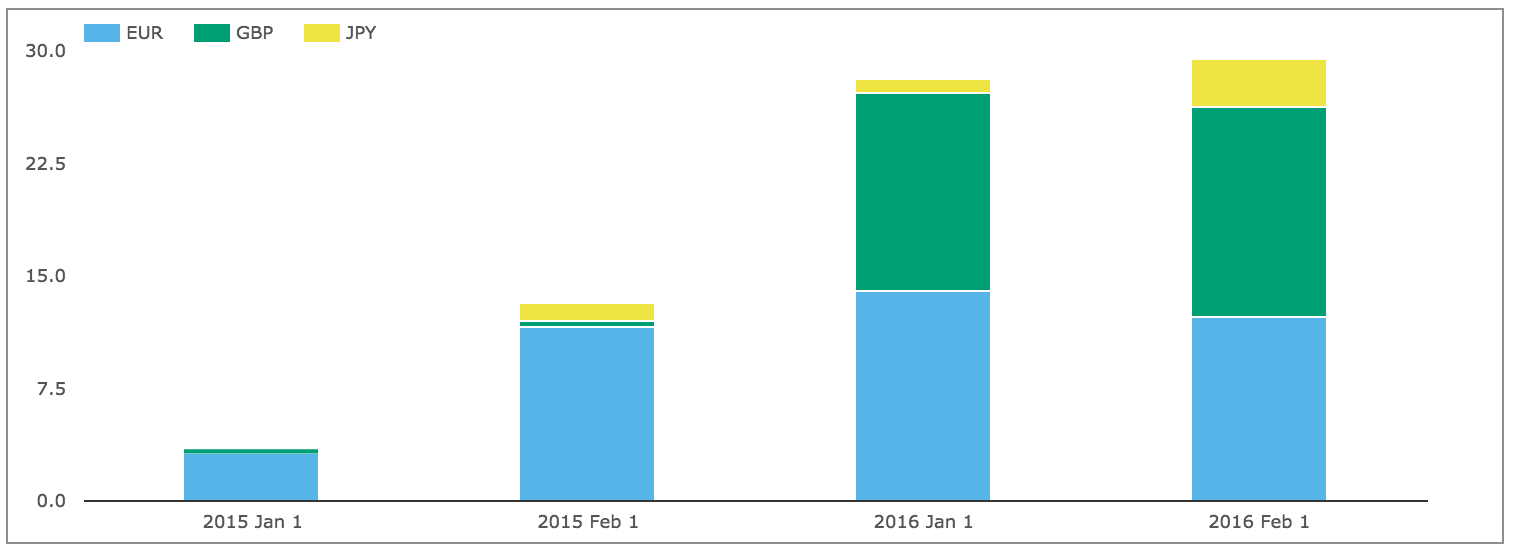

And then looking at SEF Compression activity.

Showing that compression in EUR and GBP is running at much higher levels in the first two months of 2016 than the corresponding months in 2015.

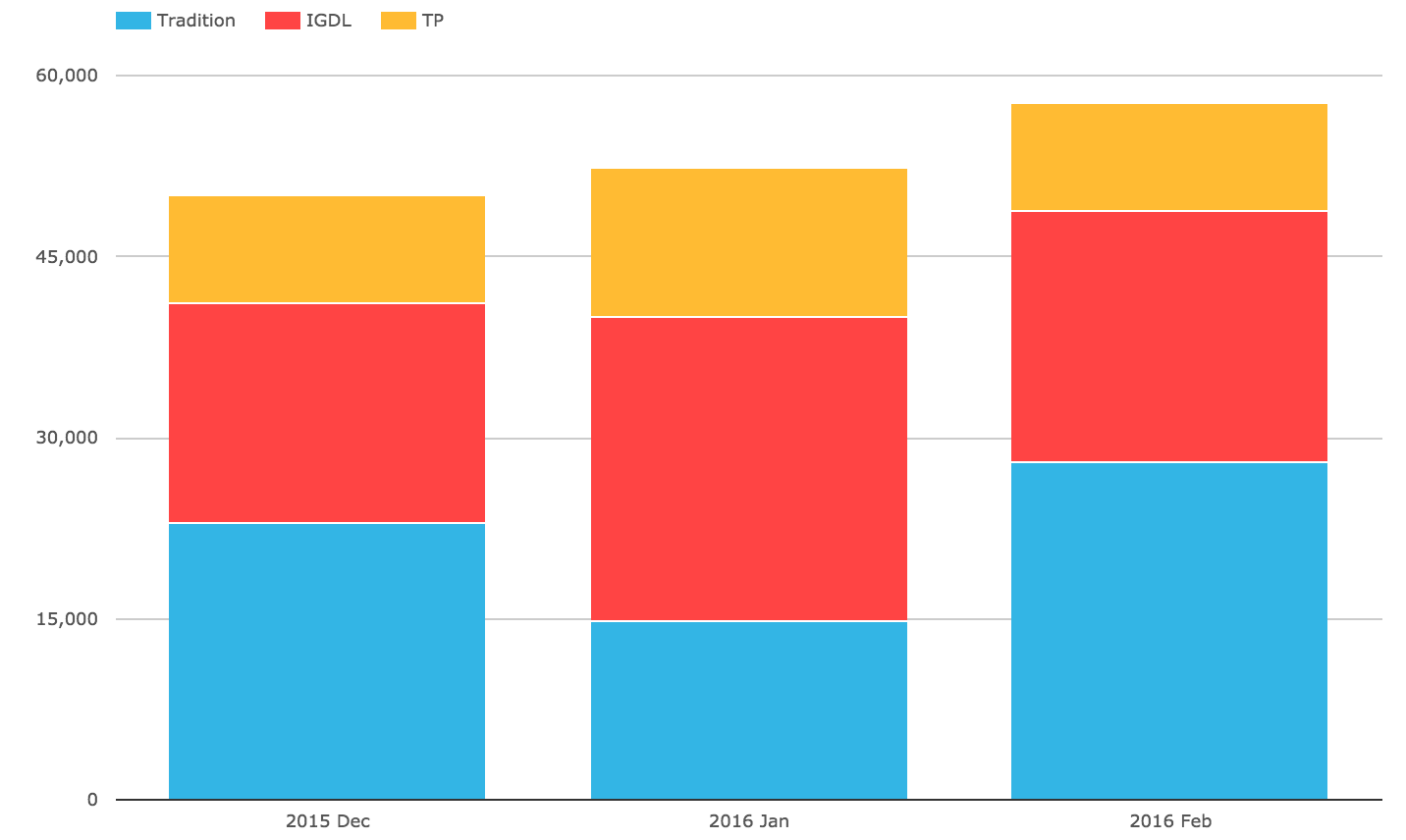

SEF Market Share

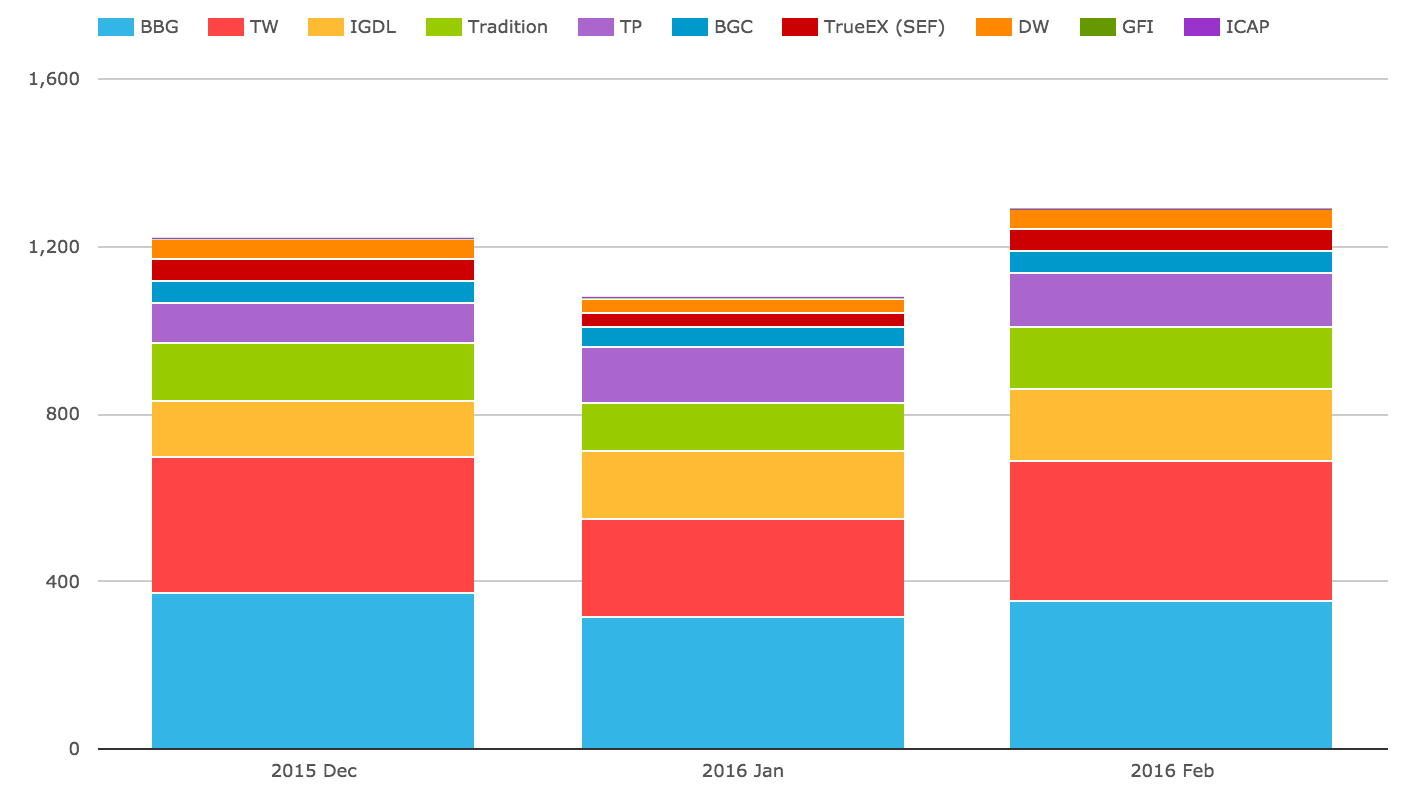

Lets now turn to SEFView and SEF Market Share in IRS including Vanilla, Basis and OIS Swaps.

We will start by looking at DV01 (in USD millions) by month for USD, EUR, GBP and by each SEF. In a departure from our usual standard, we will include SEF Compression trades and use a chart to compare the relative share in February 2016 with the prior two months.

Showing that:

- Bloomberg retains the largest share in each month

- Tradeweb is very close in February

- As a result of higher SEF Compression activity in the month

- ICAP-IGDL is up from prior months

- Tradition is significantly higher than Jan

- Tullet slightly down from Jan

- BGC and Dealerweb are both up from prior months

- TrueEx also up, due to higher SEF Compression

So what can explain Tradition significantly higher?

You guessed it CME-LCH Switch trades.

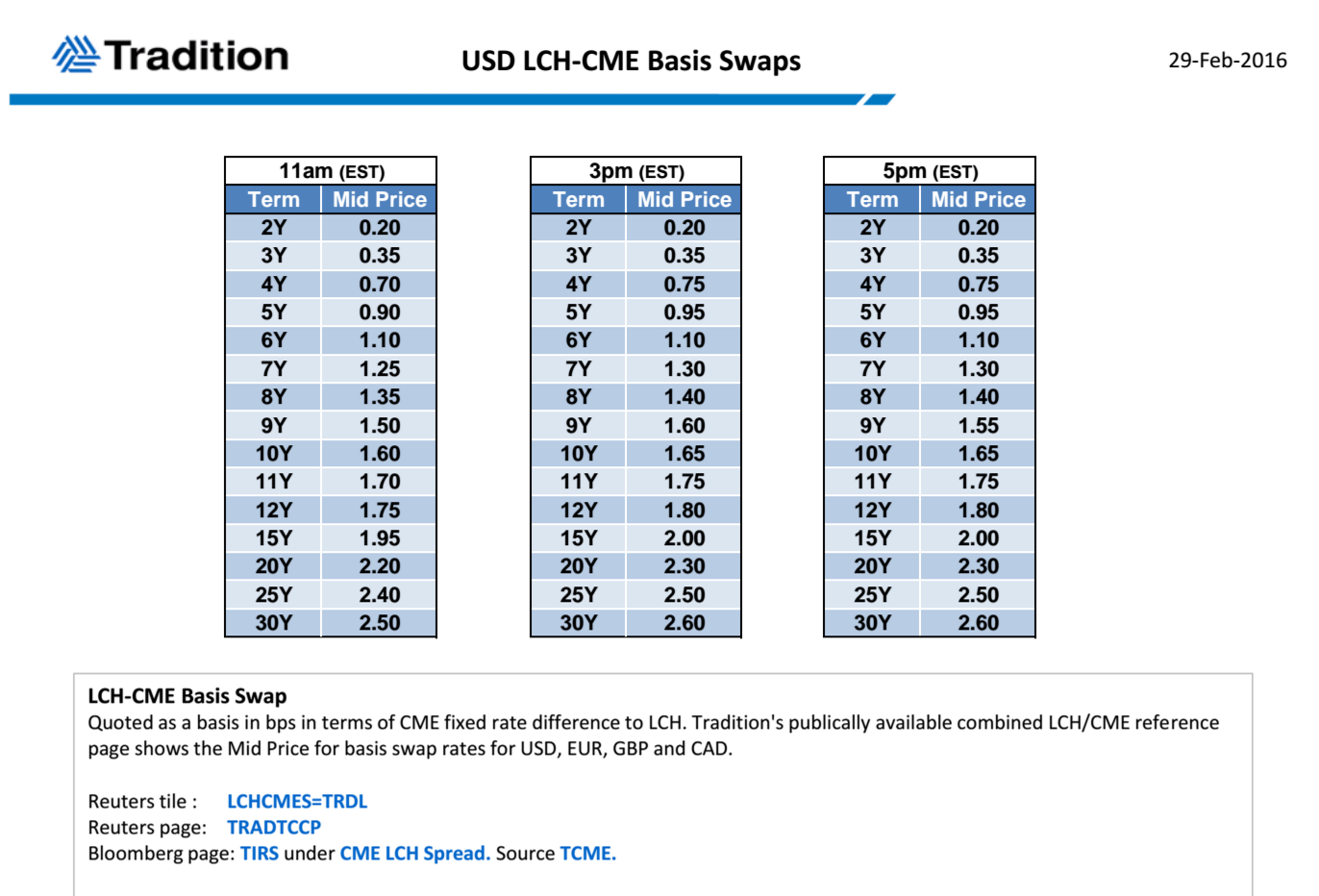

CME-LCH Basis Spreads and Volumes

Using SEFView we can isolate CME Cleared Swap volume at the major D2D SEFs (on the assumption that this is all CME-LCH Switch trade activity). Lets look at this for the past 3 months.

Showing:

- Overall volume in Feb was $58 billion gross notional

- Higher than the preceding months (except the record high in Nov)

- Tradition has grabbed back the major share from ICAP

- Explaining Tradition’s overall gain in the month

And what of CME-LCH Basis Spreads?

Well these narrowed significantly during the course of the month.

Lets look at Tradition quotes on Feb 29.

Showing:

- 5Y is now 0.95bps, which is down from 1.50bps on Jan 29

- 10Y is now 1.65bps, down from 2.65bps

- 30Y is now 2.60bps, down from 3.95bps

Significant falls indeed, 30Y down 1.5bps.

No wonder CME-LCH Switch trade volumes have remained at the higher levels observed since November 2015.

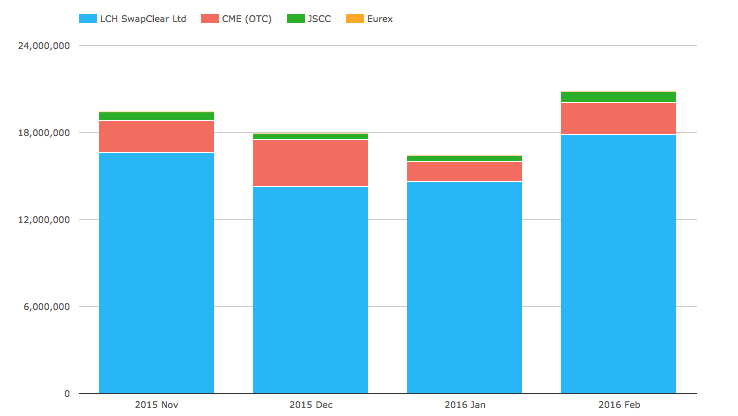

Global Cleared Volumes

Now onto CCPView to look at Global Cleared Swap Volumes for EUR, GBP, JPY & USD Swaps.

Showing:

- Overall Global Cleared Volumes were significantly up in February

- LCH SwapClear specifically increased by 22% from January

- And is the highest of any month in our period

- CME is also up from January

- JSCC is significantly up from prior months

Comparing USD Vanilla IRS LCH Client Clearing with CME OTC would show 69% to 31% for February, similar to January.

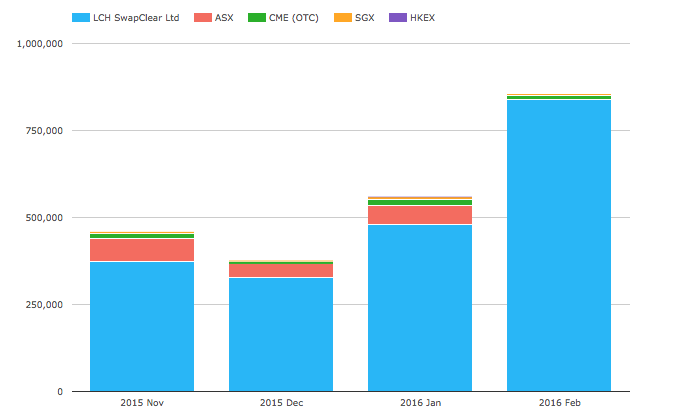

And before we end, lets look at something new, the volumes of AUD, HKD, SGD Swaps (including Vanilla, OIS, Basis, Zero Coupon).

Showing:

- LCH SwapClear is massively up in February, by 75% over prior month

- ASX figures for February are not yet available

- CME and SGX register on the chart

- HKEX not visible

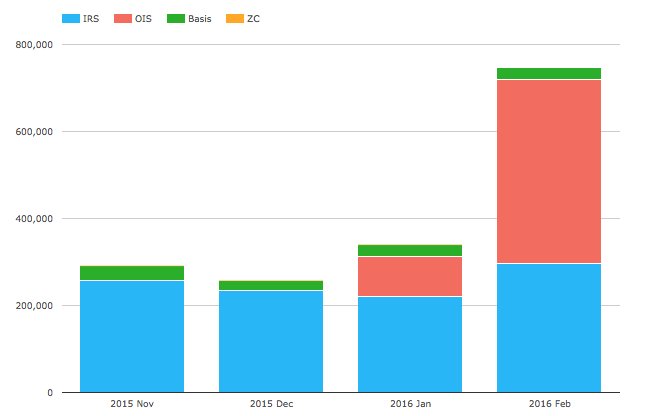

And focusing just on LCH SwapClear and AUD, we see:

Showing a very successful launch of AUD OIS (AONIA) by SwapClear in January and record volumes for this product in February, even surpassing their IRS volumes.

Thats it for today.

A lot of charts.

Thanks for staying to the end.

Our Swaps review series is published monthly.