In January 2019, the Basle Committee on Banking Supervision (BCBS) revised the 2016 market risk framework, generally known as the Fundamental Review of the Trading Book (FRTB) to address design and calibration issues and to provide further clarification.

One of the topics of interest is an improved criteria for the identification of modellable risk factors or what is referred to in the document as the Risk Factor Eligibility Test (RFET).

Background

In articles I wrote in 2017 and 2016, I covered the details for modellable and non-modellable risk factors as they were defined in the 2016 document, see here, here and here. In particular how our FRTB for Excel product and Microservices API provides a simple and powerful way to check that a risk factor passes the eligibility test.

This is important as not only do non-modellable risk factors result in a higher capital charge but also because granular risk factors can improve the result of the Profit Loss Attribution (PLA) test required for Internal models.

What has Changed?

The 2016 version of the test for continuously available real prices is defined as follows:

- a risk factor must have at least 24 observable real prices per year

- with a maximum period of one month between two consecutive observations

- the above criteria must be assessed on a monthly basis

- and measured over the current ES period (e.g. past 12 months)

This is changed in the 2019 version to:

To pass the RFET, a risk factor that a bank uses in an internal model must meet either of the following criteria on a quarterly basis.

- The bank must identify for the risk factor at least 24 real price observations per year (measured over the period used to calibrate the current ES model, with no more than one real price observation per day to be included in this count). Moreover, over the previous 12 months there must be no 90-day period in which fewer than four real price observations are identified for the risk factor (with no more than one real price observation per day to be included in this count). The above criteria must be monitored on a monthly basis; or

- The bank must identify for the risk factor at least 100 “real” price observations over the previous 12 months (with no more than one “real” price observation per day to be included in this count).

The first option for the test retains the 24 real price observations, but replaces the one month minimum gap between observations with “no 90-day period with fewer than 4 real price observations in the previous 12 months.

The second option is simply at least “100 real price observations over the previous 12 months”.

On the face of it this relaxes the test and allows it to cope with seasonality in markets, a common aspect of some commodity, energy and inflation markets.

Results in Practice

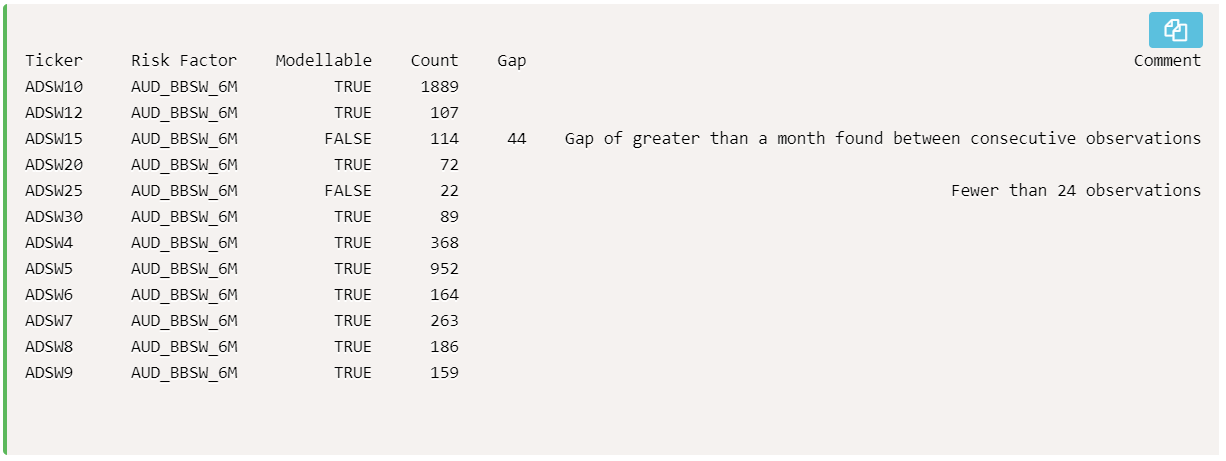

The Clarus Microservices API allows us to quickly assess the difference the new test makes for a set of risk factors. Let’s do this for AUD Swaps (BBSW 6M) using Python code, first for the 2016 test.

import clarusresponse = clarus.frtb.modellablerf(riskFactors='AUD BBSW 6M',jan2019Method='false') print (response)

Three lines of code and note the parameter “jan2019Method” is explicitly set to false.

The results of this are:

Showing that 15Y and 25Y tenor buckets fail the risk factor eligibility test (RFET).

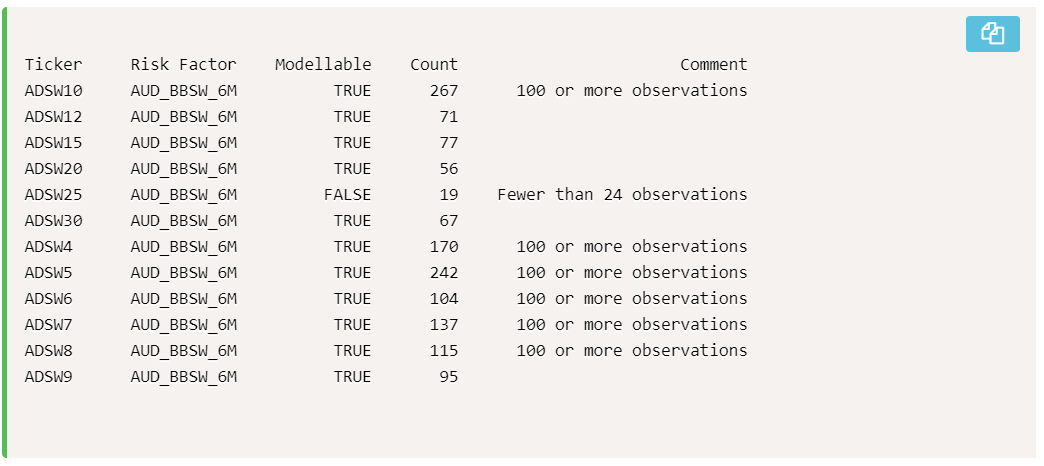

Running the same method but with the parameter “jan2019Method” set to true.

Shows that the 15Y point now passes the RFET but 25Y still does not.

While this may not seem important or significant, it could make a material difference in the capital required.

Now this is not meant to be a exhaustive analysis.

The point I am making is that it is easy to run the new RFET for any of the risk factor types we support; interest rate curves in more than twenty currencies, including OIS, IBOR, Basis and XCCY Basis risk. (Note: we plan to add Inflation, IR Vols and FX Vols).

Contact us if you are interested to find out more.

More Details on RFET

The 2019 revision includes many more details, including the concept of allowing all real price observations allocated to a bucket to assess whether it passes the RFET for any risk factors that belong to the bucket e.g. for the regulatory 25Y to 35Y bucket.

I don’t have time for all the details on this today, for those of you interested, please see pages 74 to 80 of the Minimum Capital Requirements for Market Risk Jan 2019 document.

Final Thoughts

The Risk factor eligibility test is important.

In discussions with banks we hear of different approaches.

Some firms want one vendor for all risk factors.

That ignores the reality of the real word.

Some banks want to pool data with others in their market.

That is likely to be much more expensive to do than expected.

Some firms want to use their own trade and firm price data.

That seems unlikely to provide sufficient coverage.

A few firms plan to combine multiple approaches.

For OTC derivatives, we think that our approach is very effective.

We utilise transactions reported to trade repositories.

And transactions on execution venues.

Both are backed by regulatory mandates that can be relied upon.

The Clarus solution should be part of your bank’s FRTB program.

Contact us if you are interested to try.